This week, the most important set of releases may be Thursday’s EU and US PMIs, as they may shed some light on whether and to which extent did the economic wounds, due to the coronavirus, drag into the second quarter of the year. The German ZEW and Ifo surveys for April may also attract special attention. We also get several data out of the UK, including the inflation prints for the month of March.

Monday is a relatively light day, with no major data on the economic agenda. The only releases worth mentioning are Eurozone’s current account and trade balances for February. That said, no forecast is available for neither release.

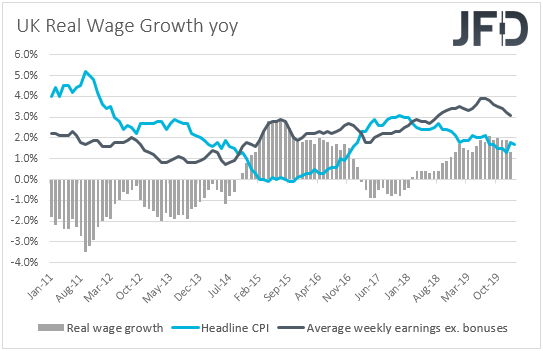

On Tuesday, during the European day, we get the UK employment report for February. Expectations are for the unemployment rate to have ticked down to +3.8% from 3.9%, while the 3-month rolling employment change is expected to show that the economy has gained 143k jobs, after adding 184k in January. Average weekly earnings including bonuses are expected to have slowed to +3.0% yoy from 3.1%, but the excluding bonuses rate is forecast to have ticked up to +3.2% yoy from 3.1%. Having said all that though, we don’t believe that this report will get the attention it has been usually getting. The reason is because it is referring to a period before the fast spreading of the virus started, leaving deep wounds to the UK economy. We believe that GBP-traders may prefer to pay more attention to data referring to more recent periods, like the CPIs and retail sales for March, due out on Wednesday and Thursday respectively.

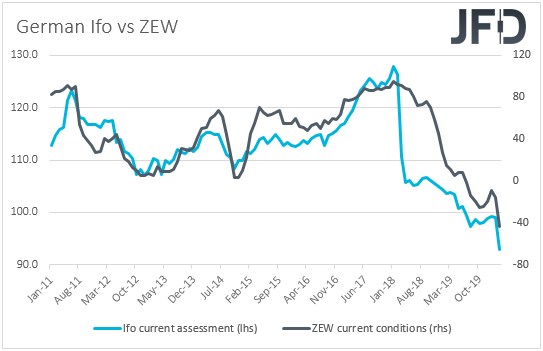

From Germany, we get the ZEW survey for April. Both the current conditions and economic sentiment indices are expected to have stayed in negative waters, but to have rebounded somewhat, to -30.0 and -43.0 from -43.1 and -49.5 respectively. Something like that may prove that the recent slowdown in the coronavirus spreading has somewhat improved analysts’ morale, and may raise speculation that the Ifo survey, which is based on manufacturers’ and retailers’ opinions, may follow suit.

Later in the day, we get Canada’s retail sales for February. The headline rate is expected to have ticked down to +0.3% mom from +0.4%, while the core one is anticipated to have rebounded to +0.2% from -0.1%. Similarly, with the UK employment data, we don’t expect this release to prove a major market mover. We believe that Loonie traders may prefer to focus on more recent data, one of which may be Canada’s CPIs for March, due out on Wednesday.

In the US, we have the existing home sales for March, which are expected to have slowed to +0.7% mom from +6.5% in February.

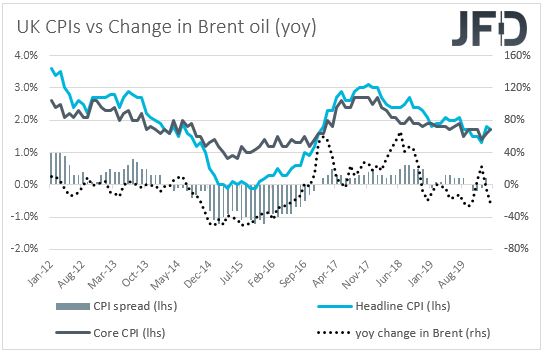

On Wednesday, during the European trading, the UK CPIs for March are due to be released. The headline rate is forecast to have held steady at +1.7% yoy, while the core one is anticipated to have slid to +1.5% yoy from +1.7%. However, bearing in mind that the yoy change of Brent oil slid deeper into the negative territory during the month of March, if the core rate is to slide, we see the risk for the headline one to have declined even more. Remember that the difference between the headline and the core CPIs is volatile items, like energy.

At their latest gathering, the first headed by the new Governor, Andrew Bailey, BoE policymakers decided to keep interest rates unchanged at 0.10%, and agreed to continue with their program of GBP 200bn of UK government bond and sterling non-financial investment-grade corporate bond purchases, to take the total stock of these purchases to GBP 645 billion. With regards to their future plans, they noted that they will continue to monitor the situation closely and that they stand ready to respond further if needed. Thus, a slowdown in inflation, further below the Bank’s objective, could add to speculation that the BoE could enhance its stimulus efforts to support the British economy from the coronavirus wounds.

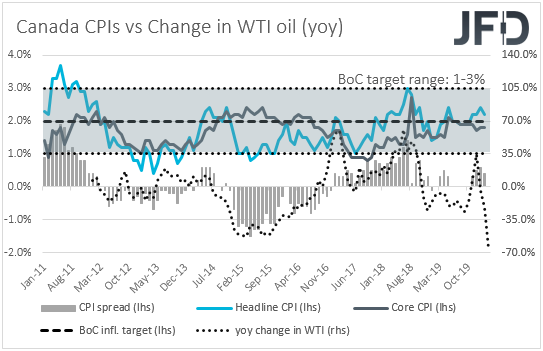

Later in the day, we get more inflation data for March, this time from Canada. The headline rate is expected to have ticked down to +2.1% yoy from +2.2%, while no forecast is available for the core rate. Taking into account that the yoy rate of change in WTI fell further into the negative territory, we see the risks of the core rate as tilted to the downside. That said, with the BoC announcing an expansion of its QE purchases just last week, we don’t expect this data set to force policymakers to act again at the upcoming gathering, especially if the headline rate stays above the midpoint of the Bank’s target range of 1-3%. We believe that officials may decide to take the sidelines and monitor whether the already adopted measures have been having the desired effect on the Canadian economy.

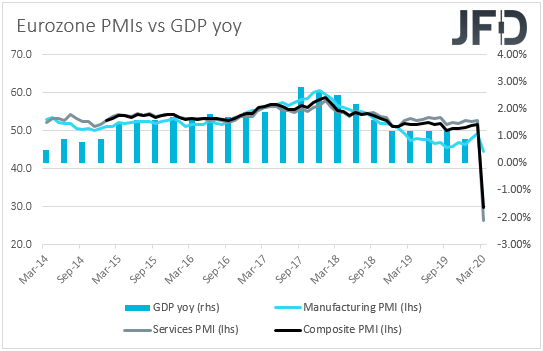

Thursday is a PMI day. We get the preliminary manufacturing and services indices for April from several Euro-area nations and the bloc as a whole, as well as the preliminary US prints. Both Eurozone’s manufacturing and services PMIs are expected to have declined further into the contractionary territory, to 40.0 and 24.0 from 44.5 and 26.4 respectively, something that will drag the composite index down to 26.0 from 29.7. In the US, the manufacturing index is expected to have slid to 42.8 from 48.5, while the services one is anticipated to have risen somewhat, to 42.0 from 39.8.

Another round of declines in the PMIs would enhance the view that the global economic wounds due to the coronavirus fast-spreading have dragged into the second quarter of the year. On Thursday, ECB President Christine Lagarde said that she and her colleagues are committed to doing everything necessary within their mandate to fight the crisis, while on March 26th Fed Chair Powell highlighted that the Fed is not going to run out of ammunition in its attempt to stimulate the economy. So, having all these in mind, a disappointing set of PMIs may raise speculation of even more easing by the ECB and the FOMC.

Apart from the PMIs, we also have the UK retail sales and the US new home sales, both for March. The UK headline retail sales are expected to have ticked down to +0.8% yoy from +0.9%, but the core rate is anticipated to have increased to +1.1% yoy from +0.5%. Nonetheless, bearing in mind that the yoy rate of the BRC retail sales monitor for the month slid to -3.5% from -0.4%, we see the risks surrounding the official figures as tilted to the downside. The US new home sales are forecast to have declined 2.2% mom after falling 4.4% in February.

Finally, on Friday, during the Asian morning, we get Japan’s National CPIs for March. No forecast is available for the headline rate, but the core one is anticipated to have declined to +0.4% yoy from +0.6%. The core Tokyo CPI rate ticked down to +0.4% from +0.5%, supporting the notion for a slide in the National core rate, while the headline Tokyo one held steady at +0.4%, suggesting that the National headline rate may have remained unchanged as well.

During the European day, the German Ifo survey for April is coming out. Both the current assessment and business expectations indices are expected to have declined to 82.0 and 75.0 from 93.0 and 79.7 respectively. This would drive the business climate index down to 80.0 from 86.1. However, bearing in mind that both the current conditions and economic sentiment indices of the ZEW survey are expected to have rebounded somewhat, we see the risks surrounding the Ifo forecasts as tilted to the upside.

From the US, we get the durable goods orders for March and the final UoM consumer sentiment index for April. Headline orders are expected to have tumbled 11.4% mom after rising 1.2% in February, while the core rate is anticipated to have risen to -0.4% mom from -0.6%. This suggests that the tumble in the headline print may be due to a fall in aircraft orders, which appears as a normal phenomenon, at least to us, if we take into account the travel bans and the hits the industry has taken due to the pandemic outbreak. As for the UoM index, it is expected to be revised down to 67.2 from 71.0

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Weekly Outlook: April PMIs Under Investors’ Radar

Published 04/20/2020, 04:23 AM

Updated 07/09/2023, 06:31 AM

Weekly Outlook: April PMIs Under Investors’ Radar

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.