Market participants are likely to pay extra attention to the minutes from the latest FOMC and ECB gatherings, as they try to figure out how policymakers of those two major central banks plan to move forwards. That said, ahead of those releases, during the Asian morning Tuesday, the RBA is scheduled to decide on policy, with the attention probably fixed on whether officials will consider further bond purchases.

Monday appears to be a relatively light day in terms of economic data releases. The most important ones are the services and composite PMIs for June from the Eurozone and the services and composite from the UK. US markets will stay closed in celebration of the Independence Day.

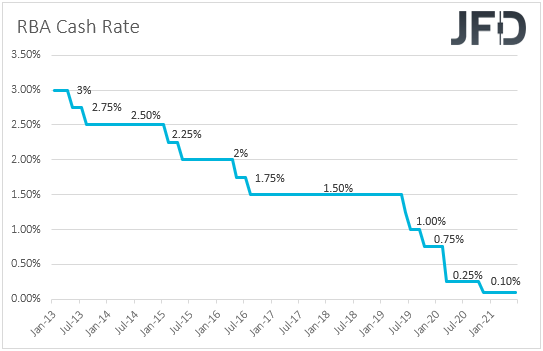

On Tuesday, during the Asian session, the RBA decides on monetary policy. At its June meeting, this Bank decided to keep its policy settings untouched and reiterated that at the July meeting, it will consider further bond purchases. In the minutes of that meeting, it was revealed that officials’ decision will depend upon the Board’s goals for employment and inflation, as well as the likely effect of different options on the overall financial conditions.

Since the release of the minutes, the only top-tier data point we got from Australia was the employment report for May. The unemployment rate slid to 5.1% from 5.5% while the employment change revealed that the economy has added 115.2k jobs during the month, much more than the 30.0k forecast. The strong employment report may have lessened the chances for the RBA to expand its QE purchases at this gathering, but with inflation standing at +1.1% yoy, well below the lower end of the Bank’s target range of 2-3%, the door remains open. The Aussie could strengthen if they refrain from announcing more bond purchases, while the opposite may be true if they do.

During the European session, we have Germany’s ZEW survey for July and Eurozone’s retail sales for May. Germany’s current conditions ZEW index is expected to have rebounded to +5.0 from -9.1, but the economic sentiment one is anticipated to have declined to 75.4 from 79.8. As far as Eurozone’s retail sales for May are concerned, they are expected to have rebounded 4.1% mom after sliding 3.1%.

Later in the day, in the US, the final Markit services and composite PMIs for June, as well as the ISM non-manufacturing index for the month, are due to be released. The final Markit prints are expected to confirm their preliminary estimates, while the ISM index is forecast to have declined to 63.5 from 64.0.

On Wednesday, the main event on the financial agenda may be the minutes from the latest FOMC monetary policy meeting, when the Committee appeared much more hawkish than market participants may have expected. Although officials kept policy unchanged, they signaled that interest rates are likely to start rising in 2023. Since then, we’ve heard the individual views of several policymakers, with some of them supporting that interest rates should even start rising during 2022, and others arguing against withdrawing monetary policy support too soon.

With that in mind, we will scan the minutes to see where the majority of members leans to, and what is the consensus with regards to QE. Remember that, at the press conference following the decision, Chair Powell said that there had been a first discussion about when to start withdrawing QE, but added that the talks will continue in the coming months as the economy continues to heal. With that in mind, anything pointing towards a first tapering move in the months to come, could support the US dollar further, and perhaps hurt equities somewhat.

Besides the minutes from the latest FOMC gathering, we have New Zealand’s NZIER business confidence for Q2 during the Asian morning, as well as the US JOLTs Job Openings for May and Canada’s Ivey PMI for June, due out later in the day.

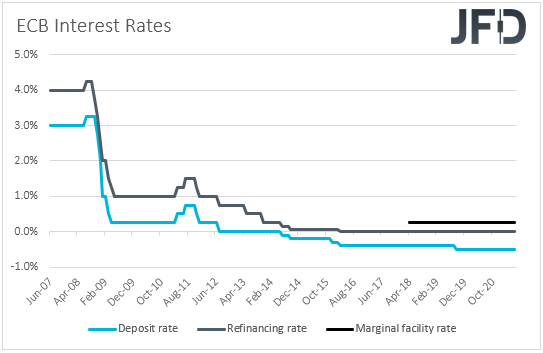

On Thursday, we get more meeting minutes, this time from the ECB. In June, the Bank decided to keep all its monetary policy settings unchanged, noting that its PEPP (Pandemic Emergency Purchase Programme) will continue to run at a “significant higher pace”. The Bank raised its 2021 and 2022 GDP and inflation forecasts, but at the press conference following the decision, ECB President Lagarde clarified that headline inflation will remain below target over the forecast horizon. She admitted that they were somewhat more optimistic about the economic outlook than three months ago, but highlighted that the decision statement was unanimously supported, suggesting that tapering is not on any official’s mind at the moment.

That said, recently, Governing Council member Jens Weidman said that “inflation is not dead” and that he wants to discuss when emergency ends from a monetary policy point of view. He believes that running a pandemic emergency plan after the pandemic is over isn’t honest. Weidmann’s remarks are certainly more hawkish than those of Lagarde, Lane and Panetta, who agree that monetary and fiscal policy support should not be withdrawn prematurely, but he is the only one who expressed such a view until now. So, with all that in mind, we don’t believe that the minutes will reveal a different message than the one we got from the meeting. A confirmation of the ECB’s dovish stance could weigh on the euro, especially against the US dollar, which has been performing very well lately.

As for the rest of Thursday’s events, the only one worth mentioning is Germany’s trade balance for May, with the nation’s trade surplus expected to stay at EUR 15.9bn.

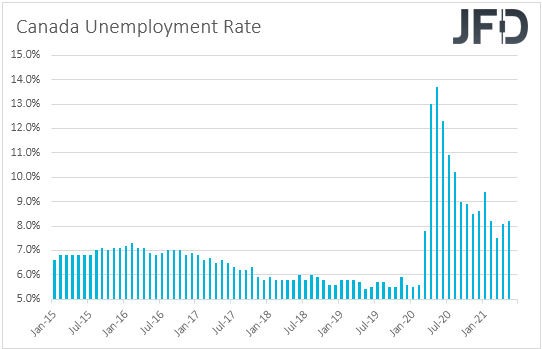

Finally, on Friday, the most important data set may be Canada’s employment report for June. The unemployment rate is anticipated to have declined to 7.8% from 8.2%, while the net change in employment is forecast to reveal that the economy has added 175.0k jobs, after losing 68.0k in May.

At their latest gathering, BoC policymakers kept their monetary policy settings unchanged and noted that any adjustments to the pace of their QE purchases will be guided by the ongoing assessment of the strength and durability of the economic recovery. In our view, the absence of strong hints with regards to further tapering in the upcoming months may have disappointed some Loonie traders, but a strong employment report may revive speculation that more tapering could be on the cards for the months to come, and thereby encourage some CAD-buying.

Ahead of Canada’s jobs report, during the Asian session, China’s CPI and PPI for June are due to be released. The CPI rate is forecast to have ticked up to +1.4% yoy from +1.3%, while the PPI one is anticipated to have slid to +8.8% yoy from +9.0%.

Later, during the early EU session, the UK monthly GDP for May is coming out, alongside the industrial and manufacturing production rates, as well as the trade balance for the month. No forecast is available for the GDP, while both the IP and MP rates are expected to have rebounded back to the positive territory. As for the nation’s trade deficit, it is expected to have widened to GBP 11.10bn from GBP 10.96bn.