Yesterday’s ECB meeting and the general market environment raise the risk of a further melt-up in risk in the short term. FOMC speakers up on Monday could add fuel to the fire or throw water on it, depending on their thinking.

In a recent video on CNBC, the famed Wall Street veteran Art Cashin generally pondered the rather bearish outlook for the moment, but discussed the risk of a “melt-up” scenario for equities (and therefore risk appetite in general, I would say), which could be driven especially by “asset shifts” from bonds into equities. Mr. Cashin only gave this scenario a one-in-five chance, but doesn’t yesterday point to a higher risk of this scenario, with the potential for a continued blow-off sell-off in the JPY and with the USD joining it, possibly adding to the overall phenomenon? Remember that the bond market is several multiples of the size of equity markets, with commodity markets an outright pipsqueak. Asset rotation and investors' ongoing desperation over “what to do” with their money - particularly now that bond yields are rising - could lead to a final brutal phase of this risk rally.

This would be a very interesting scenario for later this year, because an aggravated rally in risk assets will be unsustainable if the economic backdrop doesn’t improve dramatically (which it won’t – stability is about the best we can hope for at this time given the risk of further austerity and the background issue of the debt load and the possible end of the cycle of falling yields). A melt-up in risk could drastically increase the risk of market instability that could lead to uncomfortable volatility further ahead. It would also mean yet another bubble blown by the US Fed. If we get a zany rally and then an outright market crash, this could finally be the event that leads to the FOMC being forced to cease and desist from its mad money printing regime. Stay tuned, we could be at a critical inflection point here.

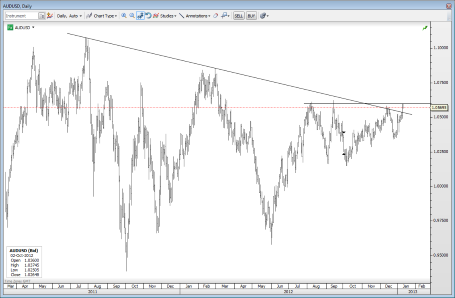

Chart: AUDUSD

The Aussie would likely be at the center of any melt-up scenario, should one occur, and yesterday’s rally finally saw the pair committing directionally after pausing in the 1.0500 area (and of course after I suggested it might be interesting to test the downside view tactically with a tight stop, because we had to see something happen soon, one way or another). Every time we have seen the pair head up toward this 1.0600 level over the last many months, it has shied away again, but as I pointed out yesterday, the trendline has now broken and now all we need is a move of confirmation through the top of the range, which could set up an attempt at the 1.10+ multi-decade high and in the right mix of complacency, to 1.12 or higher in the weeks to come. Look for Asian equity markets and commodities for confirming indicators of the ongoing risk of this scenario (gold posted an important reversal that helps support AUD). This doesn’t change the longer term outlook that AUD is over-valued and that this will end in tears, and in fact, the further we melt-up, the more violent will be the eventual melt-down on the other side. The next few days are critical for the pair.

AUD/USD" title="AUD/USD" width="455" height="298">

AUD/USD" title="AUD/USD" width="455" height="298">

EURCHF - why are we still here?

With the absolutely incredible turnaround in the Euro’s fortunes and the fact that Swiss small depositors are now being charged negative rates on their deposits just about anywhere they go (a Zurich bank added to the list of those charging negative rates yesterday), what exactly is preventing EURCHF from at least testing the waters a bit higher. Yesterday’s ECB meeting could be the event that finally uncorks a more sustained EURCHF rally, assuming everything stays orderly on the EU systemic front. THe flipside of this argument was that yesterday was merely a short squeeze on nervous Euro shorts - the key across Euro crosses is whether fresh Euro longs are bold enough to take EURUSD above 1.3300 again.

Looking ahead

Today we have very little in the way of event risks, the US Trade Balance later being a mere distraction. But already on Monday, we have the next round of FOMC event risks as Bernanke is out with a town hall meeting in Michigan and a variety of other FOMC members will be out making similar appearances. This Bernanke appearance can possibly fall one of two ways:

- Bernanke confirms the intention of the relatively hawkish looking FOMC Minutes by suggesting that “at some point” the Fed balance sheet will need to stabilize and even come in making it appear that the Fed’s stance is neutralizing ahead of his announcement (mid-spring?) that he won’t run for a second term.

- Bernanke is eyeing the long end of the yield curve with nervousness and will show dissatisfaction with the idea that the Fed has any plans to ease up in the near future and will tend to emphasize ongoing uncertainty and that the Fed remains ever-ready to keep conditions as easy as possible in support of the dual mandate. If there is anything the Fed has consistently shown, it is an amazing ability to not see bubbles blowing up on its watch.

The latter scenario (assuming Bernanke hints at Fed policy to come in this appearance at all), in this environment, would certainly help to feed the risk of a melt-up scenario. Stay tuned – the move yesterday and overnight in JPY crosses and the Euro is certainly feeding the growing likelihood that we will exit the super-low volatility environment that has plagued the major currencies for much of 2012.

And be careful out there, as always.

Economic Data Highlights

- Japan Nov. Adjusted Current Account Total out at +¥226B vs. +¥277B expected and +¥414B in Oct.

- China Dec. Consumer Price Index out at +2.5% YoY vs. +2.3% expected and +2.0% YoY in Nov.

- China Dec. Producer Price Index out at -1.9% YoY vs. -1.8% expected and -2.2% YoY

Upcoming Economic Calendar Highlights (all times GMT)

- Switzerland Dec. CPI (0815)

- Sweden Nov. Average House Prices (0830)

- UK Nov. Industrial and Manufacturing Production (0930)

- Canada Nov. International Merchandise Trade (1330)

- US Nov. Trade Balance (1330)

- US Nov. Trade Balance (1330)

- US Fed’s Plosser to Speak (1430)