- Investors scale back bets of a March Fed rate cut

- US economic data since December point to improvement

- Focus turns to Fed meeting for clearer guidance on interest rates

- Decision on Wednesday at 19:00 GMT, press conference at 19:30 To cut in March or not to cut?

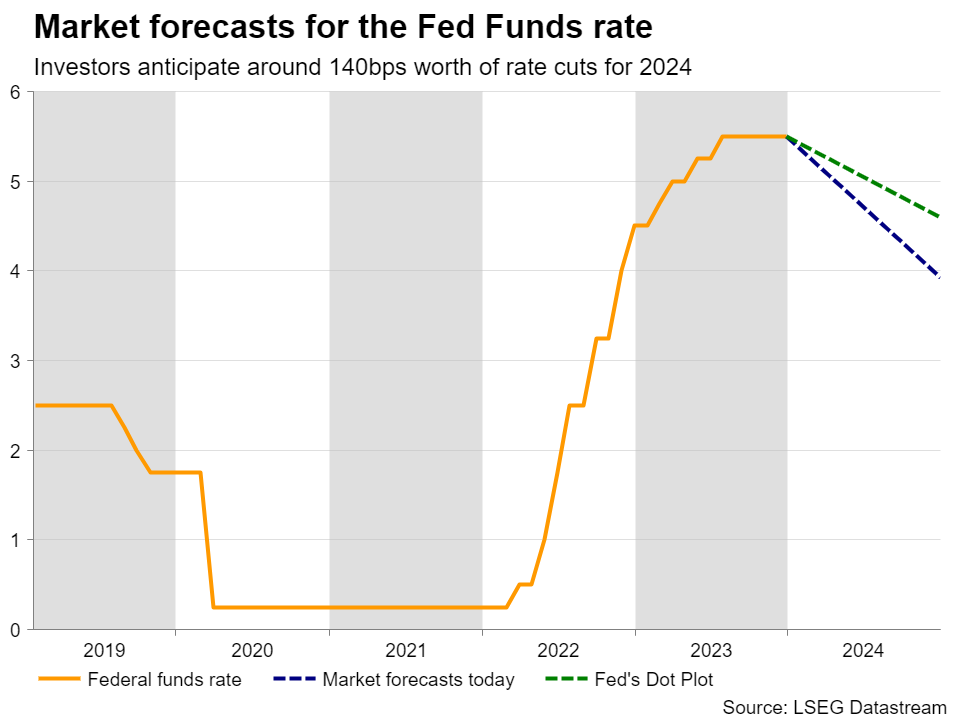

There has been a notable repricing regarding the Fed’s future course of action since the beginning of 2024. From fully pricing in a 25bps cut in March, investors are now assigning around a 50% for such a move, despite former St. Louis Fed President James Bullard recently saying that he expects the Committee to start lowering interest rates as soon as March.

It seems that the reason why investors were not particularly shocked by Bullard’s remarks was that he is not a rate setter anymore. They likely preferred to wait for Wednesday’s FOMC decision, where they could get clearer and more valid information regarding the Fed’s thinking.

Market still more dovish than the Fed

At its December gathering, the Committee revised down its interest rate projections, with the median dot for 2024 being dragged down to 4.6% from 5.1%. Yet, despite lifting their own implied path lately, market participants still expect borrowing costs to end the year lower, at around 3.93%. Perhaps their view was affected by Powell raising the question of when it may be appropriate to start lowering rates at the presser following the last meeting.

What encouraged traders to dial back some of their rate cut bets at the turn of the year may have been upside surprises in US economic data, but also remarks by Fed officials who pushed against an imminent rate reduction. Even Waller, who was the first policymaker to officially talk about the possibility of rate reductions, recently said that they should not rush into cutting interest rates until low inflation is sustained.

Data point to improving economic activity

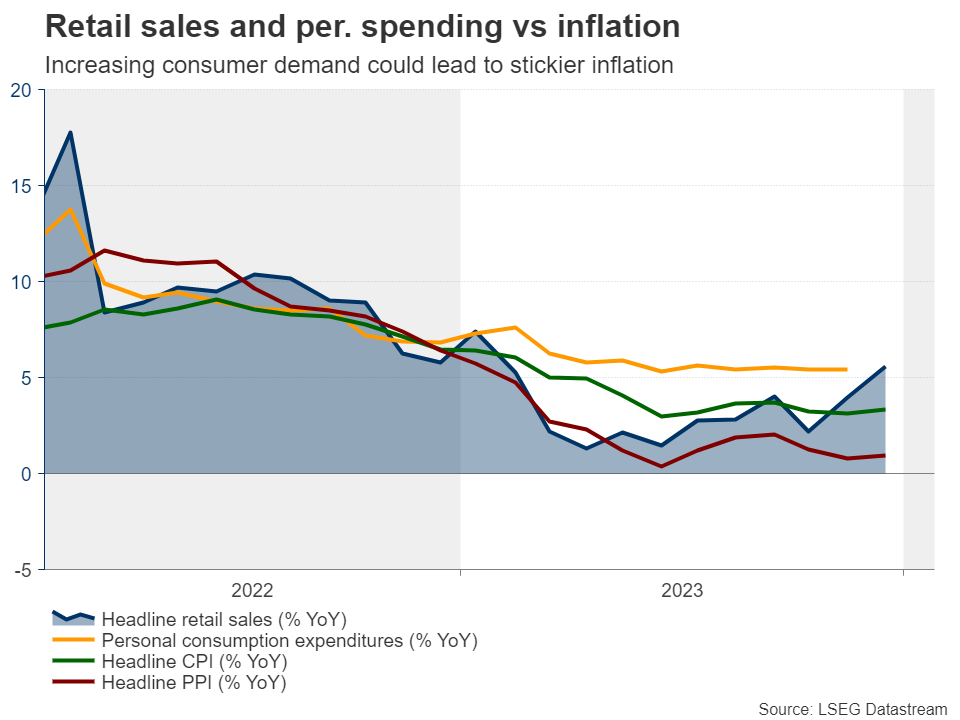

After the December gathering, the CPI report revealed that headline inflation rebounded in December, while the core rate slid by less than expected. Retail sales for the same month came in better than expected, with both the headline and core rates coming in at double their November prints, while the flash PMIs for January pointed to further improvement in business activity, with the composite index rising to 52.3 from 50.9. Adding to the bright picture, the first GDP estimate showed that the US economy grew by much more than anticipated in Q4.

With all that in mind, it seems that there is room for further upside adjustment to the market’s implied path should data and headlines continue to corroborate the view that the world’s largest economy can withstand high interest rates for longer. But will the Fed signal this when it meets on Wednesday?

Fed to stand pat, spotlight to fall on guidance

The Committee is widely expected to keep interest rates untouched and so, the big question is whether they will push back against or leave the door open to imminent rate reductions. Given that no updated economic projections will be released at this gathering, investors may seek answers in the accompanying statement and from Fed Chair Powell at the press conference. It is worth mentioning that in the minutes of the December meeting, it was noted that the future policy path will depend on how the economy evolves and that most policymakers wanted to keep borrowing costs high for “some time.”

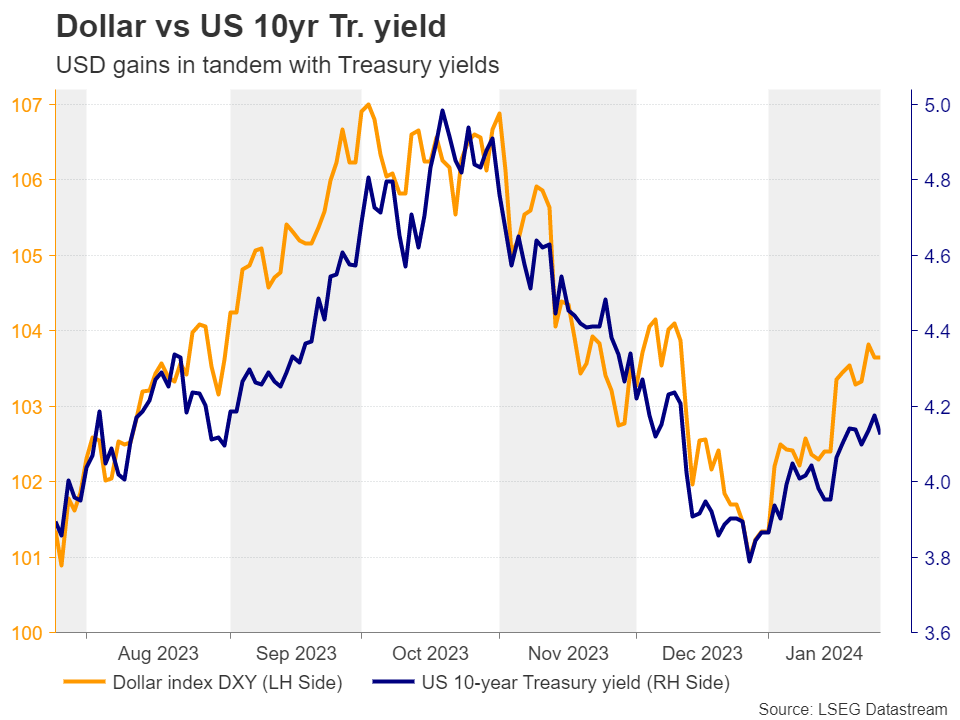

With improving economic numbers succeeding one another lately and inflation rebounding somewhat, Fed officials may not opt for rate reductions anytime soon in order not to risk letting inflation spiral out of control again. Thus, they may pour more cold water on rate cut speculation, which could allow Treasury yields to continue their recovery and thereby the US dollar to gain.

Will dollar/loonie continue trending north?

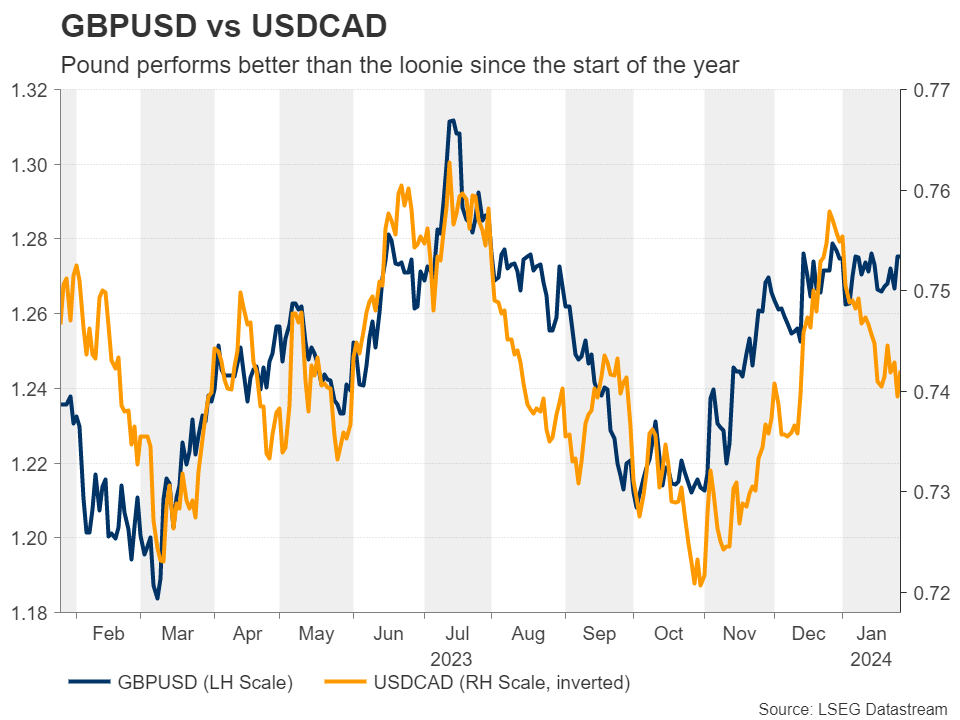

Having said all that though, with Treasury yields in some other major economies also rising and risk appetite remaining elevated, the dollar may not dominate across the board. For example, any gains against the British pound could stay limited if the BoE continues to refuse talking about rate cuts. Given the BoC’s dovish stance on Wednesday, the greenback may perform better against the loonie.

From a technical standpoint, dollar/loonie rallied after the BoC decision, but pulled back on Thursday, perhaps due to the rising oil prices. However, the pair continues to trade well above a prior downtrend line taken from the high of November 1.

A potential rebound from near the 1.3415 zone could initially aim for the recent peak of 13535, the break of which would confirm a higher high and allow extensions towards the 1.3620 territory, marked by the high of December 7.

Now, in case the Fed stresses that the rebound in inflation was solely due to base effects and that prices will slow again soon, then the market may be tempted to lift back up the probability of a March rate cut, which could result in a larger slide in dollar/loonie, perhaps towards the 1.3340 area.