Hibbett Sports, Inc. (NASDAQ:HIBB) is slated to release third-quarter fiscal 2018 results on Nov 17. The question lingering in investors’ minds is whether this sporting goods retailer will be able to deliver a positive earnings surprise in the quarter to be reported.

The company delivered a positive earnings surprise of 25% in the last reported quarter. Further, it has outperformed the Zacks Consensus Estimate by an average of 3.8% in the trailing four quarters. Let’s see how things are shaping up prior to this announcement.

What to Expect?

The current Zacks Consensus Estimate for the quarter under review is pegged at 21 cents, reflecting a decline of 68.6% from the prior-year period. Estimates have remained unchanged in the last 30 days. Moreover, analysts polled by Zacks project revenues of $217.6 million, down about 8.2% from the year-ago quarter.

Hibbett Sports, Inc. Price and EPS Surprise

Hibbett Sports, Inc. Price and EPS Surprise | Hibbett Sports, Inc. Quote

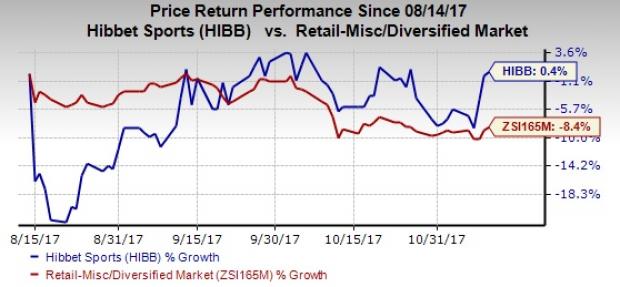

However, shares of Hibbett have improved 0.4% in the last three months, against the industry’s drop of 8.4%.

Factors at Play

While Hibbett’s bottom-line trend remains impressive, it has a dismal sales surprise history, which exhibits top-line miss in nine of the past 10 quarters. Furthermore, comparable-store sales (comps) continue to be marred by sluggish traffic, softness across all categories, increased promotional activities and difficult launch compares. Moreover, Hibbett is not immune to the challenges in the sporting goods industry.

The sporting goods industry seems to be in doldrums, as customers are jumping on the dot-com bandwagon, leaving lesser options for the brick-and-mortar retailers. Consequently, the sporting goods space has grown extremely competitive and promotional, consequently creating pressure on margins and the bottom line.

Additionally, the company substantially trimmed its guidance for fiscal 2018 due to the dismal fiscal second-quarter results and expectations of the persistence of a tough retail environment. While the company projects soft sales through the rest of the year, it now anticipates comps decline in the mid- to high-single digit range compared with the prior guidance of negative 1% to positive 1%. In addition, it envisions earnings for fiscal 2018 in the range of $1.25-$1.35 per share, down significantly from the previous forecast of $2.35-$2.55.

In addition to the soft sales trend, Hibbett is witnessing strained margins for quite a while now. This is clear from the fact that the company has witnessed reduction in gross and operating margins in the past few quarters.

Looking ahead, Hibbett anticipates gross margin to contract 250-285 bps in fiscal 2018 compared with its previous guidance of 55-75 bps reduction. Gross margin in fiscal 2018 is estimated to be hurt by increased markdowns to lower aged inventory, continuation of the highly promotional retail environment, along with persistent logistics and store occupancy deleverage stemming from lower comps. These factors make us quite apprehensive about the company’s upcoming results.

What the Zacks Model Unveils

Our proven model does not conclusively show that Hibbett is likely to beat earnings estimates this quarter. This is because a stock needs to have both a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) for this to happen. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Hibbett has an Earnings ESP of -18.70% as the Most Accurate estimate of 17 cents is pegged lower than and the Zacks Consensus Estimate of 21 cents. Further, the company currently carries a Zacks Rank #5 (Strong Sell). It should be noted that we caution against stocks with a Zacks Rank #4 or 5 (Sell rated) going into the earnings announcement, especially when the company is seeing negative estimate revisions.

Stocks Poised to Beat Earnings Estimates

Here are some companies you may want to consider as our model shows that these have the right combination of elements to post an earnings beat:

Dollar Tree Inc. (NASDAQ:DLTR) has an Earnings ESP of +2.20% and a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank stocks here.

Zumiez Inc. (NASDAQ:ZUMZ) has an Earnings ESP of +0.69% and a Zacks Rank #2.

Signet Jewelers Limited (NYSE:SIG) has an Earnings ESP of +69.09% and a Zacks Rank #2.

Will You Make a Fortune on the Shift to Electric Cars?

Here's another stock idea to consider. Much like petroleum 150 years ago, lithium power may soon shake the world, creating millionaires and reshaping geo-politics. Soon electric vehicles (EVs) may be cheaper than gas guzzlers. Some are already reaching 265 miles on a single charge.

With battery prices plummeting and charging stations set to multiply, one company stands out as the #1 stock to buy according to Zacks research.

It's not the one you think.

See This Ticker Free >>

Zumiez Inc. (ZUMZ): Free Stock Analysis Report

Dollar Tree, Inc. (DLTR): Free Stock Analysis Report

Signet Jewelers Limited (SIG): Free Stock Analysis Report

Hibbett Sports, Inc. (HIBB): Free Stock Analysis Report

Original post

Zacks Investment Research