Stocks fell around the globe yesterday and in the current “risk on = buy USD” environment, that meant USD weakened. A fall in Treasury yields also helped to undermine the dollar. On the other hand, the USD was generally stronger against most emerging market (EM) currencies as investors moved to safer havens such as CHF. Downgrades of the global growth outlook from the IMF and OECD may have helped the move out of EM currencies. Yet the overall move was not a global growth fear as AUD and the other commodity currencies also gained vs USD.

Markets all over the world seem to be trying to figure out just what the end of quantitative easing means. The QE regime has lasted some 4 ½ years now; even a gradual tapering off would be a big change. Just as QE was a massive global experiment, so too will its end. Last week, when Mr. Bernanke suggested that the Fed could begin reducing QE, the dollar gained on expectations of higher interest rates; yet yesterday, stock markets fell, apparently for the same reason, and the dollar fell with them. One implication of this change for the FX market may be that the impact of economic indicators may change. “Good” could be “bad” and vice-versa if people are focused on what the data means for QE rather than for growth.

For example, a tapering off of QE is dependent on a solid recovery in the US labor market, which should be good for global trade and hence EM currencies; yet a reduction in liquidity was said to be one reason why EM currencies generally fell yesterday. Expect volatility to rise over the next several months as the market ponders this “regime change” and people disagree on whether to focus on the implications of indicators for the real economy or the financial markets (in other words, how many steps ahead they should be looking when trying to gauge the impact of news on markets).

EUR/USD is recovering somewhat as the outlook for further easing measures by the ECB wanes despite the downgrade to Eurozone growth forecasts. Yesterday’s pickup in German inflation (+1.5% yoy in May vs +1.2% in April) and the acceleration in Eurozone money supply growth makes a further easing next week less likely, even though the fall in lending to the private sector accelerated as well. German magazine Die Welt said that three ECB board members oppose ABS purchases, while Bank of France Gov. Noyer said yesterday that he’s not convinced of the merits of negative rates. Reconsideration of the likelihood of further moves at next week’s meeting may support EUR/USD over the next week.

Japanese capital flows out overnight showed another large (JPY 1.1tn) sale of foreign bonds, following last week’s JPY 804bn sale. Japan’s quantitative easing was supposed to push investors out of JGBs and into foreign bonds, but so far that doesn’t seem to be working (although these weekly figures can be distorted by the activity of the banks). Short term USD/JPY should be supported by the J-curve effect (price of imports goes up faster than the price of exports goes down, so the trade account deteriorates) but without that capital outflow, it may be hard for USD/JPY to rise long term.

Eurozone confidence surveys are out today. The flash consumer confidence figure already came out so the market interest, if any, will be on the business climate and industrial confidence. A slight positive change is expected, following the other recent positive business surveys (French, German, Belgian and Italian surveys all showed rises). That could support EUR/USD further in today’s climate. However, I wonder if businesses are being realistic. After seeing yesterday’s French consumer confidence fall out the bottom, I’m not sure whether we should have much confidence in European confidence.

The US data too is not that crucial; revised US Q1 GDP is expected to be unchanged from the original estimate at 2.5%. The focus will therefore be on the weekly US jobless claims, are forecast to be unchanged at 340k. That would push the four week moving average up to 343k from 340k, which could add to the negative USD tone.

The Market

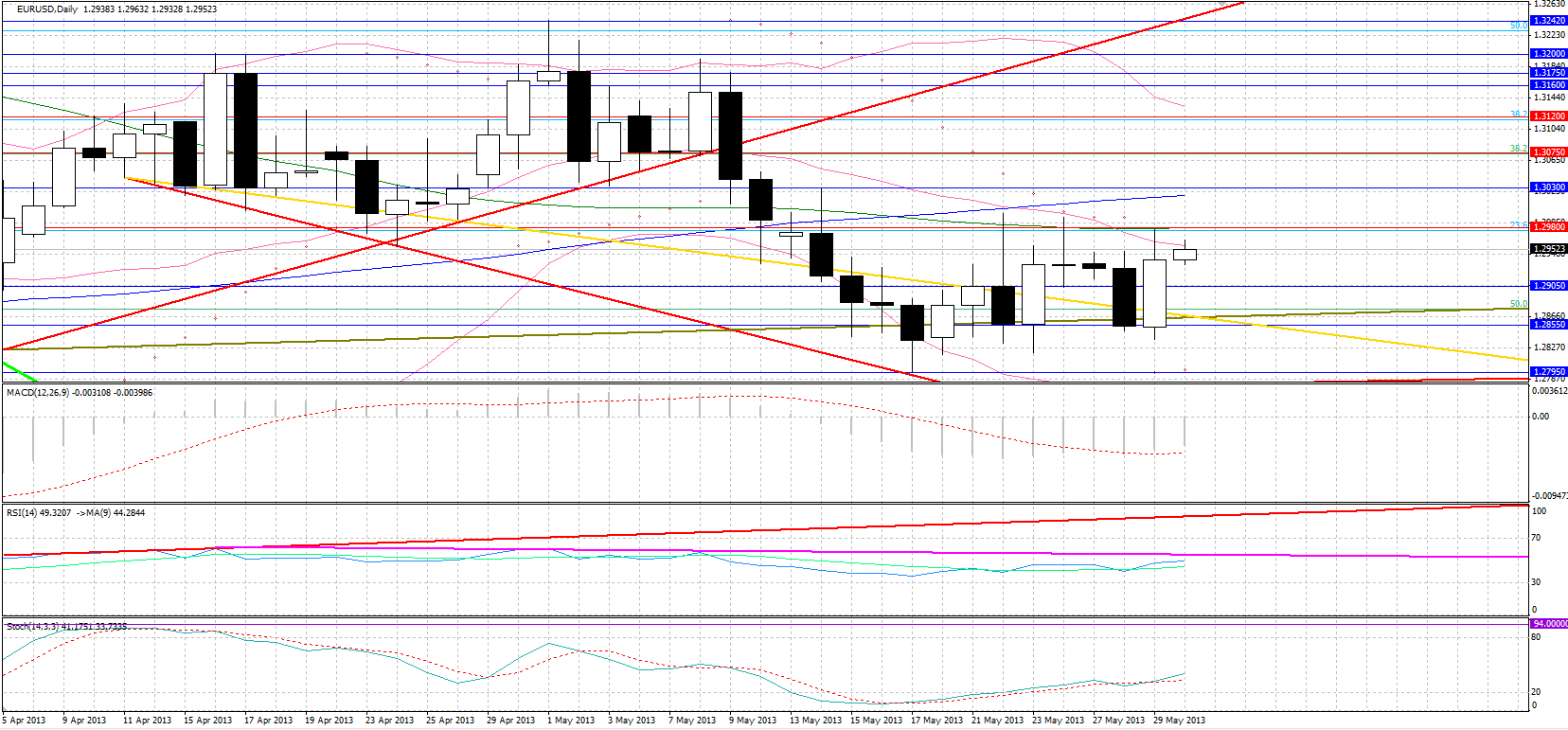

EUR/USD

EUR/USD" title="EUR/USD" width="1656" height="771">

EUR/USD" title="EUR/USD" width="1656" height="771">

• EUR/USD was a major gainer yesterday after bouncing higher from the 1.2850 support level. There is a strong resistance level at 1.2930, a level that was tested and held yesterday. If we see a further up move today this level is likely to be re-tested with a breakout leading towards to 1.3030. Support comes at the 1.2850 rising trendline support followed by1.2780.

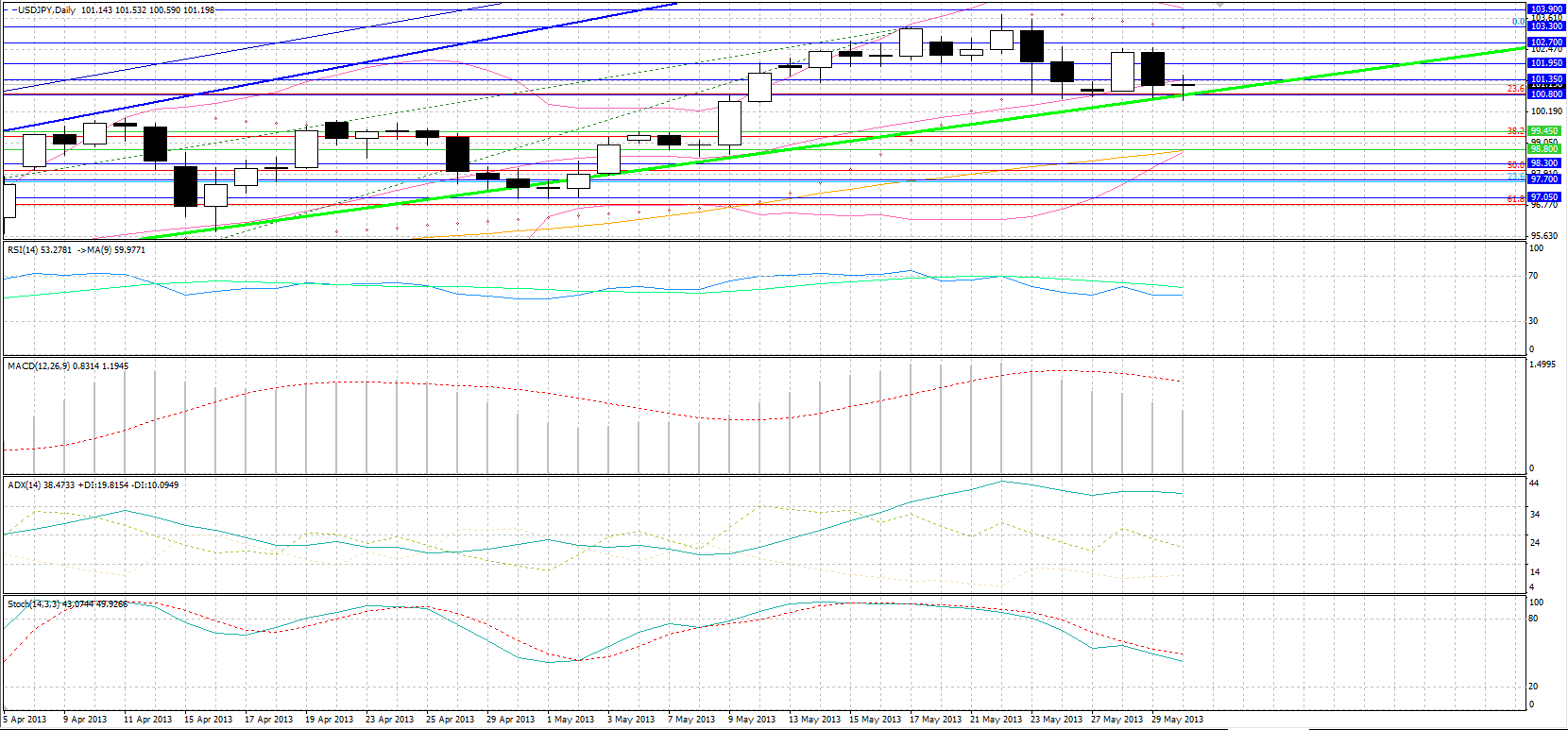

USD/JPY  USD/JPY" title="USD/JPY" width="1660" height="773">

USD/JPY" title="USD/JPY" width="1660" height="773">

• USD/JPY dropped yesterday, erasing the gains that were made on Tuesday. The drop found support once again at 100.80, which appears to be very strong as it has been tested every day since last week. A breakout of this support could lead towards 99.90. If 100.80 holds we could see the USD/JPY test 102.00 and 102.70 again.

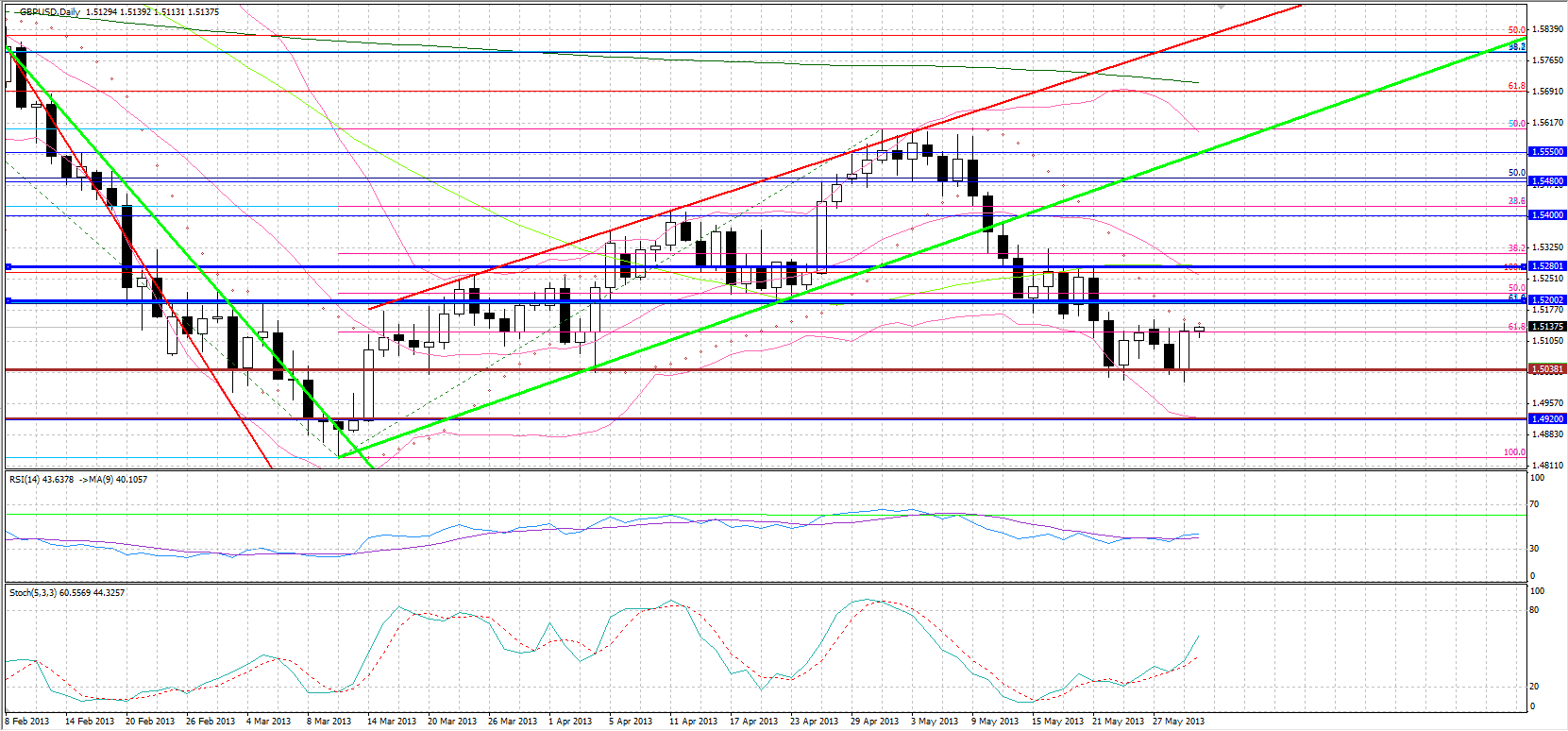

GBP/USD  GBP/USD" title="GBP/USD" width="1661" height="774">

GBP/USD" title="GBP/USD" width="1661" height="774">

• GBP/USD was another gainer yesterday following the decline in the USD. There is a strong support at 1.5040. That level was tested a couple of times during the past week and after the pair failed to break through, it bounced higher. Resistance comes at 1.5200 followed by 1.5280. If we see cable drop today, support is expected at the 1.5040 level followed by 1.4920.

Gold

• Gold once again remained unchanged, trading within the $1383-1400 range. Resistance levels remain the $1400 and $1430 levels. Support levels are $1383 followed by the $1350 level.

Oil

• WTI dropped massively yesterday after the API report showed inventories rose for the fifth consecutive week to the highest they’ve been in more than 30 years. On a technical basis, the plunge came after oil failed to close above the $95.00 key level and broke below the $93.50 support level, a support level that had been holding for quite a while. Support now comes at $92.30, while the next level can be found at $90.60. Resistance is the $95.00 level followed by $96.00.

BENCHMARK CURRENCY RATES - DAILY GAINERS AND LOSERS

MARKETS SUMMARY

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

USD Weakens As Market Mulls Implications Of Tapering QE

Published 05/30/2013, 08:23 AM

Updated 07/09/2023, 06:31 AM

USD Weakens As Market Mulls Implications Of Tapering QE

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.