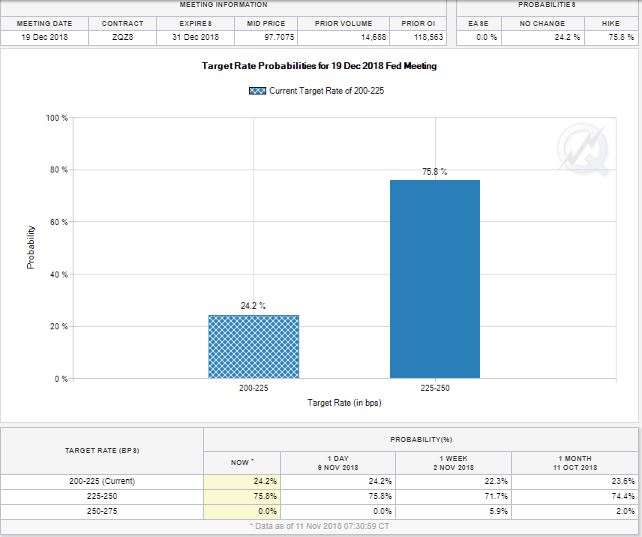

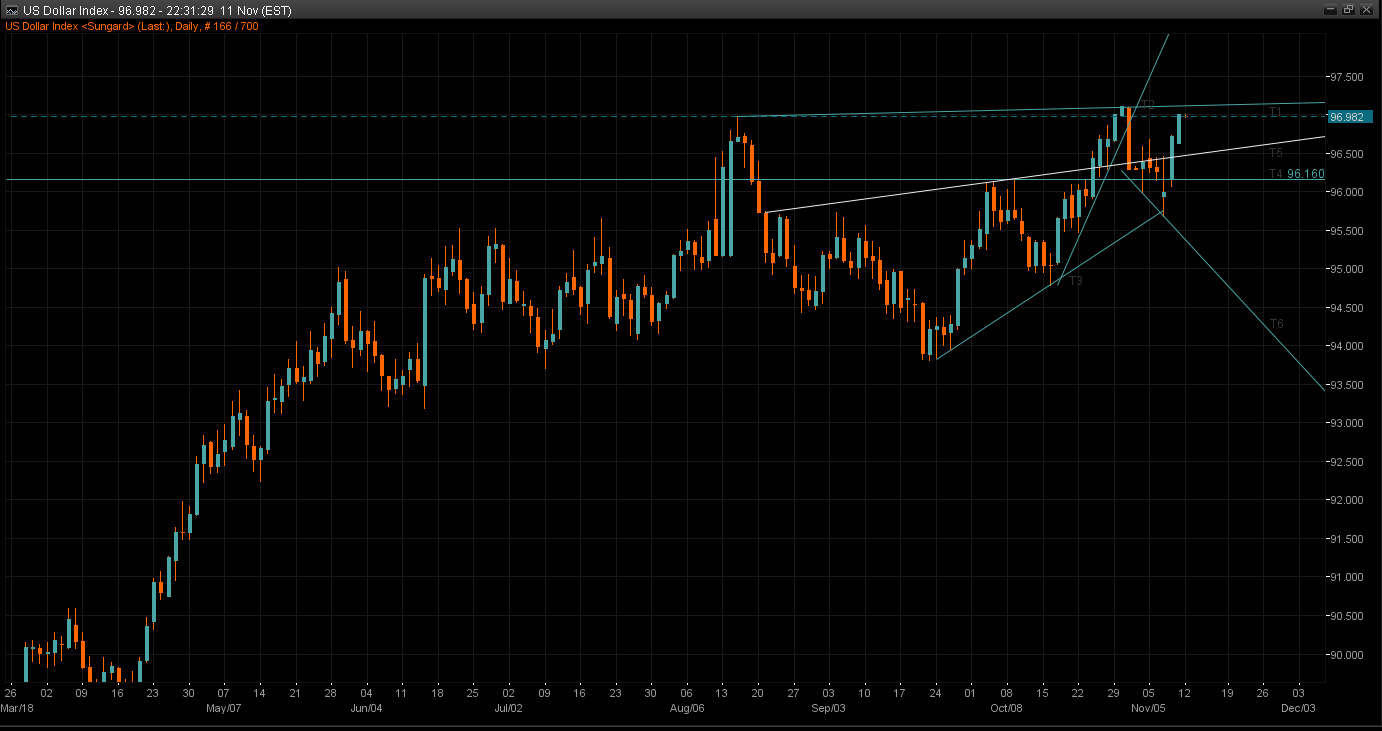

With the US and Canada both observing holidays on Monday, the economic calendar and liquidity will be a little lighter than usual. That said, the remainder of the week is packed with intriguing events from the US and its European counterparts across the pond. The two major releases on the American front are CPI on Wednesday, and Retail Sales on Thursday. Expectations are for increases in MoM and YoY CPI, as well as MoM growth in retail sales. With the odds of a December hike now sitting just below 76%, it is difficult to imagine this week’s data doing much to deter the Fed from its normalization plans. With the US Dollar Index reversing its post-election losses, DXY once again has its sights set on regaining the 97.00 handle. The 16-week high of 97.20 will be the next logical resistance point for traders to watch, and data from its fellow G10 counterparts will likely play a big part in determining the Dollar’s next move.

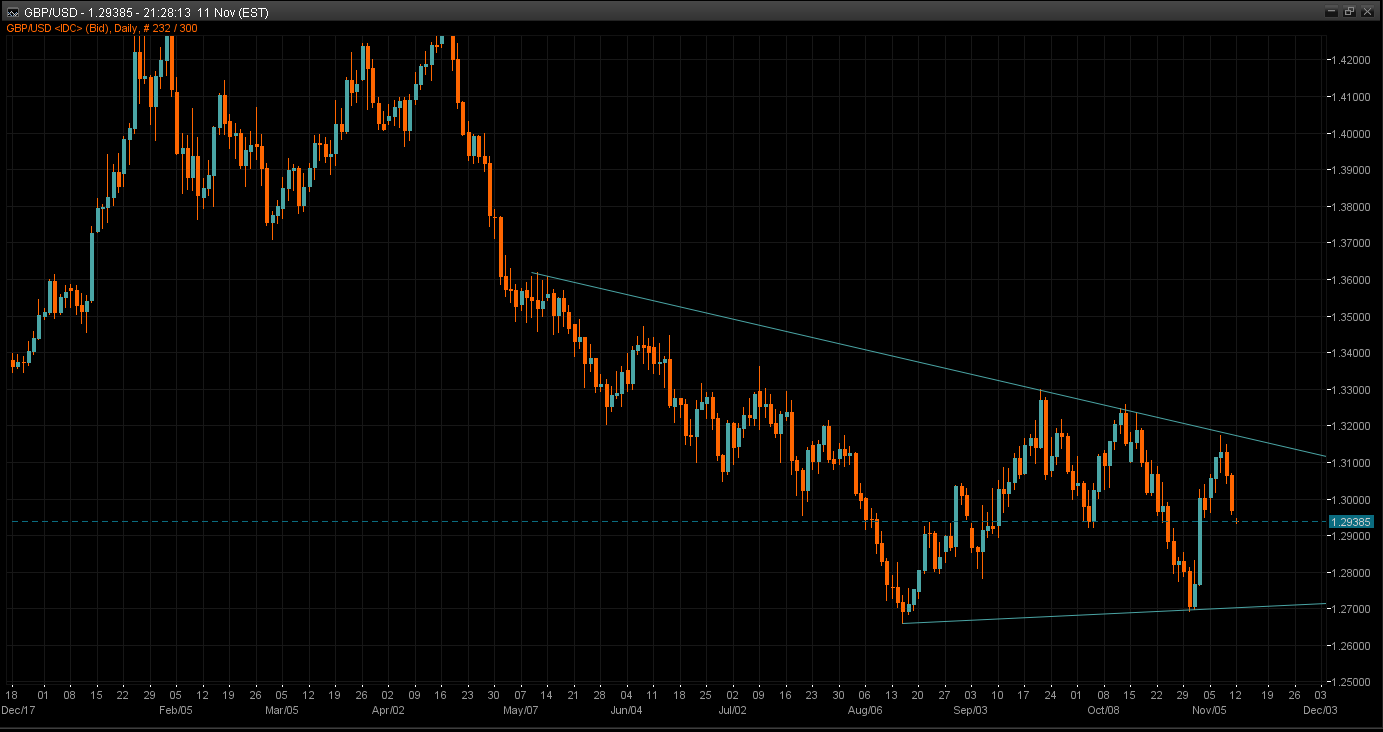

As we look across the Atlantic, the UK has an abundance of data releases this week that would normally be front and centre for Pound traders. While Average Earnings, CPI, and Retail Sales will no doubt impact GBP crosses, the true driver of the Pound is going to be the (seemingly never-ending) Brexit saga. No matter how strong the data is, all signs point to another volatile trading week in the Pound unless solid evidence of progress towards a deal is demonstrated.

Political risks are likely to outweigh the data when it comes to the Euro as well. German CPI and GDP are out this week, as well as Euro Zone GDP and CPI, but the data has not done any favours to the Euro as of late. It appears the risk is mostly to the downside based on data alone, but the brewing budget drama out of Rome is likely to weigh on the Euro more than anything. As it stands, both the sides are digging in their heels which makes it very difficult to see a sustained move higher under current circumstances.

All things considered, its quite difficult to bet on anything that isn’t the US dollar for the time being. If global risk aversion is the theme for the week, it might be positive for USD/JPY or USD/CHF. Even so, the trade-weighted DXY is unlikely to flinch so long as the Euro considers struggling. The fundamental and technicals are pointing towards DXY strength continuing, but a lot can change over the course of the week. Stay tuned.

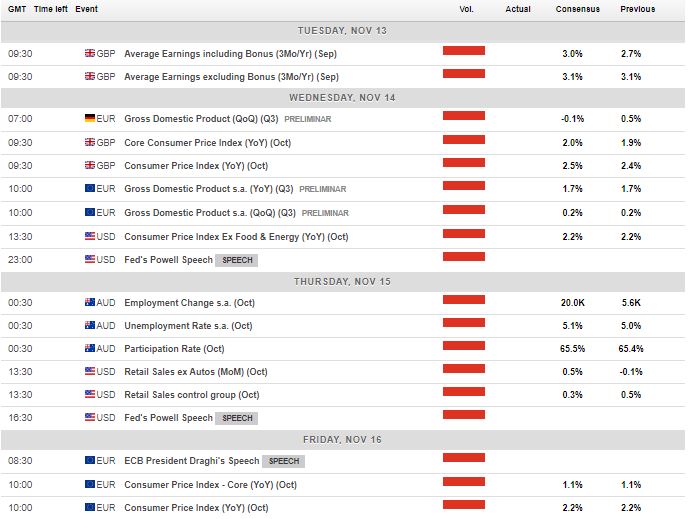

Upcoming Major Economic Events