This week seems to not be as busy as the previous one in terms of releases on the economic agenda, but still, we do get some top-tier events. The highlight may be the Jackson Hole Economic Symposium, from which we may get information as to when Fed officials may start withdrawing policy support. The preliminary PMIs for August from the Eurozone, the UK and the US are also coming out, while on Thursday, the ECB releases the minutes of its latest policy gathering.

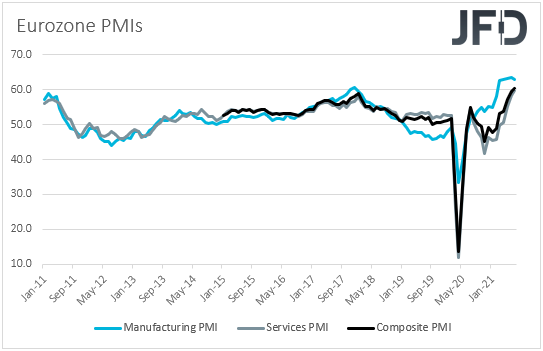

On Monday, the most important releases on the agenda may be the preliminary PMIs for August from the Eurozone, the UK, and the US. Both Eurozone’s manufacturing and services PMIs are forecast to have declined to 62.0 and 61.0, from 62.8 and 61.8 respectively, which could take the composite index down to 59.7 from 60.2. With the Delta variant still spreading fast across the continent, a slight slowdown appears more than normal to us, and – to be honest – we don’t expect the euro to fall much at the time of the release, if the actual numbers come close to their forecasts. After all, the ECB has already turned more dovish, by changing its forward guidance to hint that interest rates are likely to stay low for longer than the previous one suggested. What’s more, EUR traders may refrain from adjusting their positions and perhaps wait for the ECB minutes, due out on Thursday, for more information with regards to the ECB’s future plans.

No forecast is available for the UK prints. So, it remains to be seen whether a similar to Eurozone’s slowdown will hurt the pound. Last week, the pound tumbled against the greenback at a time when the financial world turned to risk off due to concerns over the spreading of the Delta coronavirus variant. Perhaps market participants consider the pound as a risk-linked currency due to the UK’s large current account deficit. That said, at its latest gathering, the BoE lowered the threshold of when they will start reducing their stock of bonds, which could mean that QE tapering may start earlier than previously anticipated. Therefore, this is likely to keep the pound in a relatively better position compared to risk-linked currencies the central banks of which are forecast to stay dovish for longer. One clear example among the majors is the Aussie, as RBA officials have clearly signaled that interest rates in Australia are likely to stay at present levels at least until 2024. In other words, although GBP/USD could drift south for a while more, we would expect GBP/AUD to continue trending north.

As for the US, expectations are for small declines there as well, but we don’t believe that this will be enough to reshape market expectations around the Fed’s future course of action. We believe those concerned with that will lock their gaze on the Jackson Hole Economic Symposium, scheduled for Thursday, Friday, and Saturday.

On Tuesday, during the Asian session, New Zealand’s retail sales for Q2 are due to be released, but no forecast is available. At last week’s gathering, the RBNZ delayed raising interest rates, at a time when the financial community was more than certain for such a move. Policymakers changed their minds after the nation entered a lockdown due to new coronavirus cases, however, they signaled that they still expect to push the hike button before year end. The Bank’s next gathering is scheduled for Oct. 6, and decent retail sales numbers could add to the likelihood of a hike then.

Later in the day, we get Germany’s final GDP for Q2, which is expected to confirm its preliminary estimate, and the US new home sales for July, which are expected to have increased somewhat.

On Wednesday, Asian time, New Zealand’s trade balance for July is coming out, but no forecast is available. During the EU session, we have Germany’s Ifo survey for August, and later, the US durable goods orders for July. With regards to the Ifo numbers, the current assessment index is anticipated to have inched up to 100.8 from 100.4, but the expectations one is forecast to have slid to 100.0 from 101.2. This is likely to take the business climate index down to 100.4 from 100.8. As for the US durable goods, headline orders are forecast to have declined 0.2% mom after rising 0.9% in June, while the core rate is expected to have held steady at +0.5%.

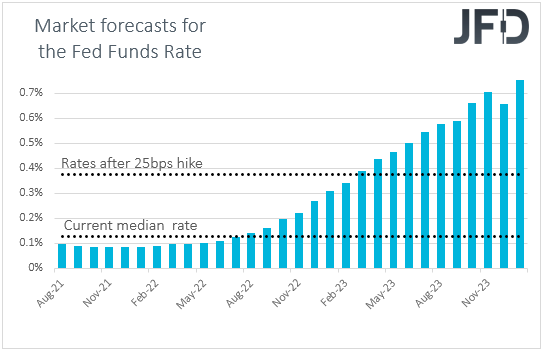

On Thursday, the Fed’s annual Economic Symposium will kick off, but it would be held online instead of at its usual location in Jackson Hole, Wyoming. The highlight is likely to be a speech by Fed Chair Jerome Powell, scheduled on Friday, from whom market participants may get extra information as to when he and his colleagues are planning to start withdrawing monetary policy support.

At the latest gathering, the FOMC kept its policy unchanged, but although officials repeated that they will keep the pace of their QE purchases unchanged until “substantial further progress has been made” towards their goals, they added that the economy has made such progress, and that they will continue to assess the progress in coming meetings. Having said all that though, at the press conference following the decision, Fed Chief Powell said that the labor market has still a long way to go, and that inflation is still expected to fall back to their longer-run goals. He also added that the timing of taper will depend on incoming data and that they will provide advance notice before any changes, something that may have poured cold water on expectations of an early tightening.

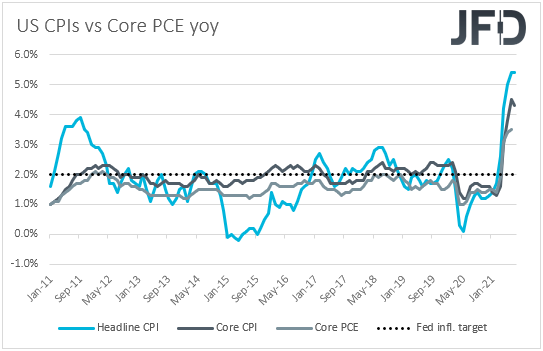

Since then though, several Fed officials, including Vice Chair Richard Clarida, expressed a more hawkish view than Powell did, while the employment report for July came in stronger than anticipated. All this may have revived speculation for early tapering by the Fed, perhaps as early as next month. The July CPIs slowed somewhat on a mom basis, but the PPIs for the month accelerated further, suggesting that inflation may have not hit a ceiling yet. On top of that, last week, the minutes of the latest gathering revealed that officials largely expect to reduce their monthly bond buying later this year. Therefore, it would be interesting to see whether the Fed Chief has changed his mind or not. Investors may be eager to find out whether indeed the Fed is planning to start its tapering process soon, and if so, what would be the reduction pace. Currently, the Fed is buying $120bn worth of assets per month. So, a $20bn taper means that the program will end in six months, and thereby allow even earlier rate hikes, while withdrawing only half of that amount would take a full year.

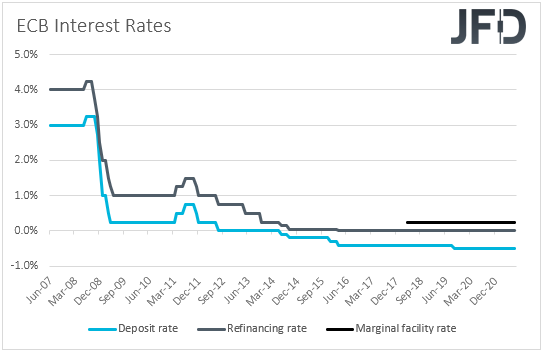

Another event that may attract some attention on Thursday may be the minutes of the latest ECB meeting. At that meeting, the Bank kept all of its settings untouched and changed its forward guidance, saying that it will keep interest rates at present or lower levels until it sees inflation reaching 2% well ahead of the end of its projection horizon, which may also imply a period during which inflation moderately overshoots that objective. As we already noted, this translates into willingness to hold rates low for much longer than the previous guidance suggested. With that in mind, we don’t expect to get any major new information from the minutes, but we will look for any possible hints with regards to officials’ plans over their asset purchase program beyond March, the current planned end date.

We also get the second estimate of the US GDP for Q2, which is expected to be revised up to +6.7% qoq SAAR from +6.5%. That said, with all eyes locked on the Fed’s Economic Symposium, we see the case for the GDP to receive little, if any, attention.

Finally, on Friday, Asian time, we have the Tokyo CPIs for August. No forecast is available for the headline rate, while the core one is anticipated to have ticked up to -0.2% yoy from -0.3%.

Later in the day, in the US, the personal income and spending numbers for July are coming out, alongside the core PCE index for the month. Personal income is anticipated to have accelerated marginally, to +0.2% mom from +0.1%, while the spending rate is expected to have fallen to +0.3% mom from +1.0%. As for the core PCE index, no forecast is available. The preliminary UoM consumer sentiment index for August is also due to be released and the forecast points to a rise to 70.9 from 70.2.