The Fed appeared dovish yesterday, saying that they will continue to increase bond and mortgage-backed securities “at least at the current pace”, something suggesting that purchases can accelerate again if deemed necessary. That said, the market reaction did not last for long. Equities gained, and the dollar slid, but this was quickly reversed, with stocks trading in negative waters and the greenback rebounding against the majority of the G10s.

FED APPEARS DOVISH, BUT INVESTORS KEEP REDUCING RISK EXPOSURE

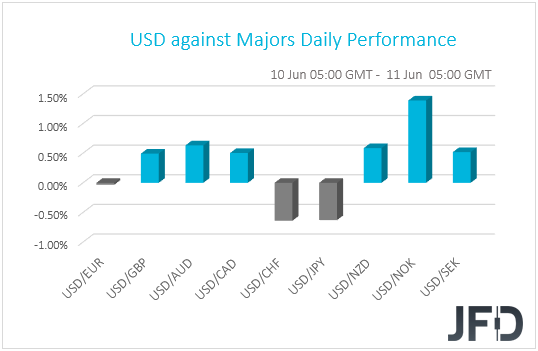

The dollar was found higher against most of the other G10 currencies during the early European morning Thursday. It was lower only against the safe-havens CHF and JPY, while it was found virtually unchanged against EUR. The greenback gained the most versus NOK, AUD, and NZD in that order.

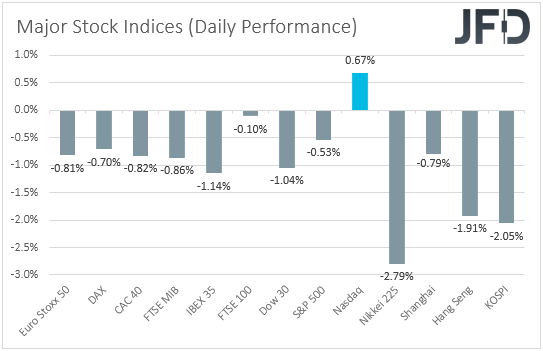

The strengthening of the safe-haven franc, yen, and dollar, combined with the weakening of the risk-linked Aussie and Kiwi, suggests that markets continued trading in a risk-off manner yesterday and during the Asian morning today. Indeed, turning our gaze to the equity world, we see that the majority of global stock indices finished their trading sessions in negative waters. The exception was Nasdaq, which hit a new record high, closing above the 10000 mark for the first time in its history.

The market impact of yesterday’s main event, the Fed’s decision, did not last for long. Ahead of the announcement, EU stocks continued sliding, as investors kept locking profits. At the time of the decision, US stocks inched higher and the dollar slid, but this was only temporary. It seems that investors continued with profit-taking post the decision, despite the Fed appearing dovish. The Committee kept interest rates unchanged and noted that they will continue to increase purchases of bonds and mortgage-backed securities “at least at the current pace”, something suggesting that purchases can accelerate again if deemed necessary. “The Committee will closely monitor developments and is prepared to adjust its plans as appropriate”, it was noted in the accompanying statement.

With regards to the new dot plot, the median dots suggested that interest rates are likely to stay at the current level at least until 2022. Members agreed unanimously for the rates to stay untouched until the end of 2021, with only two of them seeing increases in 2022. “We're not thinking about raising rates, we're not even thinking about thinking about raising rates”, Fed Chair Powell characteristically said at the press conference following the decision. As far as the economic projections are concerned, officials projected a 6.5% tumble in GDP for this year and a 5.0% rebound next year. They see the unemployment rate at 9.3% at the end of the year, and core PCE inflation at 1.0% yoy.

As for our view, it has not changed even after the FOMC decision. On the contrary, the Fed’s readiness to expand its stimulus efforts if things fall out of orbit is a positive for stocks and a negative for the dollar, in our view. Yes, investors appear to have continued locking profits after the recent steep surge in equities, but we don’t expect this to last for long. Eventually, the continued easing of the lockdown measures, combined with more data suggesting that the worse with regards to the coronavirus is behind us, may allow investors to increase their risk exposures again. This means higher equities and risk linked currencies, as well as lower safe havens. Among currency pairs, we think that the ones consisting of a risk-linked one and a safe haven will turn north again. Some of those pairs are AUD/USD, NZD/USD, AUD/JPY, and NZD/JPY.

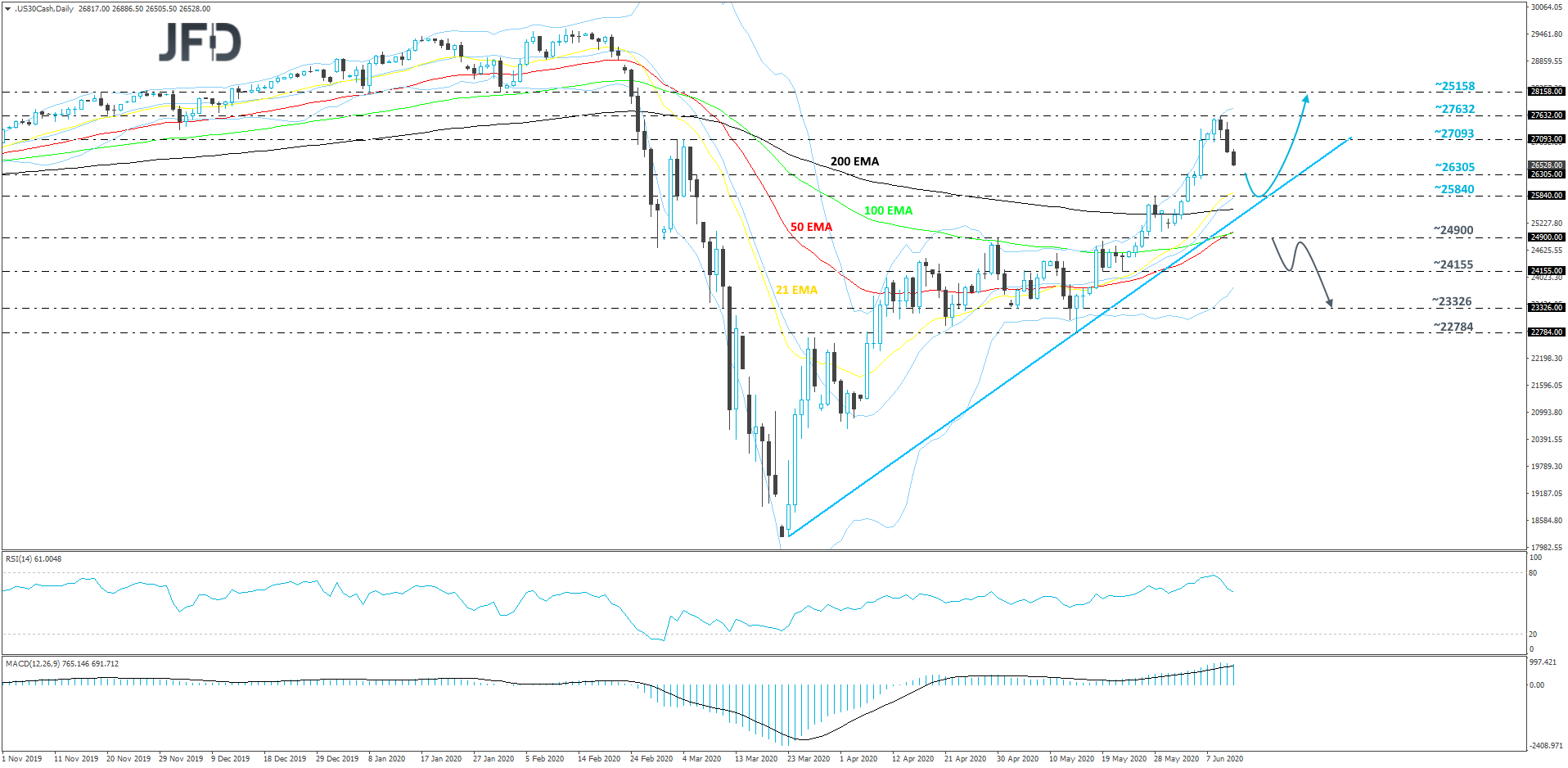

DJIA – TECHNICAL OUTLOOK

After hitting it’s two-month high, at 27632, the Dow Jones Industrial Average index started shifting slightly lower. However, if the possible further slide gets halted near the 25840 hurdle, marked by the highest point of May, or near a short-term tentative upside support line taken from the low of March 23rd, that move lower could be considered as a temporary correction, before another leg of buying. We will take a cautiously-bullish approach for now.

As mentioned above, if DJIA gets a hold-up near the above-discussed 25840 zone, or near the aforementioned upside line, the bulls may try to take advantage of the lower price. If so, this could help the index to move higher again, where a push back above the 26305 area may increase DJIA’s chances of aiming for the 27632 barrier, marked by the current highest point of this year. If that barrier surrenders to the buyers and breaks, the next potential support level could be at 28158, marked near the lows of January 8th and 31st.

On the downside, if the aforementioned upside line gets violated and the price slides below the 24900 zone, marked by the highest point of April, this would also place DJIA below all of its EMAs on the daily chart. Such a move could increase the chances for the index to drift further south, initially aiming for the 24155 obstacle, a break of which might set the stage for a move to the 23326 level, marked by the low of May 15th.

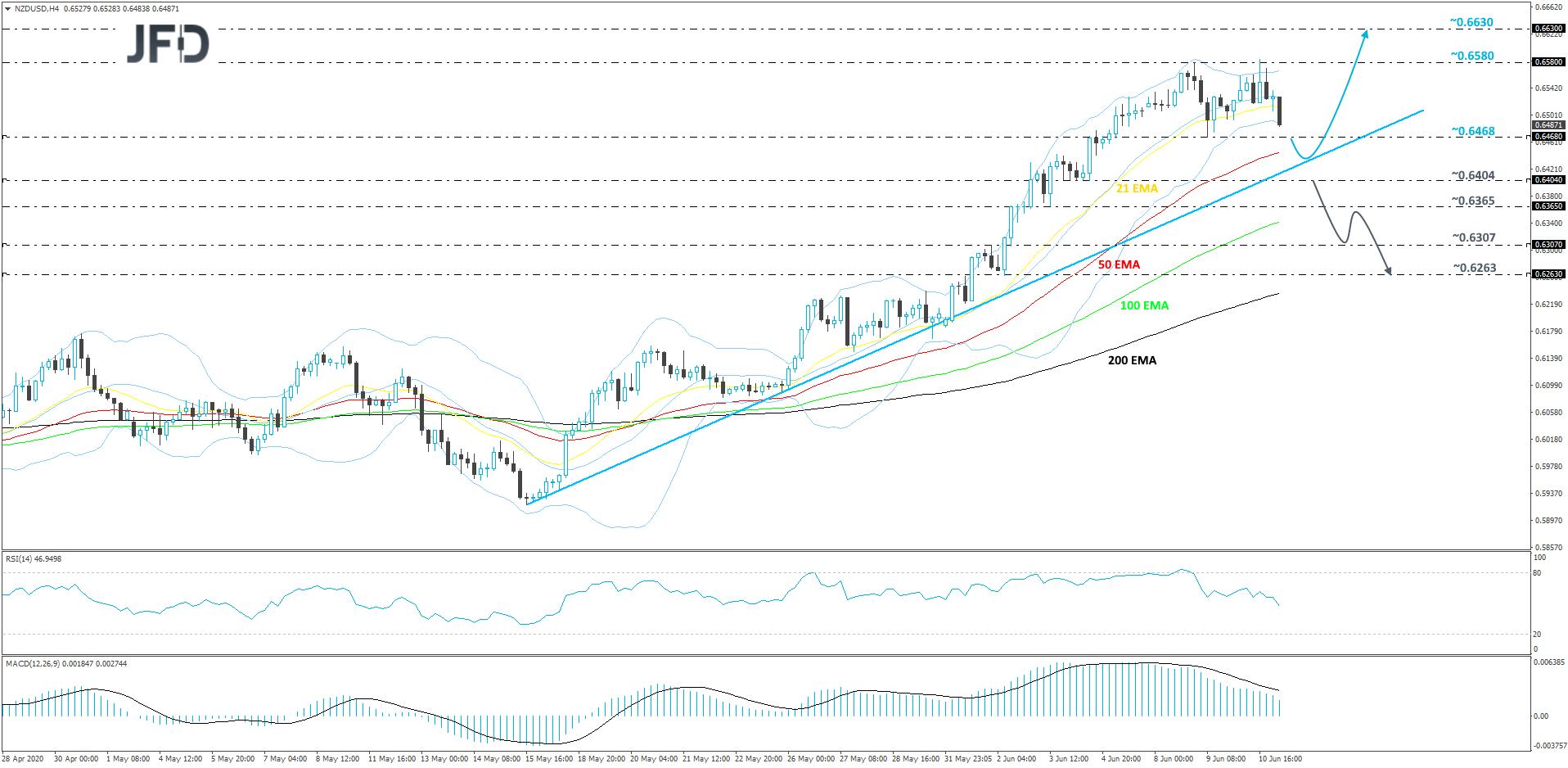

NZD/USD – TECHNICAL OUTLOOK

Yesterday, NZD/USD once again failed to stay above the 0.6580 barrier, marked by the lows of January 22nd and 23rd. This helped the bears to step in again and this morning we are seeing the pair drifting a bit lower. The slide may continue, however, as long as the rate stays above the short-term tentative upside support line taken from the low of May 15th, we will class that slide as temporary correction before another leg of buying.

If NZD/USD moves a bit further south, below the 0.6468 hurdle, which is the low of June 9th, that may test the aforementioned upside line. If that line provides a good hold-up and the rate rebounds, the pair could travel back above the 0.6468 obstacle and target the 0.6580 barrier once again. If this time NZD/USD manages to overcome and stay above it, this would confirm a forthcoming higher high and could clear the way to the 0.6630 level, marked by the high of January 24th.

Alternatively, a break of the previously-discussed upside line and a rate-drop below the 0.6404 hurdle, marked by the low of June 4th, may temporarily spook the bulls and allow the bears to dominate the field. NZD/USD could then travel to the 0.6365 obstacle, a break of which might push the rate further down towards the 0.6307 zone, marked by an intraday swing high and an intraday swing low of June 2nd. That area may provide some good support, from which the pair could rebound. However, if NZD/USD remains somewhere below the 0.6400 territory, another round of selling might be possible. If so, a move lower could once again test the 0.6307 obstacle, a break of which might clear the path to the 0.6263 level, marked by an intraday swing high of June 1st and the low of June 2nd.

AS FOR TODAY’S EVENTS

During the European morning, Sweden’s inflation numbers for May are due to be released. Both the CPI and CPIF rates are forecast to have remained unchanged at -0.4% yoy, but as it is always the case, we prefer to pay more attention to the core CPIF rate, which excludes energy. That rate slid to +1.0% yoy in April from +1.5% in March. When they last met, Riksbank policymakers decided to continue purchases of government and mortgage bonds up to the end of September 2020 and to leave the repo rate unchanged at 0.0%. They also said that the measures will be adjusted to economic developments. Thus, a potential rebound in the core CPIF metric may raise some speculation that the world’s oldest central bank may start scaling back its QE at some point soon.

From the US, we get the PPIs for May and initial jobless claims for last week. The headline PPI rate is forecast to have declined to -1.3% yoy from -1.2%, while the core one is anticipated to have slid to +0.4% yoy from +0.6%. With regards to initial jobless claims, they are expected to have slowed further, to 1.55mn from 1.87mn the week before.

Apart from the data, we also have an EU finance ministers’ meeting, where ministers are expected to discuss a coronavirus rescue fund. The euro traded in a fly mode recently, perhaps due to the announcement by the EU Commission over a EUR 750bn rescue plan, and an official approval may keep the currency supported. On the other hand, a failure to seal an accord over the aforementioned proposal may prompt some EUR-bulls to liquidate their positions and force the common currency to correct lower.

As for tonight, during the Asian morning Friday, Japan’s final industrial production for April is due to be released, with the forecast expected to confirm the preliminary print of -9.1% mom.