It’s the turn of the RBNZ to decide on monetary policy this week. We don’t expect any policy action at this gathering, but we do expect officials to reiterate concerns over Kiwi’s appreciation. The UK GDP is forecast to show that the UK economy tumbled 20.9% qoq, but we don’t expect such a print to prove determinant with regards to the BoE’s future policy plans. Australia’s employment data for July is coming out, with the forecasts pointing to softer numbers than in June.

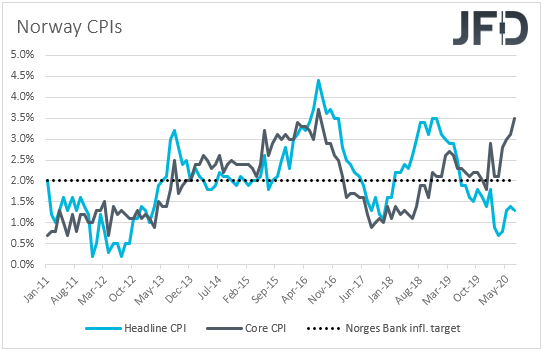

On Monday, the calendar is relatively empty with the only releases worth mentioning being China’s CPI and PPI for July, and Norway’s inflation data for the same month, both of which are already out. China’s CPI rebounded 0.6% yoy after sliding 0.1%, beating estimates of a 0.4% rebound. The nation’s PPI rate increased to -2.4% yoy from -3.0%. With regards to the Norwegian data, the headline CPI rate ticked down to +1.3% yoy from +1.4%, but the core one rose to +3.5% yoy from +3.1%, beating estimates of a slide to +3.0%.

At its latest gathering, the Norges Bank kept interest rates unchanged at 0.0%, repeating that they will stay at that level for some time ahead. Officials appeared somewhat more optimistic than previously, saying that since the prior meeting, activity has picked up faster than expected, the unemployment has fallen more than anticipated and oil prices have risen. Oil prices are now slightly higher than they were back then, while the unemployment rate for June declined to 4.3% from 4.6%. Thus, with core inflation accelerating in July, Norges Bank policymakers may feel comfortable staying on the sidelines for a while more, and reiterating their sanguine language.

On Tuesday, during the Asian morning, we have Australia’s NAB business survey for July. This release is not a major market mover, but given the emphasis of the RBA to the labor market, we would like to take a close look to the labor costs index, which rebounded +0.1% qoq in June, from -0.9% qoq in May. What may be more important for AUD-traders may be the wage price index for Q2 and the employment data for July, due out to be released on Wednesday and Thursday respectively. That said, this currency has been mostly linked to developments surrounding the broader market sentiment in last months, and thus, we expect the aforementioned releases to only result in intraday fluctuations rather than trend-determinant movements.

During the European morning, the UK employment report for June is due to be released. The unemployment rate is forecast to have risen to 4.2% from 3.9%, while average weekly earnings including bonuses are expected to have declined 1.2% yoy after sliding 0.3% in May. The excluding-bonuses rate is also expected to have fallen, to -0.1% yoy from +0.7%. The case for a weak report is supported by the KPMG and REC, UK Report on Jobs for the month, in which it was noted that starting pay for both permanent and short-term staff fell further in June as demand for workers remained weak and labor supply continued to increase.

From Germany, we get the ZEW survey for August. The current conditions index is expected to have increased to -68.8 from -80.9, but the economic sentiment one is anticipated to have slid to 58.0 from 59.3. This suggests that analysts’ opinions with regards to the current performance of the German economy have improved following the agreement between Eurozone’s members over a coronavirus-related rescue fund, but fears over a second wave of infections in Europe may have raised questions with regards to the future. The euro skyrocketed in the aftermath of the deal over the rescue package, but another round of accelerating infections may be the trigger for a decent downside correction.

Later in the day, Canada’s housing starts and the US PPIs, both for July, are coming out. Canada’s housing starts are forecast to have slowed somewhat, while the US PPI headline rate is forecast to have ticked up to -0.7% yoy from -0.8%. The core rate is expected to have rebounded to +0.1% yoy from -0.3%.

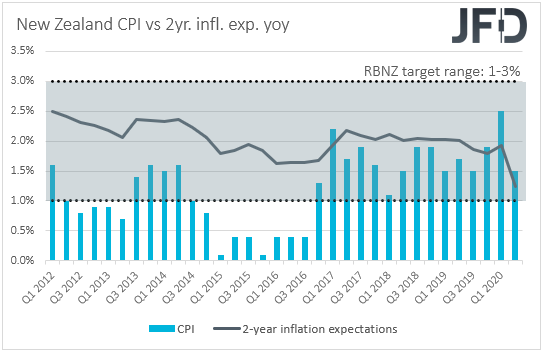

On Wednesday, during the Asian morning, the spotlight is likely to fall on the RBNZ monetary policy decision. At its previous gathering, the RBNZ decided to keep interest rates and its Large-Scale Asset Purchase (LSAP) program unchanged, with officials noting that their nation has contained the spread of the virus, enabling an earlier resumption of economic activity than assumed in May. However, they highlighted that the appreciation of their local currency has placed further pressure on exports and that the balance of economic risks remains to the downside, adding that they remain willing to ease their policy further if deemed necessary.

In Q2, inflation slowed in New Zealand, to +1.5% yoy from +2.5% yoy, but this is still higher than the Bank’s own forecast for the quarter, which was at +1.3% yoy. Thus, this may allow RBNZ officials to stand pat for another meeting, but with the Kiwi slightly higher against the dollar than it was the last time they met, we also expect them to reiterate concerns over its appreciation, as well as their readiness to ease further if needed.

From Australia, we get the wage price index for Q2. Wages in Australia are expected to have slowed to +0.3% qoq from +0.5%, something that will bring the yoy rate down to +1.9% from +2.1%. That said, bearing in mind that the qoq rate of the NAB labor costs index has risen to +0.1% qoq in June from -0.8% in March, we would consider the risks surrounding the wage price index as tilted to the upside.

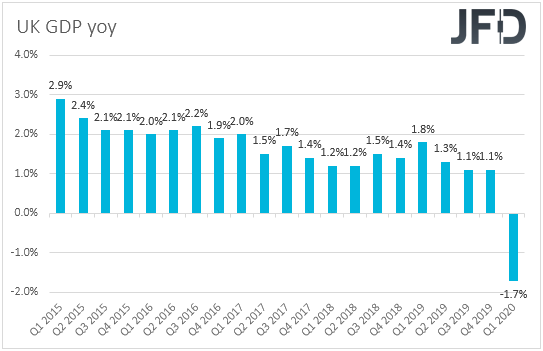

Ahead of the EU open, we have the 1st estimate of the UK GDP for Q2, as well as the industrial and manufacturing production rates for June. Economic activity in the UK is anticipated to have tumbled 20.9% qoq in the three months to June, which following the 20.4% mom tumble in April alone is unlikely to come as a surprise. Both the IP and MP mom rates re expected to have risen to +9.4% and +10.0% from +6.0% and +8.4% respectively, something that will drive the yoy rates up to -13.1% and -15.0% from -20.0% and -22.8%.

At last week’s gathering, the BoE kept its policy unchanged and although it highlighted that the economic outlook remains uncertain, it upgraded its GDP forecast for this year, but with the condition that the direct impact of the pandemic on the economy will dissipate gradually over the forecast period. In the quarterly Monetary Policy Report, officials discussed the effectiveness of negative interest rates and noted that they will continue to monitor their appropriateness. That said, we don’t expect a round of bad economic data this week to increase speculation that the Bank could adopt negative rates soon. After all, officials kept policy unchanged last week, after noting that economic activity is likely to fall more than 20% in Q2, and that the unemployment rate is projected to rise materially by the end of the year. We prefer to pay more attention to data regarding Q3 before we start examining whether officials will consider negative rates at some point in the foreseeable future.

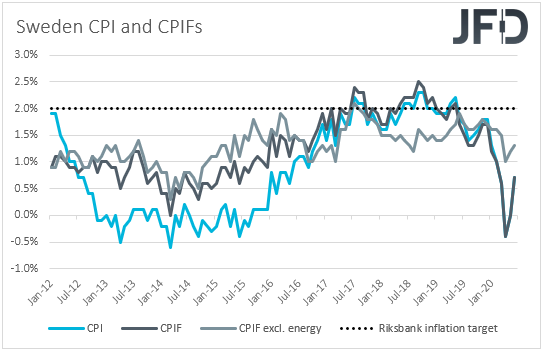

From Sweden, we have the CPIs for July. Both the CPI and CPIF rates are expected to have declined to +0.5% yoy and +0.4% yoy respectively, after both sitting at 0.7% yoy in June. That said, as it is always the case, we prefer to pay more attention to the core CPIF metric, which excludes the volatile items of energy. That rate stood at 1.3% in June.

At its latest gathering, the Riksbank decided to extend its framework for its asset purchases from SEK 300bn to SEK 500bn, up to the end of June 2021, while it announced that in September, it will start purchasing corporate bonds. The Board also decided to cut interest rates and extend maturities on lending to banks, despite keeping the repo rate unchanged at 0%. We believe that a potential slowdown in core inflation is unlikely to prompt additional action at the Bank’s upcoming gathering, but it may keep officials willing to do so if the situation continues to worsen.

From the Eurozone, we get industrial production data for June. Expectations are for a small slowdown, to +10.0% mom from +12.4%. However, this would still be a decent monthly rate as it would drive the yoy rate up to -11.6% from -20.9%.

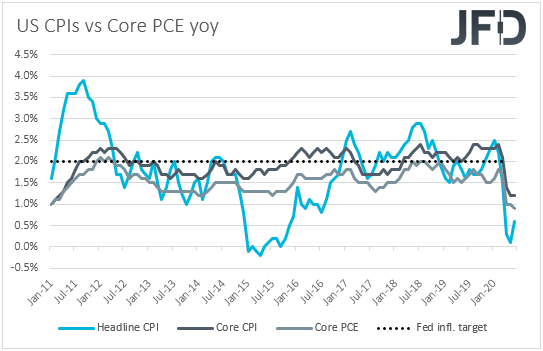

Later in the day, the US CPIs for July are coming out. The headline rate is anticipated to have increased to +0.8% yoy from +0.6%, while the core one is expected to have held steady at +1.2%. Although this could lessen somewhat the probability for the Fed to expand its stimulative efforts, all the attention in the US is likely to stay on whether the Congress can eventually reach consensus on a coronavirus-aid package.

Discussions fell apart on Friday, which prompted President Trump to sign executive orders and memorandums aimed at unemployment benefits, evictions, student loans and payroll taxes. However, details on how the measures could be funded remain unclear and Democrats have already warned that such orders are legally dubious and may be challenged in court. In any case, on Sunday, House Speaker Nancy Pelosi and Treasury Secretary Steven Mnuchin said they are open to restarting talks.

Tensions between the US and China have also escalated, with Trump unveiling sweeping bans on Chinese tech firms TikTok and Tencent. Up until now, risk sentiment remained broadly immune to those developments, but it remains to be seen whether this will be the case this week as well. If so, a potential accord in the US Congress may prove positive for investors’ morale, pushing equities further up and safe havens down.

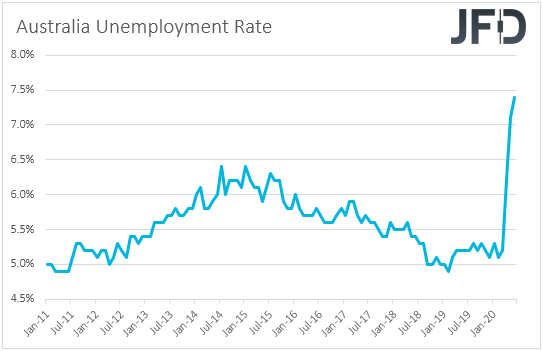

On Thursday, the highlight may be Australia’s employment report for July, due out during the Asian morning. The unemployment rate is forecast to have risen to 7.8% from 7.4%, while the net change in employment is anticipated to show that the economy has added 40.0k jobs after gaining 210.8k in June.

At last week’s gathering, the RBA kept its targets for the cash rate and the yield on 3-year government bonds unchanged at 0.25%, noting that the Bank’s mid-March package of support is working as expected. What’s more, officials noted that even though the worst of this contraction has now passed, the outlook remains highly uncertain and that the recovery will be dependent on the containment of the virus. With the Bank also noting that in its baseline scenario, the unemployment rate is likely to rise to around 10% later this year, we don’t expect a rise to 7.8% to come as a surprise to policymakers. Thus, we don’t expect this report to prove a game-changer with regards to the RBA’s plans. Even if the Aussie slides somewhat on a weak report, we would treat such a slide as a corrective move of the currency’s overall uptrend. As we already noted, we expect the Aussie to stay mostly linked to developments surrounding the broader market sentiment, and if the risk-on trading continues, its uptrend is likely to continue as well, especially against safe-haven currencies, like the dollar and the yen.

As for the rest of Thursday’s data, Germany’s final CPIs for July and the US initial jobless claims for last week are coming out. As it is always the case, Germany’s final CPIs are expected to confirm their preliminary estimates, while the US initial jobless claims are forecast to have slowed slightly, to 1.140mn from 1.186mn the week before.

Finally, on Friday, in Asia, China’s industrial production, fixed asset investment, and retail sales, all for July, are due to be released. Industrial production is forecast to have slowed somewhat, to +4.7% yoy from +4.8%, while fixed asset investment is forecast to have fallen 3.3% yoy after sliding 3.1% in June. Retail sales are anticipated to have rebounded 0.3% after falling 1.8%.

During the European morning, Eurozone’s employment change and the second estimate of the bloc’s GDP, both for Q2, are coming out. No forecast is available for the employment change, while the second GDP estimate is expected to confirm the initial forecast of -12.1% qoq.

Later, from the US, we get retail sales for July, industrial production for the same month, and the preliminary UoM consumer sentiment index for August. Both headline and core sales are forecast to have slowed to +1.8% mom and +1.6% mom from +7.5% and +7.3% respectively, while industrial production is anticipated to have slowed to +3.0% mom from +7.2%. The UoM consumer sentiment index is expected to have declined fractionally, to 72.0 from 72.5.