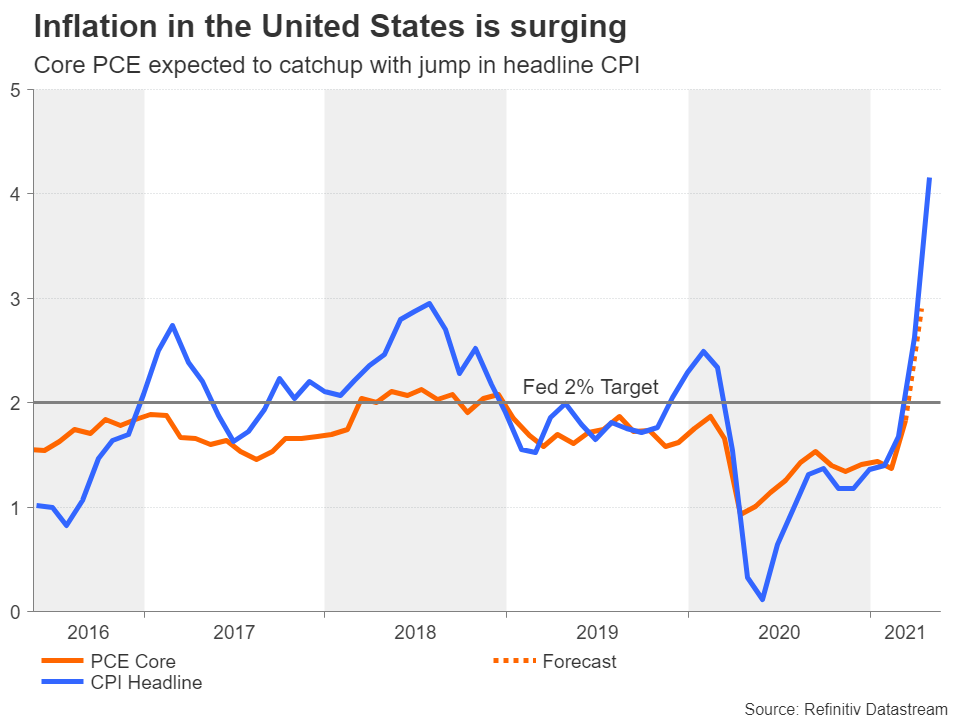

Core PCE inflation could shoot higher

When inflation expectations first began to reach worrying levels, markets were sceptical about the Fed’s relaxed stance towards the simmering price pressures. But after some not-so-spectacular data on the labour market and consumption, investors are happier to follow the Fed’s ultra-dovish guidance on the policy path. However, as markets try to make sense of the conflicting indicators on the strength of the US recovery, the higher inflation narrative could be about to become validated.

The core PCE price index, which is what the Fed looks at when aiming to keep inflation near 2%, is expected to have jumped to 2.9% year-on-year in April from 1.8% previously. Although the low base effect from 2020 is likely to blame for most of this increase, the fact that the core measure is anticipated to have risen so much so quickly to levels last seen in 1993 can only be interpreted as the start of a very dangerous trend.

Will the Fed and markets stay cool if inflation overshoots?

Of course, Fed policymakers and market participants will first want to see what happens to PCE inflation over the coming months – whether it begins to fall back towards the end of the summer, and the extent to which it declines. Until then, the incoming data may only generate knee-jerk reaction and Treasury yields may continue edging sideways.

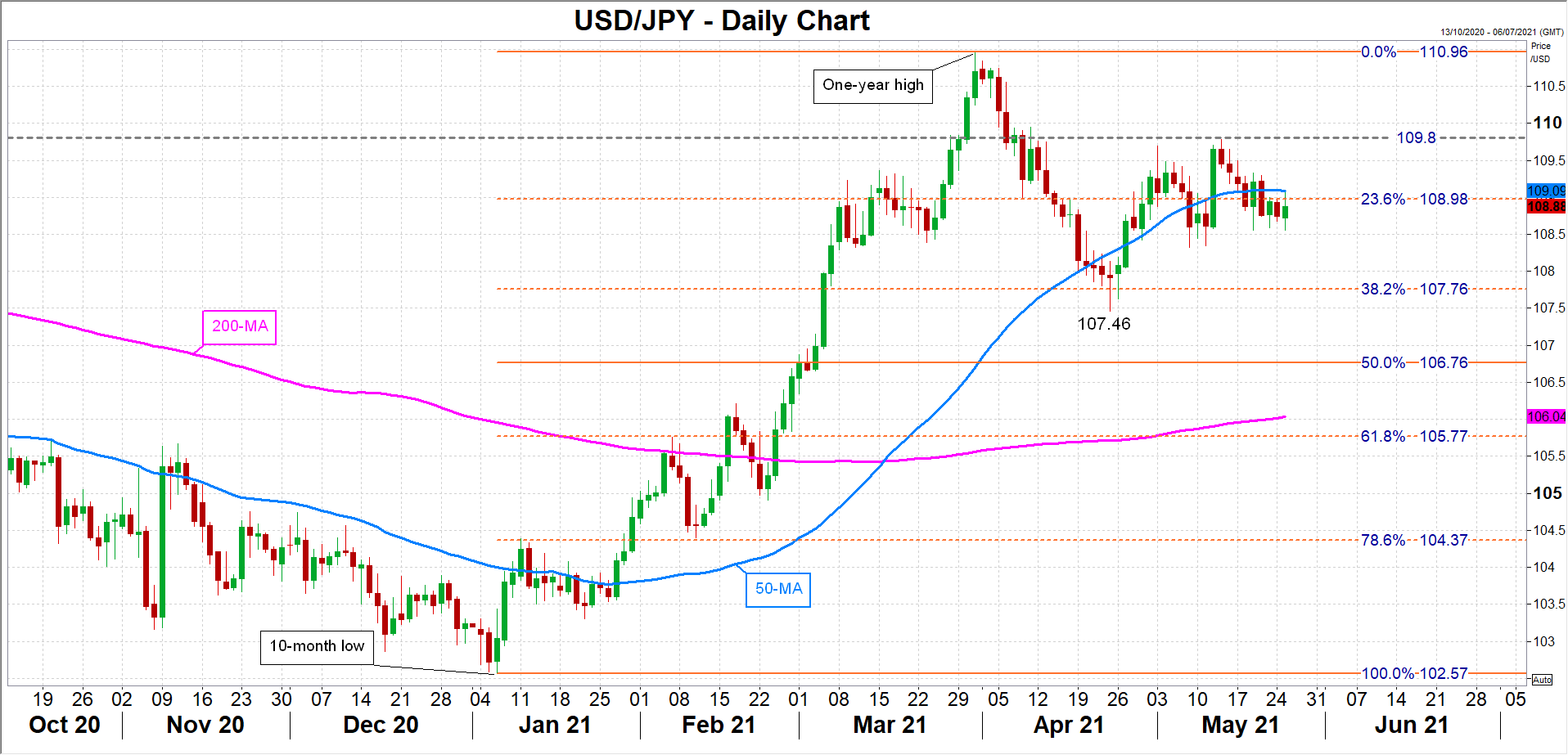

However, in the short term, Treasury yields have been under pressure, with the 10-year yield plunging below 1.60%. Any unexpected strength in this week’s releases could spur some fresh selling in bond markets, pushing yields and the US dollar higher.

The greenback has been hovering around the 109-yen level over the past week, just below the 50-day moving average, so a fresh upside burst could lift the pair above this critical resistance region and towards the next obstacle at 109.80 yen.

To the downside, the April low of 107.46, which is near the 38.2% Fibonacci retracement of the January-March upleg, remains the main support area defending the positive-to-neutral bias.

Consumption data in the spotlight too

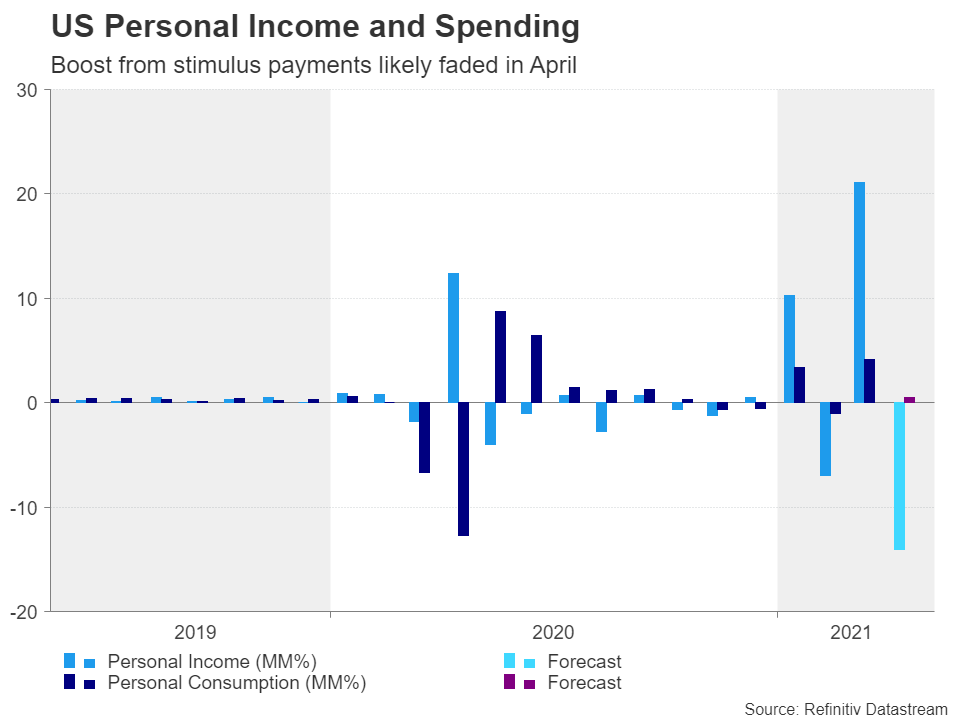

If the core PCE price index fails to set a clear direction, traders might turn to Friday’s personal income and consumption figures. Personal income is forecast to have plummeted by 14.1% month-on-month as the March boost from the stimulus payments fades. Personal consumption is projected to have risen by 0.5% m/m, slowing substantially from the prior 4.6% rate. A much milder slowdown in spending could go some way in reviving the more bullish expectations about the US economy.

Ahead of Friday’s numbers, durable goods orders for April will be watched on Thursday, along with the second reading of Q1 GDP growth. Durable goods orders are forecast to rise for the second straight month, while the preliminary GDP estimate of 6.4% is predicted to get revised up slightly to 6.5%.

On Tuesday, the latest consumer confidence index by the Conference Board showed consumer sentiment was little changed in May compared to April, with the index falling slightly to 117.2, which is notably below pre-pandemic levels of above 130.0.

Fed to stay on hold for a while longer

The data underlines how the recovery still has some way to go, supporting the Fed’s view that further progress is needed. Until the Fed is satisfied that all sectors of the economy have recovered or are close to being fully healed from the pandemic, it’s stance on monetary policy is unlikely to change, unless of course the spike in inflation turns out to be not so transitory. But that is a story for later in the year.