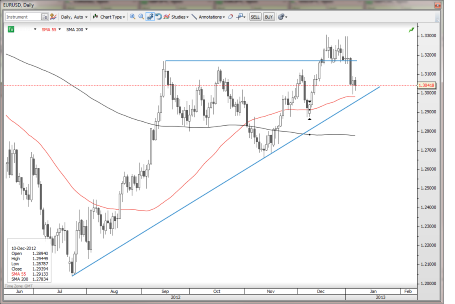

Last week saw a key rejection of the euro rally against the US dollar as the sequence above the old 1.3170 high was rejected by the close of trading last week. The key event this week that will spark a fresh look at euro fundamentals is the ECB meeting on Thursday. There may be little forthcoming in terms of concrete new measures from the ECB, but let’s look for hints of what the ECB is prepared to do down the road.

Chart: EUR/USD

Drawers of trendlines will note the key trendline in play in EUR/USD this week and we also look for whether the threat remains lower as the pair was unable to maintain altitude after the year-end break of the old 1.3170 resistance, which is now a reasonable area of resistance if 1.3090 fails to hold. EUR/USD" title="EUR/USD" width="455" height="304">

EUR/USD" title="EUR/USD" width="455" height="304">

JPY crosses

Today, we’re seeing a second attempt in JPY crosses at a consolidation lower after the brief attempt late last week by the market to digest some of the move in JPY weakening. The interesting scenario for USDJPY on Friday in terms of a blowout extension to the rally would have been a strong US jobs report. But the market was probably leaning a bit toward a stronger than expected report after the very strong ADP report, so the inline data was actually a slightly surprise.

The ISM non-manufacturing then surprised a bit with its strength and we saw the highs probed again, but US Treasurys and German bunds have paused a bit after the tremendous bloodletting last week and I suspect that the JPY crosses and treasuries will become more tightly correlated again now that we’ve seen this tremendous move in JPY weakening.

Zany Antipodeans

The aussie and kiwi have been on a zany roller coaster ride since late last year – first melting down as confidence suddenly crumbled ahead of the New Year and then squirting higher on thin liquidity as the US fiscal cliff deal was passed. Since then, they sold off and then squeezed back higher again. I can only say, mind the volatility – risk appetite is supportive, of course, but valuations are most certainly not, and we are concerned about the overall complacency here across markets, as our Chief Economist Steen Jakobsen discusses in his Weekly Stress Indicators piece from earlier today.

Looking ahead

As indicated above, the main event this week is the ECB meeting on Thursday. The US economic calendar is fairly quiet as we transition to the latest round of watching US politicians wrangle over fiscal issues – it will doubtless be an ugly spectacle.

Economic Data Highlights

- UK December Halifax House Prices fell -0.3% 3-Months YoY vs. -0.6% expected and -1.3% in November

- Switzerland December Foreign Currency Reserves out at 427.2B vs. 423.0B expected and 274.4B in November (November data revised upward from 424.8B)

- Eurozone November PPI out at -0.2% MoM and +2.1% YoY vs. -0.2%/+2.4% expected, respectively and vs. +2.6% YoY in October

- Canada December Ivey PMI (1500)

- Australia December AiG Performance of Construction Index (2230)

- UK December BRC Sales, Like-for-Like (0001)

- Australia November Trade Balance (0030)