EUR/USD dropped to just below 1.2300 today as the overhead 1.2400/50 resistance remains in place. GBP/USD fades after yet another upside attempt on its second-worst trade deficit reading ever.

Asian Developments

Developments in Asia didn’t trigger much activity. The market tried to get excited about the Australian employment report, but it was pretty much in line and the mean reversion back to a slightly positive number wasn’t a big surprise after the terrible June data. The Chinese data was slightly worse than expected and I find it interesting that Caterpillar is exporting equipment from China to sell elsewhere due to slow demand as more interesting than the likely massaged official numbers. The Bank of Japan was effectively a non-event for JPY, as USD/JPY merely eased a bit higher as U.S. treasuries sold off today. The BoJ warned of the risk of weak exports in the current environment to the Japanese economy and effectively passed on hints of further easing this time around.

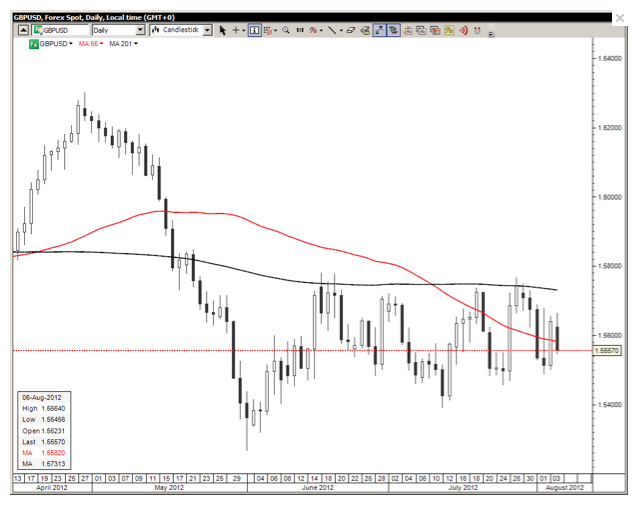

GBP/USD

The U.K. trade deficit was out at a near-record level for the month of June -- quite a contrast to the much stronger-than-expected U.S. trade -deficit number today, which should give one pause when looking at the sloppy attempt by GBP/USD to maintain a rallying stance. The EUR/GBP fell as widespread complacency is the only thing holding cable from a test of the strategic 1.5250 support area. GBP/USD" width="638" height="505">

GBP/USD" width="638" height="505">

Euro Periphery News

A Reuters article today offers good coverage of Mario Monti’s attempts to force the core E.U. powers to bend a bit on their unwillingness to commit more to bail out the periphery. The article points out that one of Monti’s strongest cards is ”the terrifying spectre of a return of Berlusconi, who has openly suggested that Italy could survive outside the Euro.” The stakes will only get higher from here. Meanwhile, Greek unemployment hit a new record at 23.1%. But the Greek government was quick to say it would get its mid-September tranche of bailout funds and there was word of a revival of plans to dismiss more workers from the public sector as part of the commitment to meeting reduced spending targets. The market wasn’t particularly impressed by the news.

U.S. Data

The data today was another argument in favour of more wait-and-see from the Fed, as weekly jobless claims were out at a comfortably low level and a far smaller-than-expected trade deficit in June argued for slightly better growth. The trade deficit was actually the smallest since late 2010. The weekly Bloomberg Consumer Comfort survey dropped to its worst reading in 10 weeks to -41.9, however, and has only registered two weekly readings worse than that since late January.

Looking Ahead

EUR/USD failed to take out the 1.2400+ area and today’s trade has been an expression of that disappointment. The pair worked lower through the weekly pivot around 1.2307 and looks ready to fully reverse back into the old range if it can’t pick up the rally impulse late today. AUD/USD is showing creeping signs of running out of momentum as new probes higher are consistently being beaten back -- stay tuned for a nosebleed watch, whether it’s here or after one more attempt at the 1.0700 trendline.

It is worth noting, once again, that the implied volatilities in FX have collapsed to new post-GFC lows and, in fact, back to pre-2008 levels. Likewise, the VIX is back near its lowest level for the cycle and the low of the long-term range as well. It appears the market consensus is that central-bank activism will outlaw all threats of market volatility. I wouldn’t be so sure! Of course, as I write these words, the S&P 500 is zipping several points higher just after the open to trade about a percent from the post-crisis highs. As the problem with an over-leveraged public sector grows ever worse and no one has a credible answer to the structural public-debt problems that face Europe, Japan and the U.S., are we really headed back toward complacency levels that were the hallmark of the height of the global credit bubble?

Tomorrow we have U.K. PPI and Canada's July employment report.

Stay ever careful out there.

Economic Data Highlights:

- New Zealand Aug. ANZ Consumer Confidence out at 114.1 vs. 110.5 in Jul.

- Australia Jul. Employment Change out at +14.k vs. +10k expected and -28.3k in Jun.

- China Jul. Consumer Price Index out at +1.8% YoY vs. +1.7% expected and +2.2% in Jun.

- Australia Jul. Unemployment Rate out at 5.2% vs. 5.3% expected and 5.3% in Jun.

- China Jul. Producer Price Index out at -2.9% YoY vs. -2.5% expected and -2.1% in Jun.

- Japan Jul. Consumer Confidence out at 39.7 vs. 40.0 expected and 40.4 in Jun.

- China Jul. Industrial Production out at +10.3% YoY vs. 10.4% expected and +10.5% in Jun.

- China Jul. Retail Sales out at +14.2% YoY vs. +14.3% expected and vs. +14.4% in Jun.

- Sweden Jun. Average House Prices out at 2.078M vs. 2.017M in May

- UK Jun. Visible Trade Balance out at -£10119M vs. -£8725M expected and -£8364M in May

- Canada Jul. Housing Starts out at 208.5k vs. 213k expected and 222.1k in Jun.

- Canada Jun. International Merchandise Trade out at -1.81B vs. -1.0B expected and -0.95B in May

- Canada Jun. New Housing Price Index out at +0.2% MoM and +2.3% YoY as expected and vs. +2.4% YoY in May

- U.S. Jun. Trade Balance out at -$42.9B vs. -$47.5B and vs. -$48.0B in May

- U.S. Weekly Initial Jobless Claims out at 361k vs. 370k expected and vs. 367k last week

- U.S. Weekly Continuing Claims out at 3332k vs. 3275k expected and 3279k last week

- U.S. Weekly Bloomberg Consumer Comfort out a -41.9 vs. -39.7 last week

Upcoming Economic Calendar Highlights (all times GMT)

- U.S. Jun. Wholesale Inventories (1400)

- New Zealand Jul. Credit Card Spending (2245)

- Japan Jul. Domestic CGPI (2350)

- Australia Reserve Bank Board’s Statement on Monetary Policy (0130)