Today's ISM purchasing manager index from the US is today's most important number. I guess this week will see limited interest from market participants and the market year will start in earnest next week.

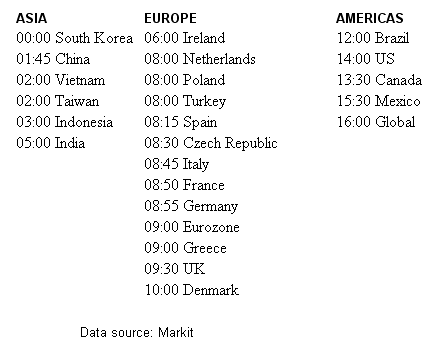

December Markit Manufacturing Purchasing Manager Index (08:58 GMT): After the preliminary data released on December 16, the final manufacturing data will be released today for most countries. The Eurozone-level PMI is expected to remain unchanged from the earlier flash estimate of 52.7. As the divergence between France (47.1) and Germany (54.2) continued growing according to the flash estimates, with France’s index below 50 and suggesting economic contraction, any revisions to the divergence are worth watching out for. All times are GMT:

Another important thing to watch will be the developing countries’ PMIs. When the Federal Reserve decided to postpone its asset-purchase tapering last September one reason was the turmoil in emerging markets, as countries with current account deficits saw hot money inflows stopping and reversing after the yields in the US had risen. Signs of weakness in developing economies could feed back to the developed world, and possibly slow down the Fed’s tapering schedule.

The European Central Bank’s (ECB) first meeting of the year will be held already next week, and today’s numbers, together with the end of 2013 and the high EURUSD rate could provide enough reason for the market to start speculating that the ECB will comment on the strong euro. In February 2013, ECB President Mario Draghi stated that the euro’s strength is problematic, and the rate was around 1.35 at the time. Now the rate is near 1.38.

See my earlier text on the flash estimates for more thoughts. Note that most of Markit data will be released on Reuters two minutes before they are published to the general public. The service PMIs will be released next Monday, January 6. The Markit press releases will be available here, and the first ones for Asia will already be out by the time you read this.

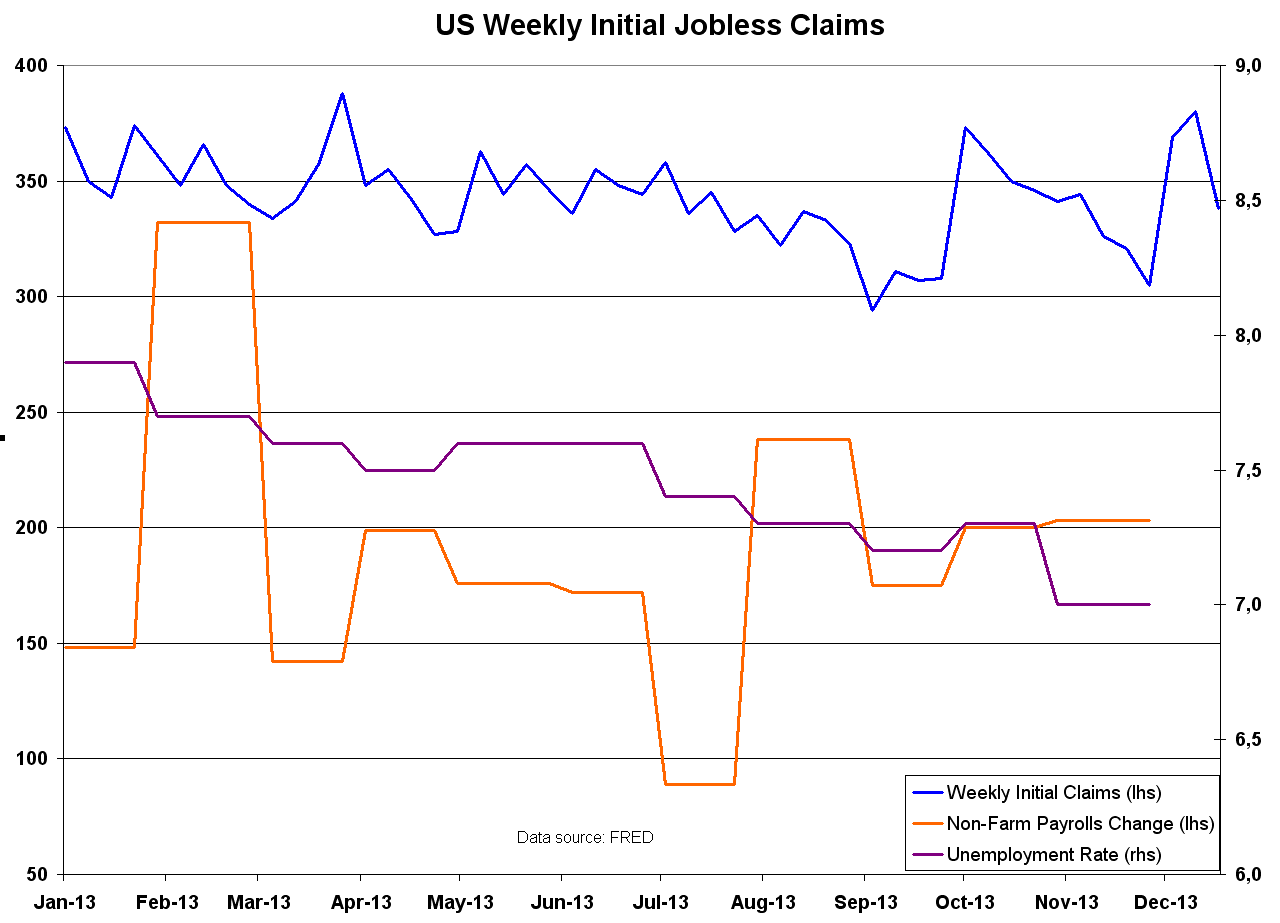

US Weekly Initial Jobless Claims (13:30 GMT): Jobless claims are expected at 334,000, almost unchanged from the previous week’s 338,000. Weekly claims are not one of the most important economic numbers usually, but as the job market is currently the key indicator dictating US monetary policy, it will be worth watching today.

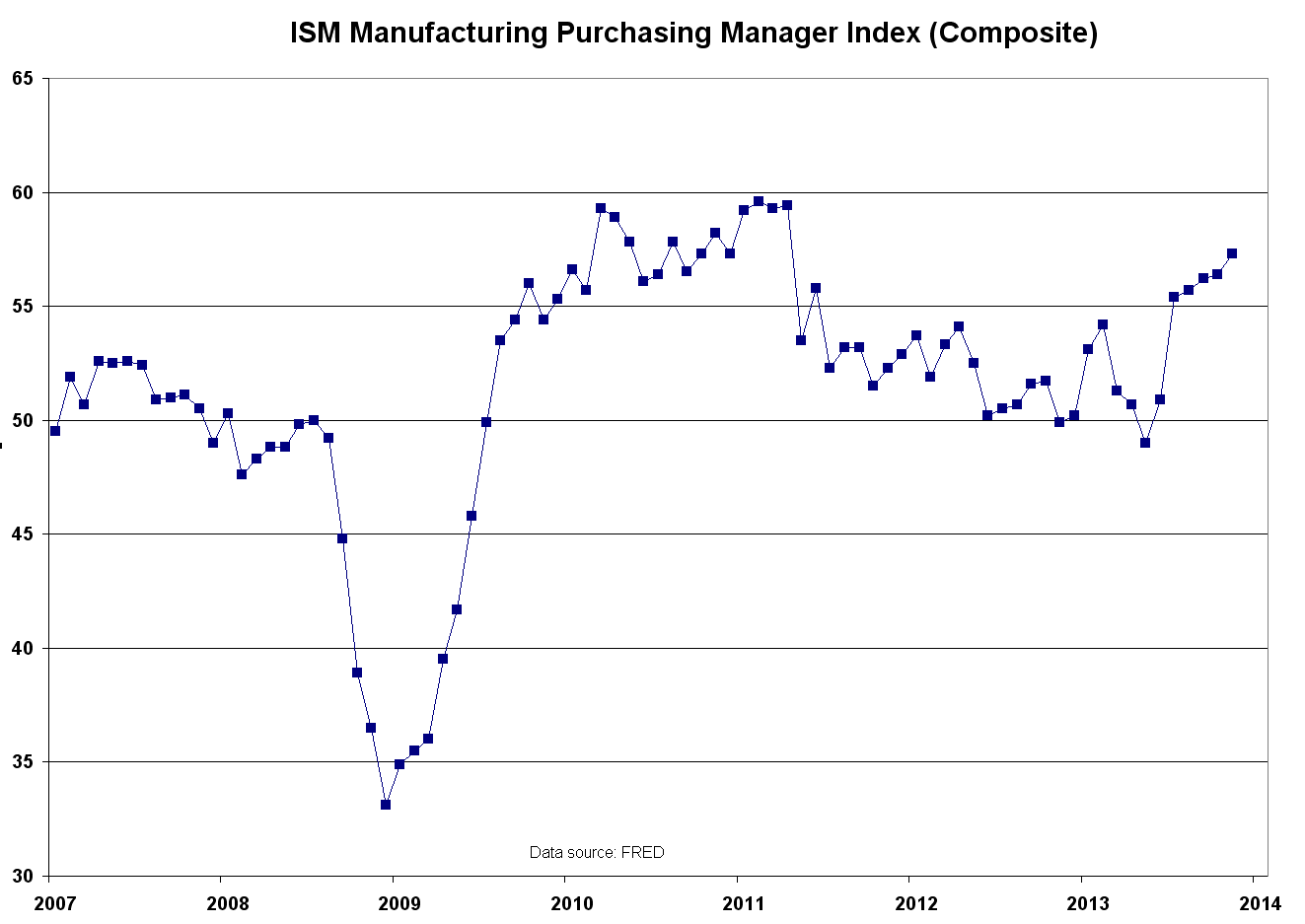

US December ISM Manufacturing Purchasing Manager Index (15:00 GMT): The PMI is expected to have fallen a little to 56.9 from November’s 57.3. The regional indices are already out, so a slight decrease should not be a shock to the markets, especially as the index is currently at relatively high levels and well above the 50-level.

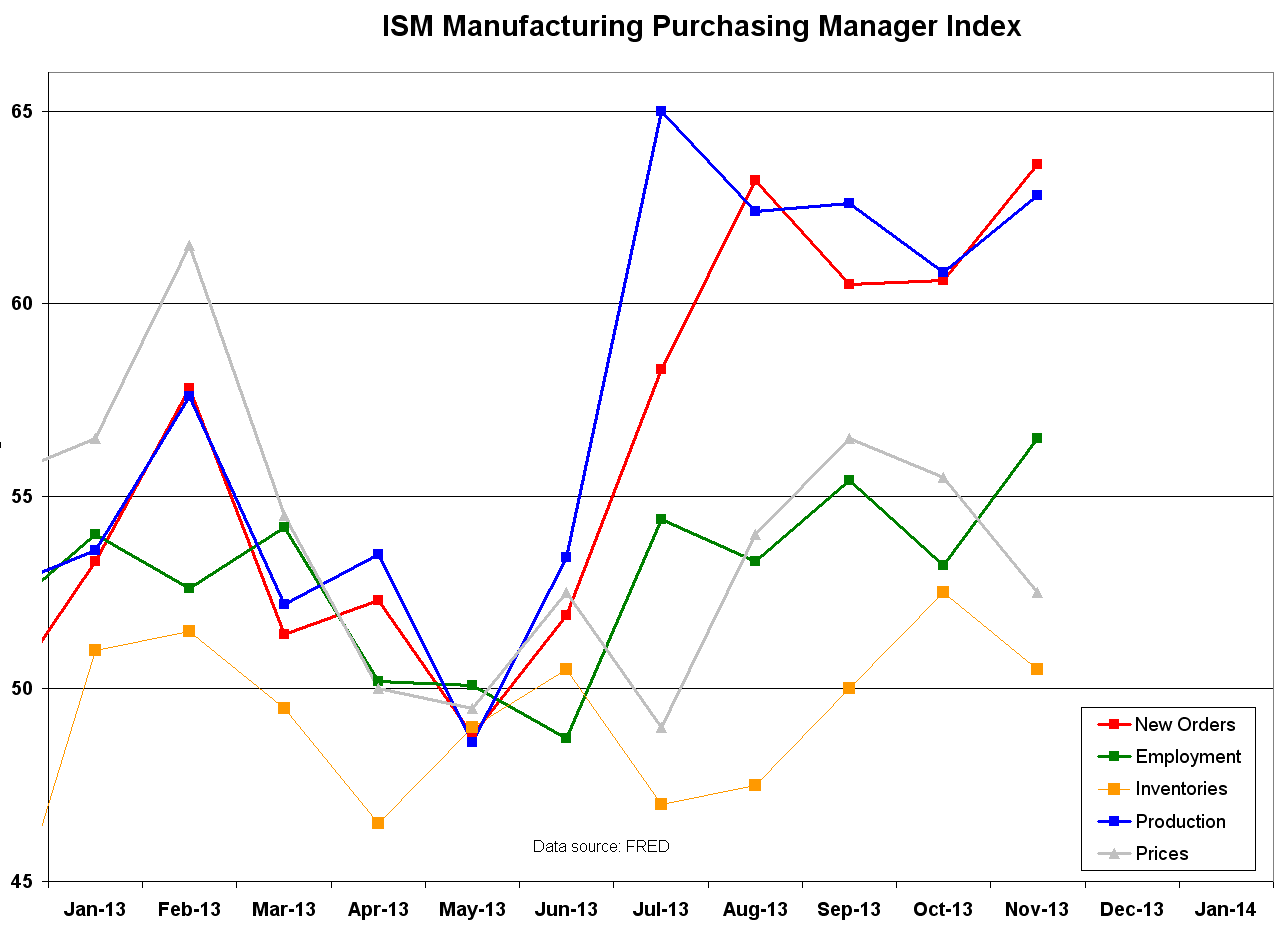

Mads Koefoed, head of macro strategy at Saxo Bank, commented the regional Chicago PMI last Tuesday, and noted that new orders and low inventories made the report strong, even though the headline figure fell from November. Much the same can be said of the national-level PMI: both production- and new orders-indices are at very high levels, while at the same time the inventories index, and even more so the customer’s inventories index (45.0 in November), are at much lower levels. Both new orders and inventories should support manufacturing in the coming months. The employment index is just now starting to move higher to catch up with production, and that is supportive of the recently announced schedule for tapering of the Federal Reserve’s asset purchases.

Of course, none of the above is something that the markets would not have figured out already, so the possibility of a negative surprise is beginning to grow. Barring a shock from outside the US, it would take plenty of time for the current positive momentum to turn, as we saw in 2010.

November’s full report from the ISM can be found here, and a good chart from Thomson Reuters showing the PMI and the annual return of stocks versus government bonds. Not surprisingly, during good times for manufacturing, stocks tend to outperform bonds. However, if the past is any guide, the difference between the returns of the two asset classes should soon start to revert to the long-run average. The Citigroup G10 economic surprise index is also quite high at the moment, which should be taken as a warning for stock bulls or bond bears.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

3 Numbers To Watch: Markit PMIs, US Jobless Claims And ISM PMI

Published 01/02/2014, 01:22 AM

Updated 03/19/2019, 04:00 AM

3 Numbers To Watch: Markit PMIs, US Jobless Claims And ISM PMI

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.