The EUR/USD is slipping at the 1.30 level and the GBP/USD at 1.50 ahead of ECB and BoE meetings on Thursday. We also have the RBA up tonight and BoC on Wednesday - and much more in an action packed FX week.

Authorities in China are getting down to business in the new Chinese year to nip the risks from bubbly real estate prices in the bud; policy moves got markets off to a sour start for the week, with Chinese equity markets hit for steep losses.

The JPY was a bit weaker on a speech by Kuroda after he became Abe’s official nominee for the BoJ governorship, in which he promised open-ended asset purchases before next year. But at this point, talk is getting increasingly cheap with the JPY.

RBA up tonight

We’ve seen the Aussie trading lower on the weak asset market performance out of Asia overnight, and the currency will always have a hard time getting anything going as long as commodity prices are weak (note gold prices edging back toward recent lows as well). But the important test for Aussie in the nearest term will be tonight’s RBA meeting, where we look for the latest twists in the rhetoric. The front end of the curve has edged towards its lowest levels in many months, so we’ll need to see a bit of hawkishness to alter the status quo.

The latest RBA rhetoric has been fairly complacent, and there is little reason to expect dramatic developments. Governor Stevens has touted signs that the early easing moves are bearing fruit while at the same time the strong currency has mildly surprised some RBA officials, though they are happy that it has prevented any discomfort on the inflation front. It would be interesting if anything is mentioned on risks associated with weak commodity prices or uncertainties regarding China. Otherwise, besides what the RBA has to say, a technical break is a technical break –and the AUD/USD has taken out key near-term support, as discussed below.

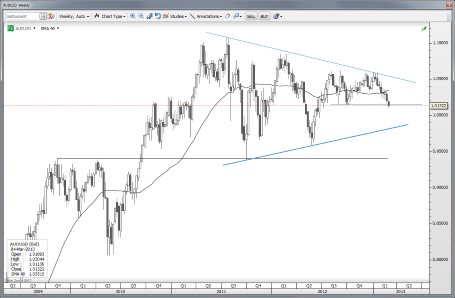

Chart: AUD/USD

The AUD/USD broke key flat-line support with its move below 1.0150 overnight, which sets up a key test. There’s plenty of room for the action to take the pair lower without threatening the major structure, which is the rising line of consolidation from the massive triangle that began forming back in in 2011. In other words, a true structural bear market for AUD/USD begins with a transition below the 0.9800-0.9900 area, depending on where (and if) the pair eventually cross below that rising line. AUD/USD" title="AUD/USD" width="455" height="298">

AUD/USD" title="AUD/USD" width="455" height="298">

Looking ahead

We’ve got a busy week ahead, with the RBA up tonight followed by the US ISM non-manufacturing survey tomorrow. This latter data point will be an important one - the US economy is managing to maintain a head of steam here in the near term despite the threats from the payroll tax cut expiry and sequester effects,

although some of the latter won’t be felt until later.

BoJ Deputy Governor nominees to speak tonight – focus on Iwata, who has been a very aggressive and long-time critic of BoJ policy.

Later this week: the Bank of Canada on Wednesday and then both the BoE and ECB on Thursday. Can the BoE say anything that stops the bleeding on the pound, or will it only encourage it further? The pound's inability vs. the euro despite the Italian election result,s speaks volumes about continued potential weakness for GBP. And as for the ECB, how does it respond to what is essentially an existential and political crisis rather than a monetary one?

Through the week, we have the ongoing uncertainty generated by Italy’s political situation. The weekend certainly failed to produce any reason for calm, as Beppe Grillo wants a referendum whether Italy should leave the Euro. On Friday, Bersani ruled out the idea of a grand coalition with Berlusconi, and claims he will form a government.

To top things off, we have the US employment report on Friday, just in case we though volatility would be muted this week….

Stay careful out there.

Economic Data Highlights

- China February Non-manufacturing PMI out at 54.5 vs. 56.2 in Jan.

- Australia January Building Approvals out at -2.4% MoM and +9.9% YoY vs. +2.8%/+8.1% expected, respectively and vs. +12.4% YoY in Dec.

- UK February PMI Construction out at 46.8 vs. 498.0 expected and 48.7 in Jan.

- Eurozone January PPI (1000)

- US Fed’s Yellen to Speak (1300)

- US February ISM New York (1445)

- Australia February AiG Performance of Services Index (2230)

- UK February BRC Sales Like-for-like (0001)

- Australia Q4 Current Account Balance (0030)

- Australia January Retail Sales (0030)

- Japan January Labor Cash Earnings (0130)

- Japan BoJ Deputy Governor Nominees to Speak in Parliament (0130)

- China February HSBC Services PMI (0145)

- Australia RBA Cash Target (0330)