- Recovery will be delayed until 2015

- Asia and China need quality growth

- Fixed income will be the only asset class that gives a positive return in 2014

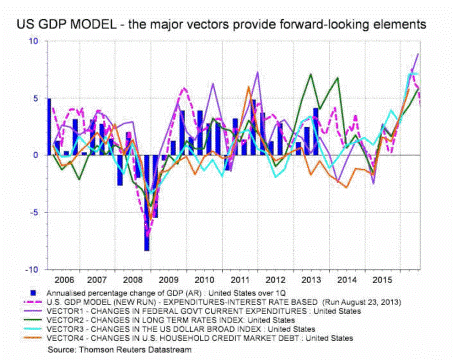

2014 started with high expectations for growth. In early January, the International Monetary Fund, World Bank and European Central Bank were falling over themselves to upgrade their growth forecasts for 2014. But now, first-quarter growth in the US is expected to come in +1.9 percent after the initial +2.6 percent forecast by the pundits in late 2014, according to a Bloomberg survey on December 12.

This is despite Q4 (the base line) being revised considerably down from 4.1 percent initially, then to 3.2 percent and ending at 2.7 percent at the final count, marking a 37 percent drop from the first to the final number). This is apparently entirely due to the weather.

But the fixed-income market seems to have a different opinion.

This is my long-term chart, which has a maximum of one signal per year, if that:

The model has been good at calling bigger trend changes, with the last one being the end of December 2012, where it bought on the close at 2.94 percent yield. It's now getting ready to sell-off, indicating that the bond market "disagrees" more and more with the weather assumption.

Furthermore, here's my gauge for central bank policy: the GDP-weighted G10 one-year interest is also making noises to the downside, although less so than long-term interest rates.

The point here is that despite hearing daily from both investors and other strategist's that "we are in clear recovery on growth and that 2014 will be a good year for stock market again", I remain extremely disappointed in the REAL PROGRESS being made in terms of structural and cyclical improvement in key indicators.

The housing market no longer supports growth: this chart shows 30-year mortgage rates inverted (down mean higher rates) versus building permits:

With the introduction of tapering – the Fed indicated less willingness to expand balance sheet – this chart shows the NET percentage change year-over-year, one year back. Looking further back will not work as it's the May 2013 tapering indication by Ben Bernanke that created the "macro impulse change".

It's still expanding the balance sheet, but the "momentum" is waning fast.

It's important for me to point out that seeing new lows in yield does not imply that I am a Super Bear on the world, as Ambrose Evans-Pritchard said in his blog the other day.

However, it does mean that I believe the recovery, or healing, will be delayed into 2015 (it's a 2015 story, not a 2014 one). Our model sees Q2 2015 as the real turning point. But more importantly, market consensus is at its highest for the least amount of real data supporting it since the crisis in 2009 (where the market was the other way around).

The world is in rebalancing mode, which hurts growth in most of the world:

• Asia and China need quality growth to substitute nominal growth on over-investment;

• The US current account is falling mainly due to less energy imports, leaving a massive "hole in the ground on consumption" for the rest of world;

• Europe has not even started to address its fundamental lack of reforms. Presently, Europe is trying to sell implications of low interest rates as a recovery, a similar mistake that was made in Australia.

Low rates are there for a reason or, rather, two:

1. Low growth and no visibility for improvement in business investment and consumer demand;

2. Deflationary forces because of a lack of technology/innovation (read my Q2 forecast here) and a global depression.

If the recovery was real and deeply rooted, unemployment would be dropping, businesses would be investing in further capacity and, most certainly, the consumer would be buying goods. No, the bond market remains the most steady hand of all markets and assets and my conclusion remains the same.

Fixed income will be the only asset class that gives a positive return in 2014, leading to both inflation and growth from Q2 2015. As our rule of thumb, there is a nine-month lag from interest to the real economy, which means that the low rates seen over this summer will be positive for Q2 2015.

The world is barely growing at zero policy interest. If anything, the disinflation says lower growth is coming, so the path of least resistance is lower rates first as policymakers continue to believe "guidance on interest rates" is more important than real changes.