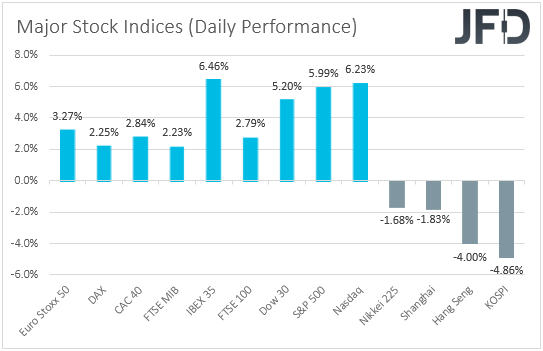

EU and US equity markets rebounded yesterday on announcements of fiscal stimulus packages from Spain and the US. The FOMC also took further measures to fight the effects of the coronavirus, noting that it will be purchasing short-term corporate bonds. That said, Asian bourses traded in the red today as the coronavirus new cases and deaths hit records yesterday. With regards to the FX world, NOK and CAD were the big losers, feeling the heat of tumbling oil prices.

WHITE HOUSE PLANS DIRECT PAYMENTS TO AMERICANS

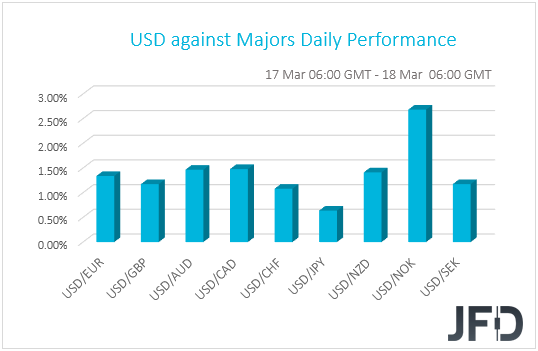

The dollar traded higher against all the other G10 currencies on Tuesday and during the Asian morning Wednesday. It gained the most versus NOK, CAD and AUD in that order, while it gained the least versus JPY and CHF.

The relative strength of the yen and the franc suggests a risk-off trading, while the slide in the krone and the Loonie suggests that oil prices kept tumbling. Although the latter is correct, the former conclusion is not that right. Yes, most Asian bourses closed in the red today, but major EU and US indices were a sea of green yesterday. European shares were boosted by the Spanish Prime Minister’s announcement with regards to a EUR 200bn stimulus package, with IBEX 35 surging 6.46%, while in the US, Wall Street indices rallied as the Fed and the White House proceeded with further measures in order to inject more liquidity and ease the effects of the fast-spreading coronavirus.

Specifically, the FOMC decided to purchase short-term corporate bonds in an attempt to help companies to keep paying their employees and buy supplies. This comes after several rescue attempts by the Fed, including the latest 100bps rate cut and the decision to restart US Treasury purchases. With regards to the government’s measures, the White House announced it is seeking a stimulus package worth between USD 850bn and USD 1.0tn. Potentially, USD 250bn will be directed to Americans via checks, and this could happen in the next couple of weeks.

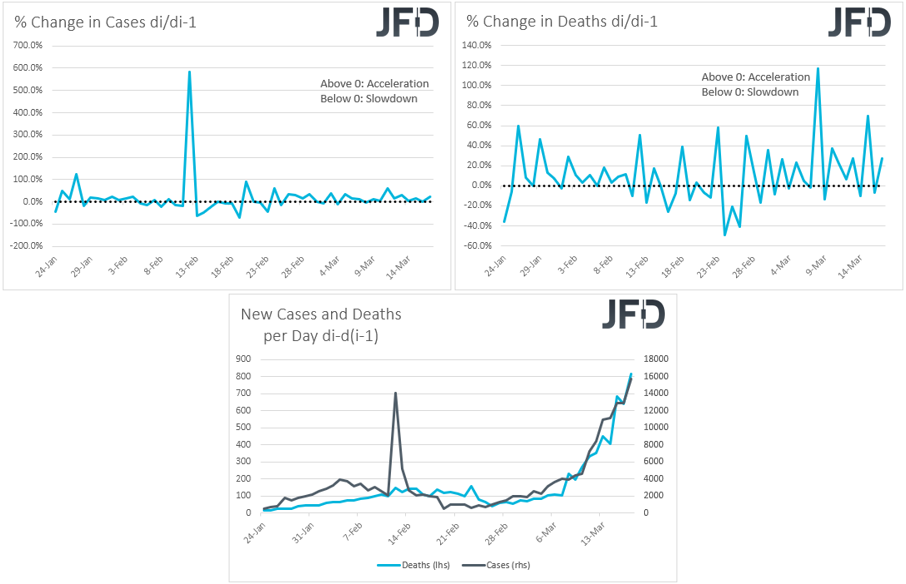

Having said all that though, the joy did not last for long as Asian indices turned south and the reason may have been once again the fact that the virus continues to spread at a fast pace. Both cases and deaths returned to acceleration mode yesterday, while in absolute numbers, they hit daily records. Namely, on Tuesday, we had 15740 new cases and 817 new deaths.

As for our view, we stick to our guns that consumers are unlikely to opt for cheap loans and get out of their homes to start spending. With the virus spreading around the globe at an exponential pace, even with helicopter money, people may prefer to stay home and save the money, perhaps considering it as compensation for their lost salaries. Thus, we don’t expect the latest bounce to continue. It was even halted during the Asian morning today. Since February 20th, we rarely saw two consecutive days of gains in the equity markets, and all the aforementioned suggests that we have not hit a bottom yet, especially with no virus-vaccine on the horizon.

Now, in case the opposite happens, where people and businesses start spending, this could lead a sharp rise in inflation, which would put central banks between a rock and a hard place. Their dilemma will be: Do we increase rates to avoid hyperinflation, or do we keep them low in order to save our battered economies from falling into recession? In our view, with most central banks cutting rates aggressively at the moment, we believe that they are either not prepared for such an outcome, or they just decided that they will prioritize saving growth over curbing inflation.

DAX – TECHNICAL OUTLOOK

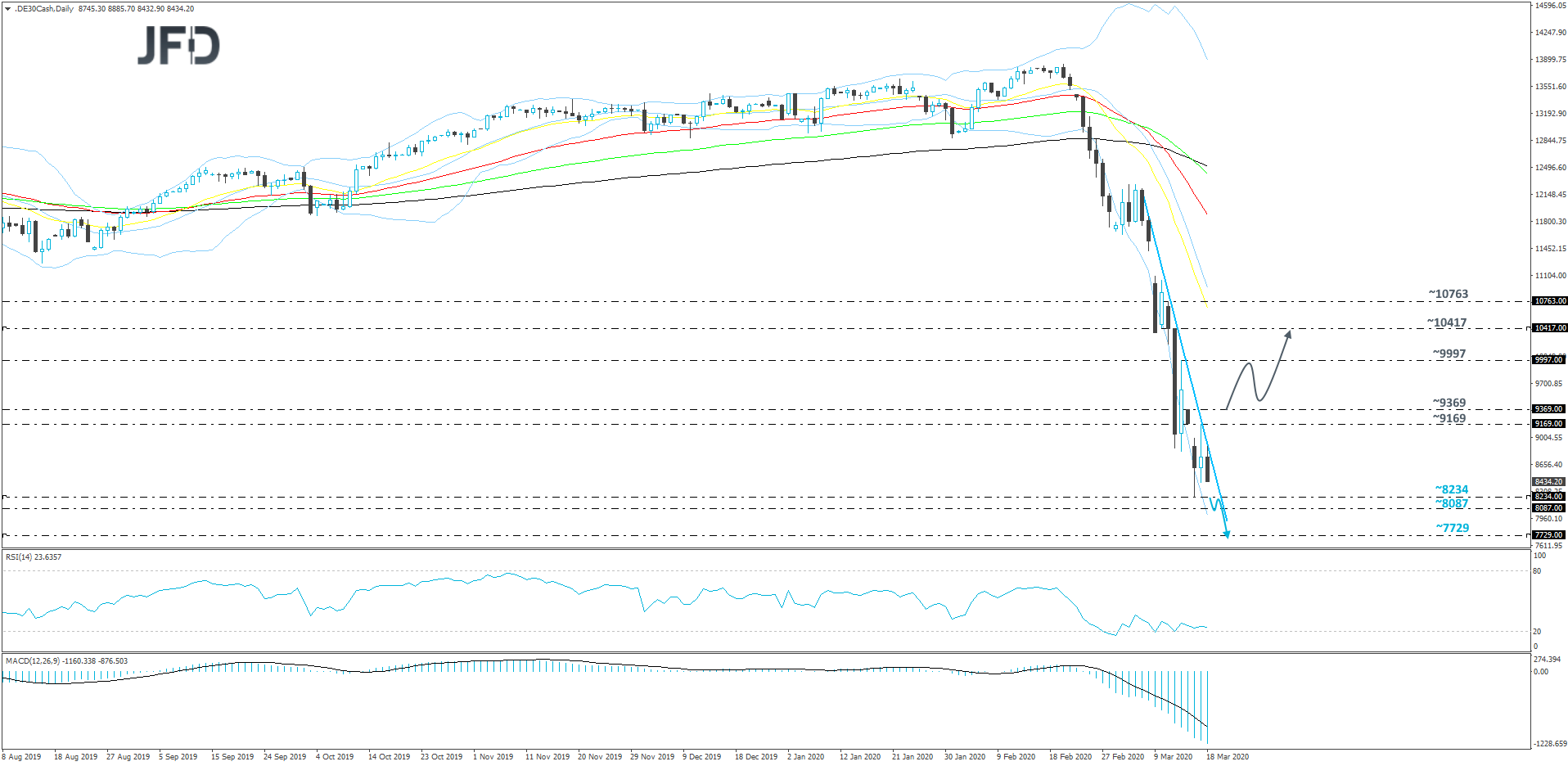

As the global indices continue to slide, DAX is joining forces with them in their journey south. This week, after finding support near the 8234 hurdle, the German index rebounded somewhat. However, looking at the daily chart of our DAX cash index, the price remains under bear pressure, as it is still trading below a very steep downside resistance line drawn from the high of March 5th. Although we are bearish overall, we would first like to see a break of the latest low, at 8234, before aiming for further declines.

As mentioned above, a break below that 8234 zone would confirm a forthcoming lower low and the move may clear the way to some even lower levels. The next area to consider might be the 8087 obstacle, marked by the lowest point of August 2013. If the slide continues, the next support level, which could get tested, may be at 7729, marked by the lowest point of July 2013.

Alternatively, if the aforementioned downside line breaks and the price climbs above the 9169 hurdle, or even the 9369 barrier, marked by the highest point of this week, we may see a larger correction to the upside. This could temporarily attract more buyers into the arena, possibly helping DAX to move towards the 9997 zone, a break of which could send the index to the 10417 level, marked by the high of March 12th.

OIL PRICES SLIDE, DRAGGING NOK AND CAD WITH THEM

Now back to the currencies, the dollar may have benefited from the White House announcement, but also because investors are liquidating positions everywhere in favor of holding cash. Remember yesterday we noted that even gold, which is usually considered a safe haven, has been in a tumbling mode, as holders of the precious metal liquidate their long positions to cover losses and margin calls elsewhere.

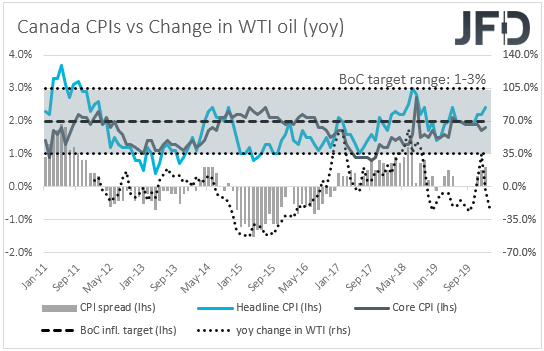

The Norwegian Krone and the Canadian dollar have been the main losers among the G10s, and this may have been owed to the tumbling oil prices. Both Brent and WTI fell 4.03% and 6.17% yesterday, on fears that the restrictive measures adopted for fighting the coronavirus will hurt energy demand even further, as well as due to the price war that has broken after the collapse of an agreement between OPEC and major non-OPEC members to curb supply further. Iraq’s oil minister called for an emergency meeting between producers in order to discuss immediate action for balancing the market. However, the hard stance of Saudi Arabia and Russia makes the case of finding common ground soon a very hard task. This means that with what we have in hand now, oil prices are likely to keep falling, dragging the Loonie and the Krone with them.

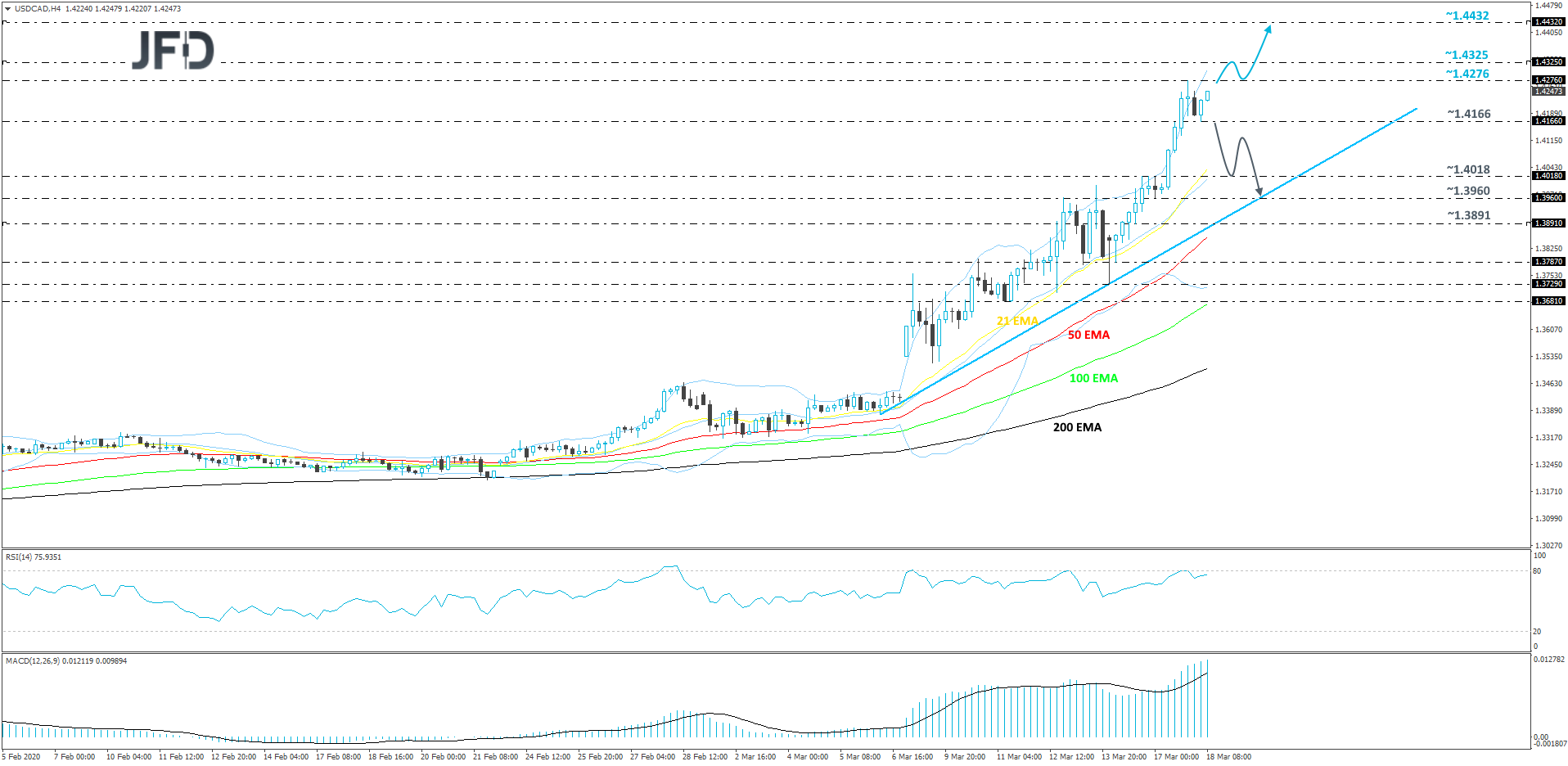

USD/CAD – TECHNICAL OUTLOOK

USD/CAD has rallied strongly this week, due to falling oil prices and the turbulence in the equity markets. After hitting the resistance level at 1.4276 yesterday, the pair retraced a bit. The rate continues to trade above a short-term upside support line taken from the low of March 6th. Although USD/CAD looks quite overbought, given the current market circumstances, it may drift a bit further north, especially if it clears the yesterday’s high. We will take a cautiously-bullish approach for now.

A break above yesterday’s high, at 1.4276, would confirm a forthcoming higher high and more buyers could be joining in. The pair might then get a boost to the 1.4325 zone, which is the high of January 26th, 2016. If the buying doesn’t stop there and the rate breaks that hurdle, the next target could be around the 1.4432 level, marked by the inside swing low of January 19th, 2016.

On the other hand, if USD/CAD starts sliding and drops below the current low of today, at 1.4166, this could make the bulls worry temporarily, as the move may increase the pair’s chances of drifting a bit lower for a larger correction. That’s when we will target the 1.4018 obstacle, a break of which may send the rate to the 1.3960 level, marked by the low of March 17th. Around there, USD/CAD could also test the aforementioned upside line, which might provide additional support.

AS FOR TODAY’S EVENTS

Under normal circumstances, we would have had an FOMC policy decision, but following the 100bps cut late Sunday/early Monday, Fed Chair Powell announced that the Committee will not proceed with this week’s scheduled meeting. The same may apply for the BoJ’s gathering during the Asian morning Thursday.

As for the data, during the European morning today, we get Eurozone’s final CPIs for February and as it is always the case, they are expected to confirm their preliminary estimates, namely that the headline rate slid to +1.2% yoy from +1.4%, while the core rate ticked up to +1.2% yoy from +1.1%.

From the US, we get building permits and housing starts for February, with the forecasts suggesting small declines, while from Canada, we have the CPIs for February. The headline CPI is anticipated to have slowed to +2.1% yoy from +2.4%, while no forecast is available for the core rate, which stood at +1.8% yoy in January. Under normal circumstances, this would have allowed BoC policymakers to stay away from the cut button, but bearing in mind that central banks are now acting to support the wounded global economy that is hit by the effects of the coronavirus outbreak, we cannot rule out another bold action by the BoC, perhaps outside a scheduled meeting as well.

With regards to the energy market, the EIA (Energy Information Administration) report on crude oil inventories is coming out and the forecast points to a 1.963mn barrels slide, from a 6.404mn decrease the week before. However, bearing that the API report yesterday revealed a much smaller slide (-0.421mn), we see the risks surrounding the EIA forecast as tilted to the upside.

As for tonight, during the Asian morning Thursday, we have Australia’s employment report for February. The unemployment rate is expected to have stayed unchanged at 5.3%, well above the 4.5% threshold which the RBA believes it will start generating inflationary pressures, while the employment change is forecast to show that the economy has gained less jobs than it did in January. Specifically, it is expected to reveal 10k new jobs, down from the 13.5k print in January.

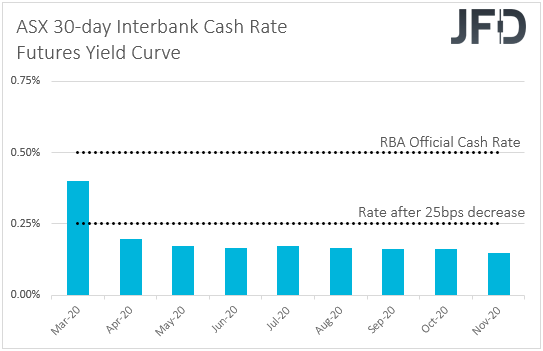

At their latest meeting, RBA officials decided to cut interest rates by 25bps, to a new record low of 0.5%, with Governor Philip Lowe saying in the post-meeting statement that the coronavirus was having a “significant” impact on the domestic economy and that it’s hard to assess how large the effects will be. In the statement, it was also repeated that officials “remain prepared to ease monetary policy further to support the Australian economy”. According to the ASX 30-day interbank cash rate futures yield curve, investors expect officials to push the cut button again at the April meeting, and a soft employment report may just seal the deal.

New Zealand’s GDP for Q4 is also due to be released. The forecast is for the qoq rate to have declined to +0.5% from +0.7%, but this will drive the yoy one up to +2.4% from 2.3%. With all other major central banks easing their policy in order to safeguard the global economy from the coronavirus crisis, the RBNZ was no exception, kickstarting this week’s easing chorus with an emergency 75bps rate reduction, noting that the economic outlook has “deteriorated significantly”. Officials also added that the rate will stay at 0.25% at least for 12 months, meaning that there are no more cuts on the horizon. That said, they agreed that should further stimulus be required, a large-scale asset purchase program would be preferable. With all that in mind, we don’t believe that data referring to a period before the virus outbreak would alter that view and thus, they may not prove the market mover they usually are. We prefer to wait for data concerning the first quarter of 2020, as these numbers may prove determinant over to whether the RBNZ will proceed with QE.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Oil Prices Slide And Drag Down NOK And CAD

Published 03/18/2020, 06:28 AM

Updated 07/09/2023, 06:31 AM

Oil Prices Slide And Drag Down NOK And CAD

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.