Reopening to a consumer boom

It has been a strong start to 2021 despite the ongoing Covid-19 restrictions.

Robust manufacturing and construction numbers have been backed up by stellar consumer spending figures as the latest $600 stimulus payment boosted household buying power. Winter storms probably prompted a slight pullback in February. But with President Biden promising enough vaccines for all adult Americans by the end of May, consumers and businesses can look forward to the realistic prospect of a broad reopening of the economy from the second quarter onwards.

This means heavily impacted sectors including leisure, entertainment, hospitality and travel can finally open their doors and hire back workers. With an additional $1400 stimulus payment being part of President Joe Biden $1.9tn fiscal support package, economic momentum will surely build through 2Q into 3Q.

Moreover, household balance sheets are in great shape, with savings accumulated and credit card debts paid down. On household savings, there is strong reason to believe that improvements in finances are more evenly spread across the income distribution than in Europe. Consequently, with job opportunities set to expand on the reopening, a sizeable proportion of households may have the confidence to spend a portion of the accrued savings.

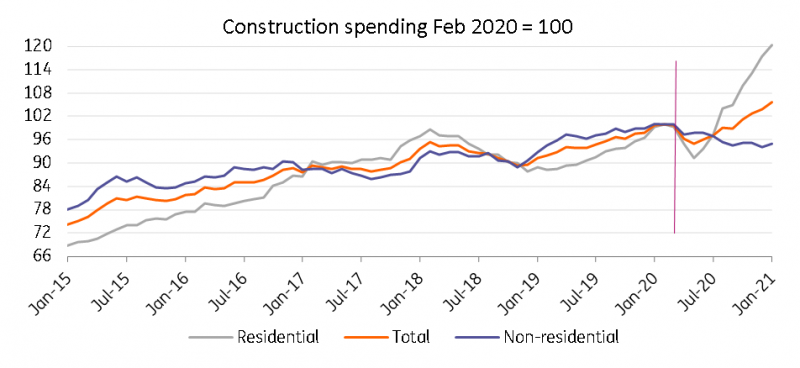

Residential property building is leading a construction boom

Source: Macrobond, ING

A broad based recovery

Corporate investment is also going to be making a major contribution to US GDP growth as businesses make up for the lost time.

The durable goods report points to a very strong growth story and with inventory levels looking low by historic standards a rebuild of stocks can also support the recovery. Then there is residential investment, which looks set to be well supported by the booming property market. The inventory of available homes for sale is at incredibly low levels – less than the equivalent of two months of sales for existing homes – which is likely to keep prices elevated and encourage construction.

The result is that we believe the US economy can grow in excess of 6% this year and if the $3tn+ Build Back Better programme of infrastructure and clean energy investment gets the green light this will keep the strong growth and job creation momentum moving forward into 2022 and beyond.

This economic vigour raises the potential threat of inflation

Annual inflation rates will rise significantly in the coming months as depressed price levels in the depths of the pandemic 12 months ago are compared with price levels in what we hope is a vibrant, reopened economy. On top of this, there could also be supply constraints in many industries; thousands of bars, restaurants and entertainment venues have closed, airlines have laid off staff and mothballed aircraft, and leisure and hospitality staff need to be hired and trained. If consumers have fewer options of where to spend money, businesses will have more pricing power and this could add to the inflation risk.

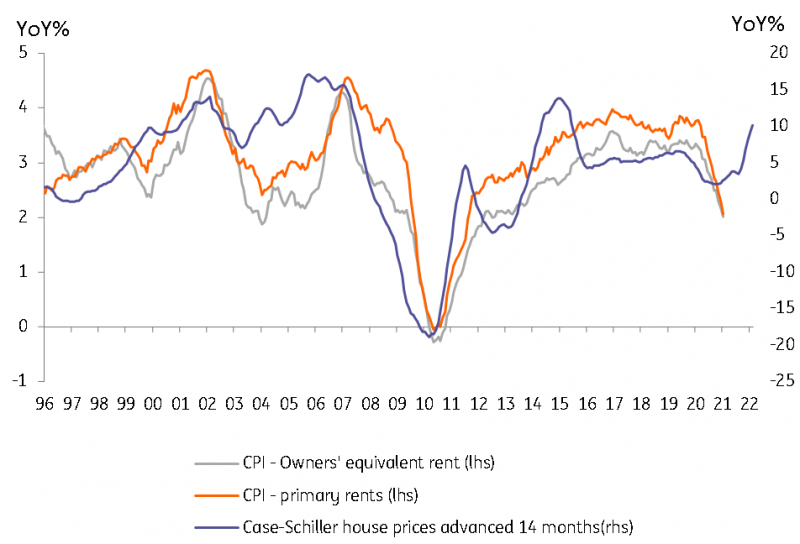

Freight bottlenecks and rising commodity and energy prices are an added threat for higher inflation readings while the red-hot housing market could translate into more sustained elevated inflation readings through the housing CPI components - owners’ equivalent rent component (24.3% of the total inflation basket) and primary rents (7.9% of the inflation basket).

Rising house prices could leave CPI higher for longer

Source: Macrobond, ING

And it could be stickier than the Fed anticipates

For now, Federal Reserve officials sound relaxed and are very much focused on ensuring the recovery happens, citing risks around the vaccine rollout and potential mutant Covid-19 strains. Officials also argue that there is spare capacity in the economy and that any spike in inflation will prove to be temporary. This has been enough to calm financial markets after the recent bond market sell-off, but there will be more challenges to come.

Our forecasts have inflation running in excess of 3% for much of this year and the economy growing 6.5% in real terms. This effectively gives us 10% nominal GDP growth. In such an environment and where fiscal policy is unambiguously expansionary, the case for ongoing monthly QE purchases of $120bn of Treasuries and mortgage-backed securities will be increasingly difficult to justify.

Federal Reserve risks are skewed towards earlier policy action

The Fed has suggested it will keep buying until there is “substantial further progress” towards meeting its inflation and labour market goals and this could take “some time”.

It is a very vague statement, but our interpretation of it involves a point where there is the imminent prospect of herd immunity, the economy is reopening with jobs being created plus the emergency of price pressures. All of this could materialise in the second quarter, so we wouldn’t be surprised to see the Fed signalling as soon as June that they will begin a gradual tapering of asset purchases before the end of the year.

This could also involve a “twist” to shift a greater weighting of the remaining purchases towards the longer end of the curve to perhaps limit the scope for any resulting yield curve steepening. In any case, we increasingly doubt the Fed will wait until 2024 before raising rates, as they are currently signalling.

We suspect a mid-2023 start point is more likely.

Original Post

Content Disclaimer: The information in the publication is not an investment recommendation and it is not an investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.

This publication has been prepared by ING solely for information purposes without regard to any particular user's investment objectives, financial situation, or means. Read more