The financial community switched to risk-on trading yesterday and today in Asia, as hopes of global economies reopening may have returned. Remarks by Fed officials that it is too early to start discussing policy normalization may have also helped. As for today, the main event may be the BoE decision, where policymakers are expected to slow down the pace of their bond purchases.

Equities Rebound On reopneing Hopes, BOE Takes The Central Bank Torch

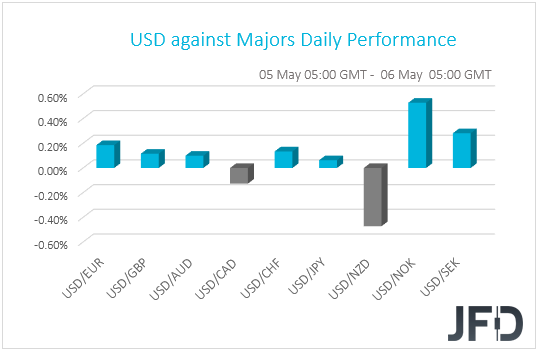

The US dollar was found slightly higher against all but two of the other G10 currencies on Wednesday and during the Asian session Thursday. It gained the most versus NOK, SEK, and EUR, while it underperformed only against NZD and CAD.

Despite the relative strength of the US dollar, the strengthening of the commodity-linked Kiwi and Loonie, as well as the fact that the Japanese yen was found nearly unchanged against its US counterpart, suggest that the financial markets may have traded in a risk-on fashion yesterday and today in Asia.

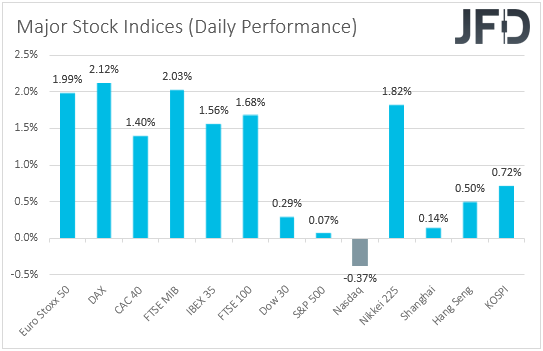

Indeed, turning our gaze to the equity world, we see that major EU indices rebounded strongly, marking their best day in nearly two months. Appetite softened somewhat during the US session, with NASDAQ sliding 0.37%, the S&P 500 gaining only 0.07%, but the Dow Jones rising 0.29% and hitting a fresh record high.

This suggests that market participants may have turned back to cyclically oriented sectors, as hopes of global economies reopening may have returned. Today in Asia, although China’s Shanghai Composite gained only 0.14%, Japan’s Nikkei 225 rallied 1.82%.

On Tuesday, stock indices tumbled following comments by US Treasury Secretary Janet Yellen that interest rates may have to rise somewhat to make sure that the economy does not overheat. However, yesterday, several Fed officials clearly suggested that they are in no rush of normalizing monetary policy.

Chicago Fed President Charles Evans clearly stated that he expects monetary policy to stay super-easy for some time, while Boston President Eric Rosengren said that inflation pressures will be short-lived and should not lead to a pullback in monetary policy. Last but not least, Cleveland’s Loretta Mester said that more progress in the job market is needed before the conditions for reducing support are met.

All this is in line with our view that market participants may continue to add to their risk exposures. Data suggesting that the global economy is recovering from the pandemic at a decent pace, a progress in the vaccination-rollout programs, the Fed’s extra-loose monetary policy, and US President Biden’s willingness to proceed with more fiscal support, are a blend of developments suggesting that stock indices may continue trending north.

Risk-linked currencies, like the Aussie, the Kiwi, and the Loonie, may benefit as well, while the US dollar and other safe havens, like the yen, may come under renewed selling interest.

Speaking about currencies, unlike the Kiwi and the Loonie, the Aussie failed to outperform its US counterpart. It was doing so during the whole day yesterday, but overnight, it tumbled as China said it plans to suspend indefinitely all activities under the China-Australia strategic economic dialogue mechanism, escalating strains due to Australia acting on China’s persistent human right abuses. In any case, the currency is now recovering those losses, suggesting that it could still be positively affected by further improvement in the broader market sentiment.

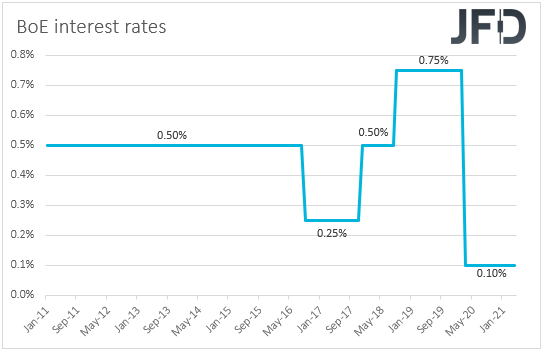

As for today, the main event may be the BoE monetary policy decision. Back in March, British policymakers kept their policy unchanged and noted that the recent plans for easing of covid-related restrictions may be consistent with a slightly stronger outlook for consumption growth. However, they repeated that the outlook for the economy remains unusually uncertain and that if the inflation outlook weakens, they stand ready to take the necessary action.

Since then, the UK economy has been recovering from the coronavirus recession faster than expected as the vaccine rollout continues, and market chatter suggests that officials are likely to scale back the pace of their bond purchases at this gathering. The pound could gain on such a decision, but pound traders are also likely to pay attention to the new economic projections, where upside revisions are likely to encourage them to add to their long positions.

The big risk today is for policymakers to postpone their decision to slow down their bond purchases, something that could disappoint participants and result in a sliding pound.

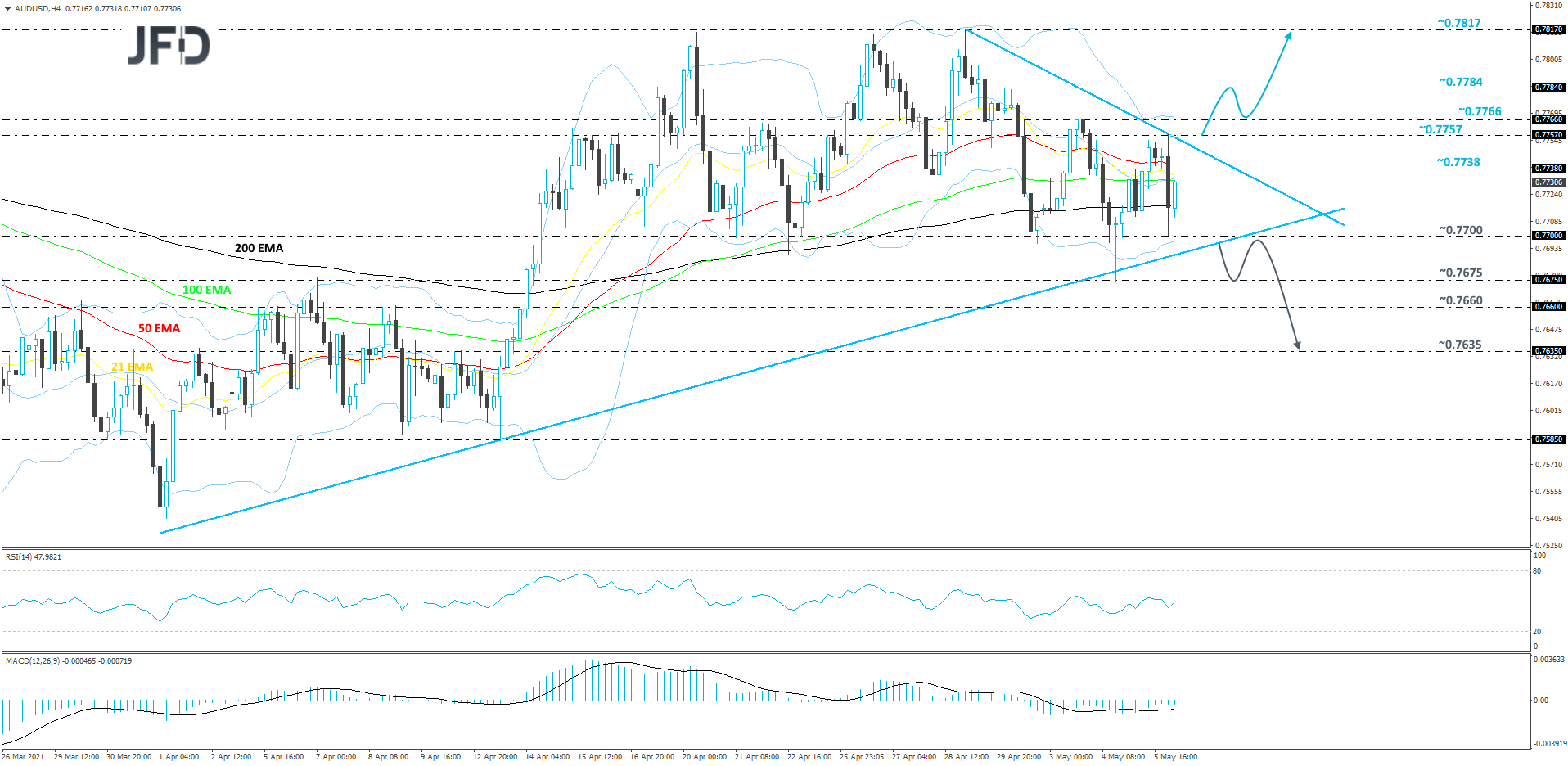

AUD/USD Technical Outlook

AUD/USD is currently stuck between two of its short-term lines, a tentative downside one drawn from the high of Apr. 29, and an upside one taken from the low of Apr.1. In order to consider the next short-term directional move, a break through one of the lines would be needed. Until then, we will take a neutral approach.

If the aforementioned downside line surrenders and the rate also pushes above 0.7757 barrier, marked by the current high of today, this might invite more buyers into the game. AUD/USD could travel to the 0.7766 obstacle, or even to the 0.7784 zone, marked by the high of Apr. 30, where a temporary hold-up may occur. If the buying doesn’t stop there, the next possible target might be at 0.7817, marked by the highest point of April.

Alternatively, if the pair ends up breaking the previously mentioned upside line, this could open the way for further declines, as more sellers may see it as a good opportunity to join in. AUD/USD could then travel to the current lowest point of May, at 0.7675, where a temporary hold-up could happen. However, if the bears are still dominating the field, they could overcome the 0.7675 obstacle and aim for the 0.7660 area, or the 0.7635 level, marked by the inside swing high of Apr. 12.

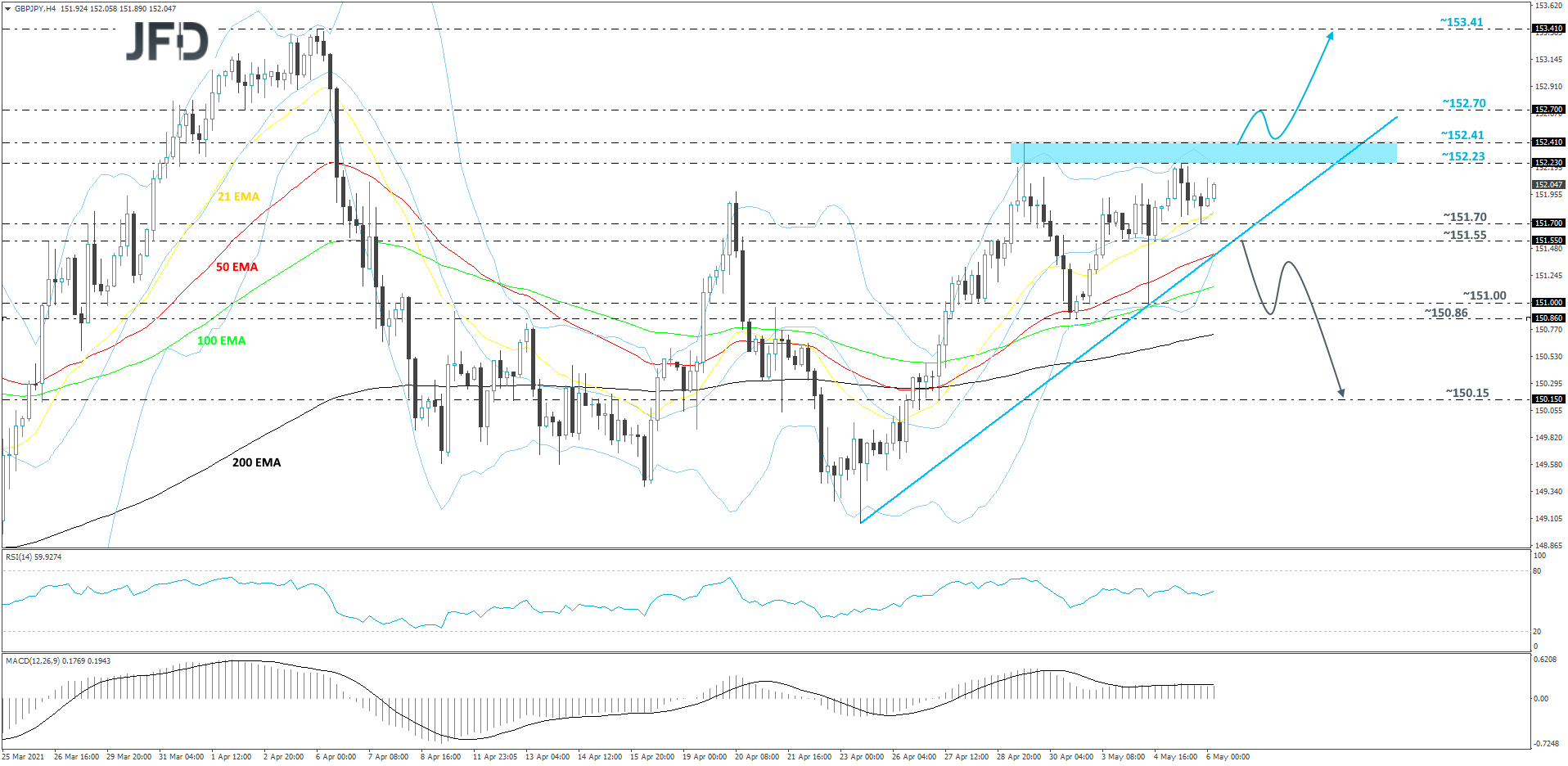

GBP/JPY Technical Outlook

After the reversal to the upside in the end of April, GBP/JPY is currently trading above a short-term tentative upside support line taken from the low of Apr. 23. However, before we could get comfortable with further advances, we would need the pair to overcome the resistance area between the 152.23 and 152.41 levels, marked by the highs of May 5 and Apr. 29 respectively. Until then, we will take a cautiously-bullish approach.

If, eventually, the pair does make its way above that resistance area, this would confirm a forthcoming higher high, potentially attracting more buyers into the game. The rate could then get pushed to the 152.70 hurdle, marked by the low of Apri.2 and an intraday swing low of Apr. 6, where GBP/JPY might stall for a bit.

It may even correct slightly lower, however, if the rate continues to trade somewhere above the previously mentioned resistance area, which now could take the role of support, then another push north might be possible. If so, GBP/JPY could make its way to the 152.70 obstacle again, a break of which may set the stage for a move towards the 153.41 level, marked by the highest point of April.

Alternatively, if the aforementioned upside line breaks, this could change the direction of the short-term trend, potentially inviting more bears into the field. GBP/JPY might drift to the support area between the 150.86 and 151.00 levels, marked by the lows of Apr. 30 and May 4. If the slide continues, the next possible target may be at 150.15, marked by the low of Apr. 27.

As For The Rest Of Today's Events

Besides the BoE monetary policy decision, the other releases worth mentioning are Eurozone’s retail sales for March and the US initial jobless claims for last week. Eurozone’s retail sales are expected to have slowed to +1.5% mom from +3.0%, while the US jobless claims are forecast to have declined slightly, to 540k from 553k.

Tonight, during the Asian session Friday, China’s trade balance for April is due to be released and expectations are for the nation’s trade surplus to have increased to USD 28.10bn from USD 13.80bn.

As for the speakers, we have five on today’s agenda and those are: ECB President Christine Lagarde, ECB Executive Board member Isabel Schnabel, New York Fed President John Williams, Atlanta Fed President Raphael Bostic, and Cleveland Fed President Loretta Mester. During the Asian trading tomorrow, we will get to hear from Dallas Fed President Robert Kaplan.