Tilly's, Inc. (NYSE:TLYS) shares surged over 16% in after-hours trading session on Nov 30, following the company’s spectacular performance in third-quarter fiscal 2016. Consequently, it would be prudent on the investors’ part to hold on to the stock, as this retailer of casual apparel and footwear looks promising and is poised to carry the momentum ahead. This is quite apparent from the company’s impressive long-term earnings growth rate of 15.5% and a VGM Score of “A”.

In fact we observe that Tilly's shares have comfortably outperformed the Zacks Categorized Retail Wholesale industry ever since the company reported second-quarter fiscal 2016 results with an average return of 36.4% compared with -1.1% for the latter.

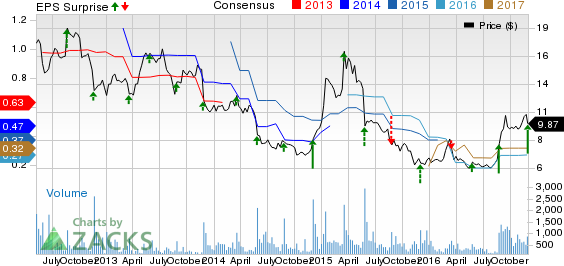

Tilly's reported third-quarter fiscal 2016 earnings per share of 22 cents, well above the Zacks Consensus Estimate of 10 cents and also surged 37.5% year over year. Notably, the company has reported positive surprise for the third consecutive quarter.

We believe the company will continue to entice investors as the Black Friday weekend and Cyber Monday were very promising for the company. Moreover, based on these positive factors the company is expects fourth-quarter earnings per share in the range of 15 cents to 20 cents, in comparison to year-ago earnings of 10 cents per share.

Gross profit increased 7.5% to $48 million, while gross margin came in at 31.5%, flat year over year. The company’s gross profit which increased 110 basis points (bps) due to lower buying, distribution as well as occupancy cost was neutralized by 110 bps increase in product margins on account of increased markdowns.

Operating income came in at $10.7 million in comparison to year-ago figure of $5.4 million. Operating margin jumped 320 bps to 7%.

TILLYS INC Price, Consensus and EPS Surprise

TILLYS INC Price, Consensus and EPS Surprise | TILLYS INC Quote

Continues with Revenues Uptrend

Tilly's revenues which have shown constant improvement since 2012 impressed investors in the third-quarter. The company’s revenue increased 7.3% year over year to $152.1 million and surpassed the Zacks Consensus Estimate of $142 million, making it the fifth consecutive quarter of revenue beat.

Moreover, comparable store sales rose 3.9% in the reported quarter while including eCommerce sales it increased 4.4%. Tilly’s expects fourth-quarter fiscal 2016 comparable sales in the range of flat to up 2%.

Other Financial Details

The company ended the quarter with cash and cash equivalents of $43.4 million, down from the prior-year quarter’s figure of $51 million. The long-term liabilities decreased to $37.1 million from $41.7 million in the year-ago period. On the other hand, shareholders’ equity stands at $104.5 million.

Other Stocks to Consider

Tilly’s currently carries a Zacks Rank #3 (Hold). Some better-ranked stocks worth considering include The Children's Place, Inc. (NASDAQ:PLCE) , sporting a Zacks Rank #1 (Strong Buy) while PVH Corp. (NYSE:PVH) and Nordstrom Inc. (NYSE:JWN) , both carry a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Children's Place has an average positive earnings surprise of 36.3% in the trailing four quarters. The stock, with a long-term growth rate of 10.3%, has seen positive estimate revisions in the last 30 days.

PVH has a long-term earnings growth rate of 11% and the company’s earnings have surpassed the Zacks Consensus Estimate in the trailing four quarters, with an average beat of 7.9%.

Nordstrom’s long-term EPS growth rate of 9.7% and solid positive estimate revisions for the current fiscal in the past 30 days aiding it stand strong in the industry. Moreover, the company has delivered back-to-back earnings beat in the last two quarters.

Confidential from Zacks

Beyond this Analyst Blog, would you like to see Zacks' best recommendations that are not available to the public? Our Executive VP, Steve Reitmeister, knows when key trades are about to be triggered and which of our experts has the hottest hand. Click to see them now>>

NORDSTROM INC (JWN): Free Stock Analysis Report

CHILDRENS PLACE (PLCE): Free Stock Analysis Report

PVH CORP (PVH): Free Stock Analysis Report

TILLYS INC (TLYS): Free Stock Analysis Report

Original post

Zacks Investment Research