Following last week’s RBA monetary policy decision, this week, the central bank torch will be passed to the ECB and the BoC. We don’t expect any change from neither Bank, and thus, if this is the case, the attention may fall on hints and clues with regards to their future plans.

Investors may also pay extra attention in the US CPIs for May, where another surge in both the headline and core rates may increase speculation for the Fed to start scaling back its monetary policy support sooner than previously thought.

Monday is a very light day with no top tier indicators on the schedule. Therefore, market participants may focus on US politics and the negotiations between Democrats and Republicans over President Joe Biden’s proposed USD 1.7trln infrastructure deal. Expectations of government spending on infrastructure has already added fuel to the recent stock market rally, and thus, it would be interesting to see what the outcome could be. In our view, the large stock gains on expectations of a large government spending may have left stocks vulnerable to a decent pullback in case the final decision does not point to such a big plan.

On Tuesday, during the Asian session, we have Japan’s final GDP for Q1, which is expected to be revised fractionally up, to -1.2% qoq from -1.3%. Australia’s NAB business survey for May is also coming out, but no forecast is currently available.

During the EU trading, Germany’s ZEW survey for June is due to be released. The current conditions index is forecast to have risen to -28.0 from -40.1, while the expectations one is anticipated to have inched up to 85.3 from 84.4. Eurozone’s final GDP for Q1 is also coming out, alongside the final employment change for the quarter. As it is usually the case, the final prints are expected to confirm their preliminary estimates.

Later in the day, we get Canada’s trade balance for April and the US JOLTs job openings for the same month. Canada’s trade deficit is expected to have narrowed somewhat, while no forecast is available for the US JOLTs number.

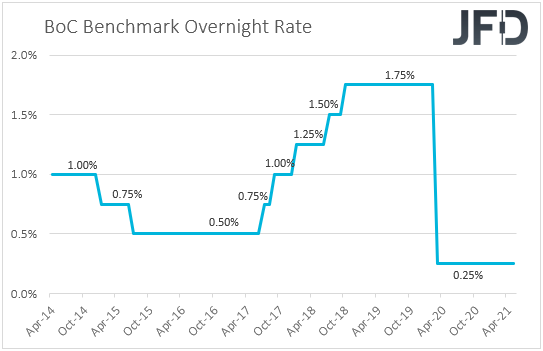

On Wednesday, the main event is likely to be the BoC interest rate decision. At its latest meeting, this Bank kept its benchmark interest rate unchanged at +0.25%, but decided to scale back its QE purchases. Since then, both the headline and core CPI rates for the month of April surged, and although the GDP slowed in the first quarter of the year, the expansion accelerated notably in March. However, on Friday, the employment report for May showed that the unemployment rate ticked up to 8.2% from 8.1%, and that the economy has lost 68.0k more jobs after losing 207.1k in April.

Thus, although the spike in the CPIs and the decent GDP data may dismiss questions as to whether the Bank has acted correctly in scaling back its bond purchases at the last gathering, the soft employment report is unlikely to lead to more tapering at this meeting. That said, an upbeat tone in the statement, hinting that further tapering may be in the works for the months to come may be enough to keep the Loonie on the front foot for a while more.

As for Wednesday’s data releases, during the Asian session, we get China’s CPI and PPI for May, both of which are expected to have risen to +1.6% yoy and +8.5% yoy respectively, from +0.9% and +6.8%. Germany’s trade balance for April is also coming out, and the forecast points to some increase in the nation’s surplus.

On Thursday, the highlights are likely to be the ECB policy decision and the US CPIs for May.

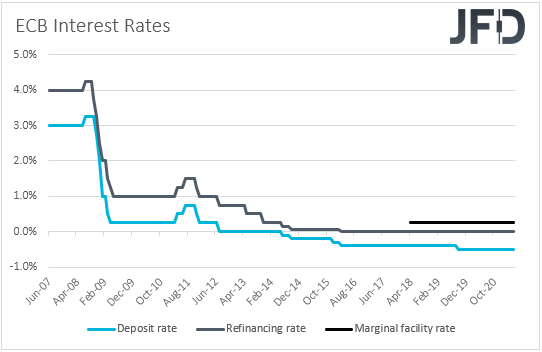

Getting the ball rolling with the ECB, when they last met, officials of this Bank kept their policy settings untouched, while there was not much new material information in the statement accompanying the decision. What’s more, according to sources, policymakers did not discuss plans with regards to their bond purchases at all.

Since that meeting though, a surge in inflation, especially in the US, has been the main theme for the financial markets, adding to speculation that the Fed may soon need to start scaling back its monetary policy support. In the Eurozone, headline inflation rose to +2.0% yoy, but the core rate increased only to +0.9% yoy from +0.7%, adding some credence to the view that the spike in headline inflation may be due to transitory factors. With that in mind, investors may be looking for hints as to what are the Bank’s future plans in terms of monetary policy.

Recently, ECB Chief Economist Philip Lane has pushed against the inflation-is-back narrative, adding that markets will take years to return to pre-crisis levels and that stimulus is still needed to secure the recovery. On top of that, ECB President Christine Lagarde said that it is “essential that monetary and fiscal support are not withdrawn too soon”.

Therefore, we expect the Governing Council to keep its policy extra loose and avoid any tapering talks. On the contrary, there may be a debate on whether to prolong their support, a decision that will depend on how strong officials believe the economic recovery is, something we will get clues on from the updated economic projections.

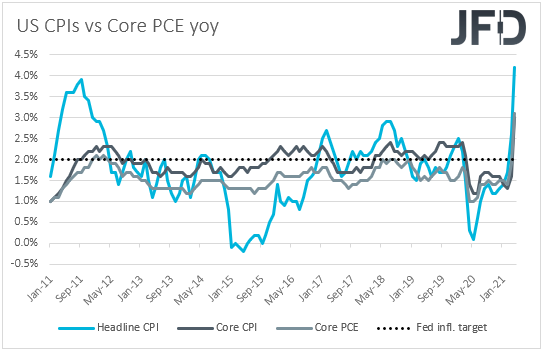

Now, passing the ball to the US and its CPIs for May, both the headline and core rates are expected to have climbed even higher, to +4.7% yoy and +3.4% yoy from +4.2% and +3.0% respectively. In contrast to the Eurozone, here, the surge in the core rate well above the Fed’s target of 2% suggests that the inflation spike may not be due to transitory factors. Even the core PCE rate, which is the Fed’s favorite inflation metric, jumped to +3.1% yoy in April from +1.9% yoy. With several Committee members already talking about the need to have a tapering discussion in the upcoming meetings, this may increase speculation that the Fed will have to start normalizing its monetary policy sooner than previously thought, and may result in a pullback in equity markets and other risk-linked assets. At the same time, the US dollar and other safe havens could come under buying interest.

Finally, on Friday, GBP-traders are likely to focus on the UK monthly GDP for April, as well as the industrial and manufacturing production rates for the month. While no forecast is available for the GDP, both the IP and MP rates are expected to have declined to +1.2% mom and +1.5% mom from +5.8% and +2.1% respectively.

That said, this will send the yoy rates skyrocketing to +30.2% and +42.0%. In our view, decent data combined with a strong vaccination rollout pace in the UK may keep the pound relatively supported in the short run. However, the economic recovery in the UK is likely to face a real test in the coming weeks as there is likely to be a delay in the planned reopening due to concerns surrounding the new “Delta” coronavirus variant, first detected in India.

Later in the day, from the US, we get the preliminary UoM consumer sentiment index for June. Expectations are for an increase to 84.0 from 82.9.