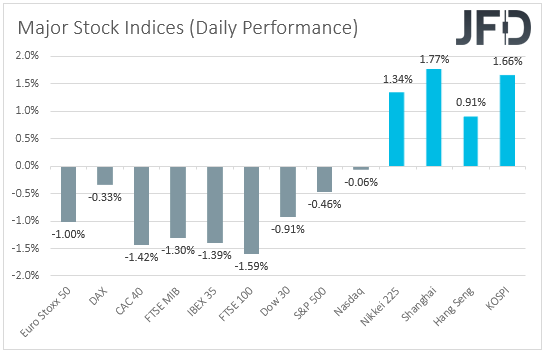

Equities retreated on Monday, perhaps due to end-month portfolio rebalancing, but Asian stocks traded higher today, as China’s Caixin PMI rose to a more-than-three-year high. Overnight, we also had an RBA policy decision, with officials standing pat and reiterating their readiness to do more if needed, while today, Fed Chair Powell and Treasury Secretary Steven Mnuchin will testify before Congress.

AUSSIE UNFAZED AFTER RBA, POWELL AND MNUCHIN TESTIFY

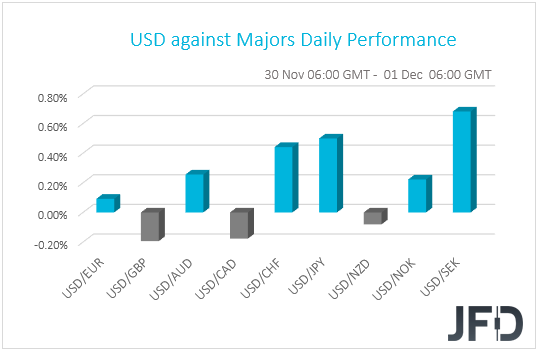

The US dollar traded higher against the majority of the other G10 currencies on Monday and during the Asian session Tuesday. It slightly underperformed only versus GBP, CAD, and NZD, while it gained the most against SEK, JPY, and CHF.

The strengthening of the US dollar suggests that markets traded in a risk-off fashion for most of the day. However, the weakening of the Japanese yen and the Swiss franc points otherwise. Thus, in order to get a clearer picture with regards to the broader market sentiment, we prefer to turn our gaze to the equity world. There, major EU and US indices finished their trading in negative waters, perhaps due to end-month portfolio rebalancing. Nonetheless, Asian indices were in the green, perhaps due to China’s Caixin manufacturing PMI rising to 54.9 from 53.6, beating estimates of a downtick to 53.5. This is the fastest expansion in factory activity in more than three years, and following the latest upbeat developments over a potential coronavirus vaccine, it may have increased hopes of a swift economic recovery around the globe in 2021.

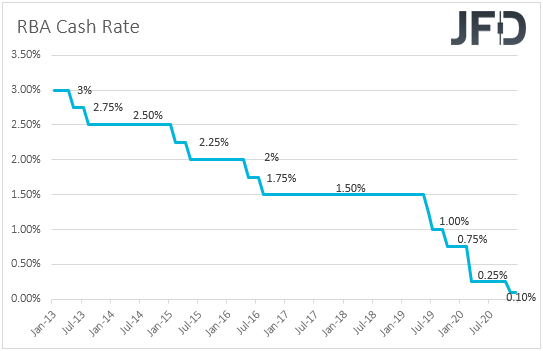

Overnight, we also had an RBA monetary policy decision, with officials standing pat and repeating that they are prepared to do more if necessary. As we noted yesterday, with Governor Lowe noting last time that a negative rate is “extremely unlikely”, we believe that if any new easing is needed, this will come in the form of QE expansion. That said, with the Bank noting that the Australian economic recovery is underway, and that recent data have generally been better than expected, we don’t see the case for further action any time soon. For now, AUD-traders are likely to keep their gaze locked on developments surrounding the broader market sentiment. On that front, we stick to our guns that the positive vaccine headlines, combined with a Joe Biden presidency in the US, may keep investors’ morale, and thereby the risk-linked Aussie, supported.

As for today, market participants are likely to pay extra attention to the testimony of Fed Chair Jerome Powell and Treasury Secretary Steven Mnuchin before the Senate Banking Committee. Tomorrow, the two officials will appear before the House of Financial Services Committee. They will testify on the CARES Act, under which Congress made USD 2 trillion available to the Treasury as a coronavirus aid, a large portion of which was aimed to support the FOMC’s lending programs. Less than a couple of weeks ago, Mnuchin cut off the programs, requesting the Fed to return unused funds and declined any extension. With all that in mind, it will be interesting to see what the two officials have to say on the matter, and whether Powell will hint at other ways in stimulating the US economy from a monetary policy front. The US government has yet to agree with Congress on a new fiscal package, something that makes the case for the Fed to act in December more likely. Thus, if Powell adds more fuel to that view, the US dollar and other safe havens could come under selling pressure, while riskier assets, like equities, may drift north.

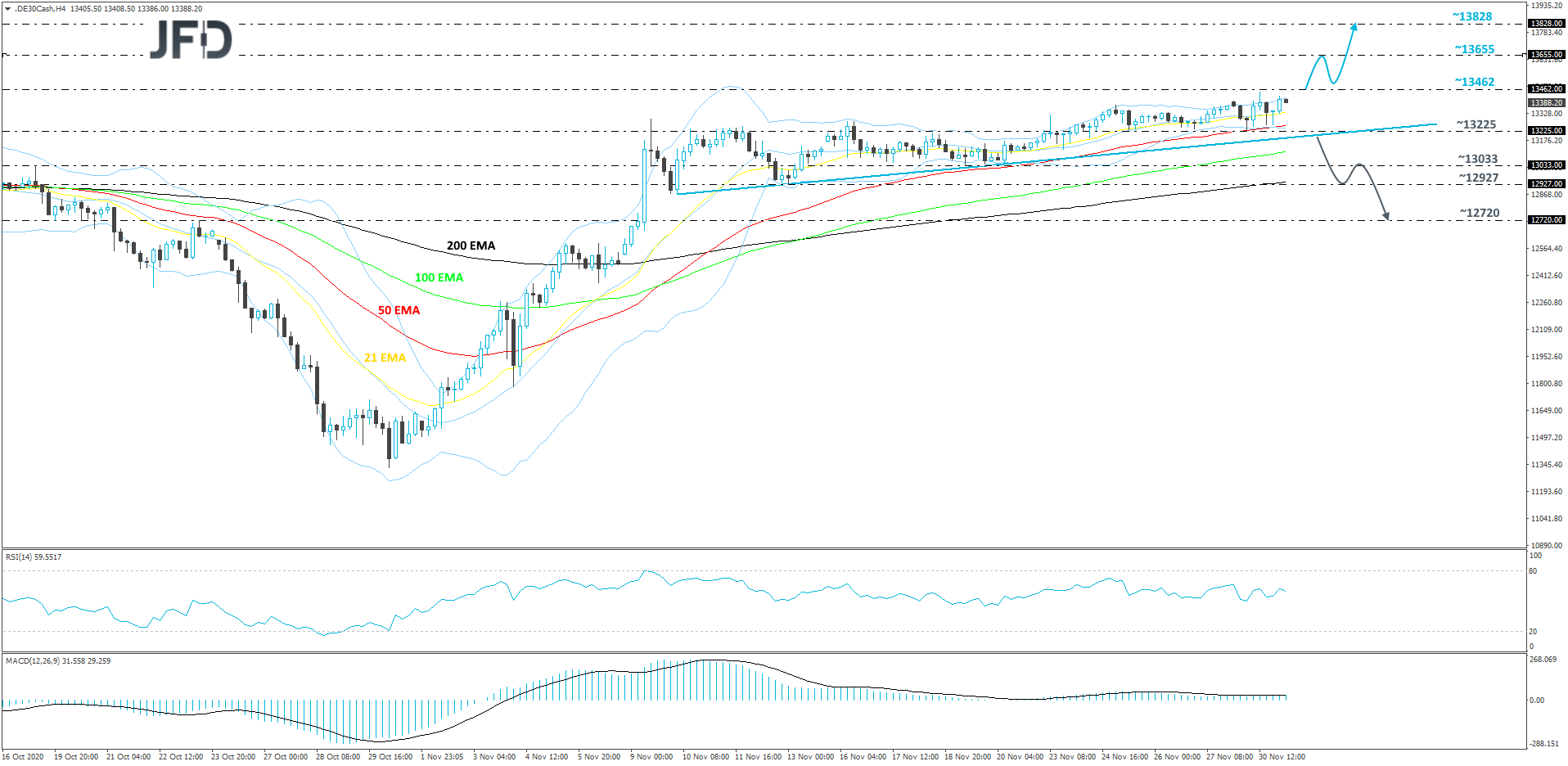

DAX – TECHNICAL OUTLOOK

Although DAX is not having the same strong moves higher, as it had in the first half of November, still, the index continues trade above a short-term upside support line taken from the low of November 10th. However, in order to get a bit more comfortable with larger extensions to the upside, we would first prefer to wait for a push above the highest point of September, at 13462.

If, eventually, we do see a pop above that 13462 barrier, this will confirm a forthcoming higher high, possibly opening the door to some higher areas. DAX might then travel to the 13655 zone, which is the inside swing low of February 18th, where the price might get halted for a while. The index may even retrace back down a bit, however, if it stays above the previously mentioned 13462 area, the buyers could re-enter the game again. If the buying pressure is able to lift the price above the 13655 hurdle, the next possible target could be at 13828, marked by the highest point of February.

On the downside, if the aforementioned upside line surrenders, this may signal a change of the short-term trend, potentially inviting a few more sellers into the arena. DAX could then drop to the 13033 obstacle, or to the 12927 zone, marked by the low of November 13th, which is also near the 200 EMA. The slide might initially stall there for a bit, however, if the sellers are still feeling comfortable, the next potential aim might be at 12720, marked by the high of November 23rd.

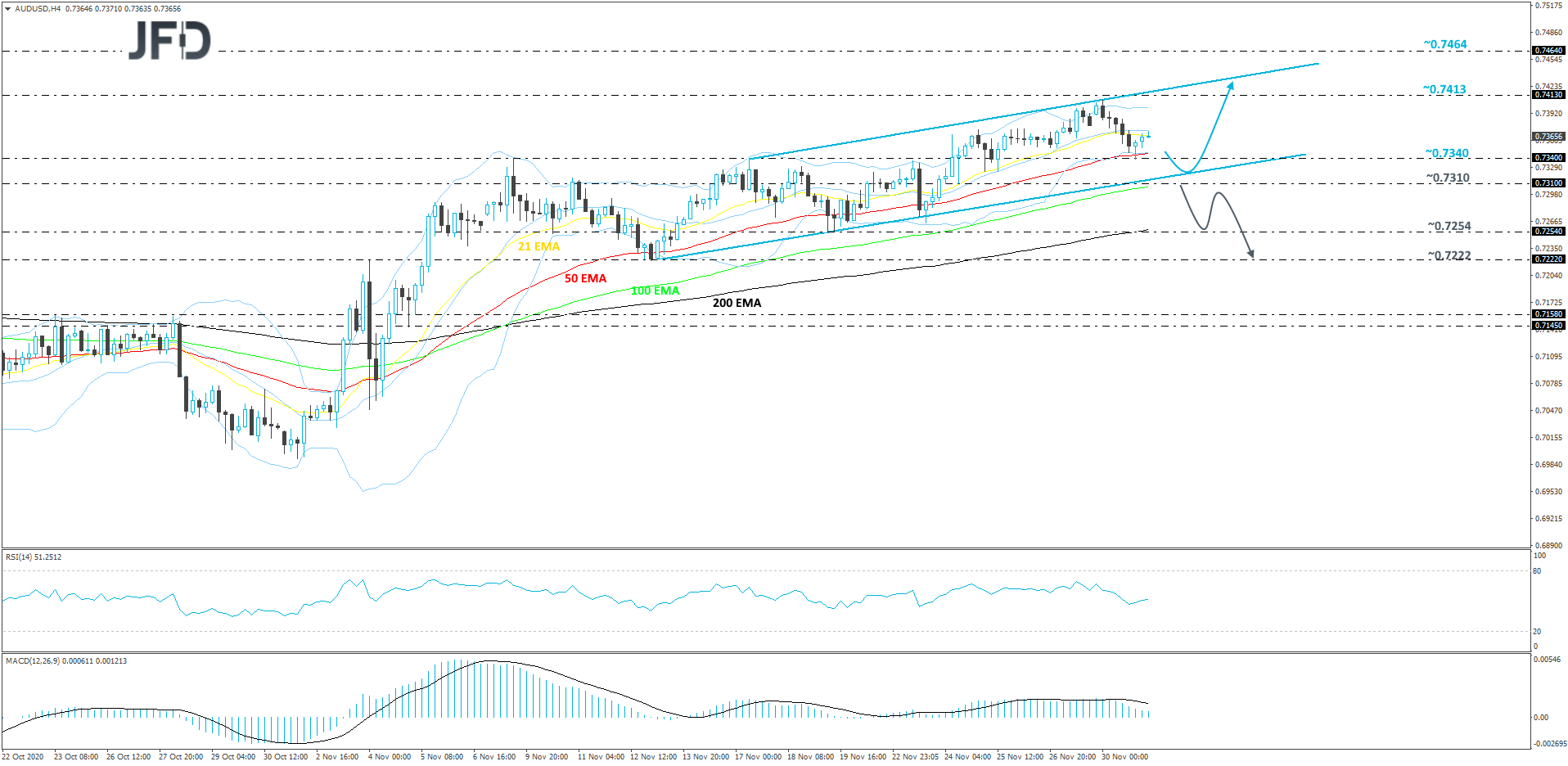

AUD/USD – TECHNICAL OUTLOOK

AUD/USD continues to trade inside a short-term rising channel pattern, which has been in play from around mid-November. After last week’s test of the upper bound of that formation, the pair corrected back down a bit. That said, if the rate remains inside that pattern, we could see AUD/USD continuing to slowly grind higher. For now, we will take a somewhat positive approach.

A small decline could bring the pair to yesterday’s low, at 0.7340, or to the lower side of the rising channel. If that area provides good support and a good territory for a rebound, the pair may end up aiming for the 0.7413 hurdle, marked by the highest point of September. Initially, the pair might stall there for a bit, but if the buying doesn’t end there, the next target may be the upper side of that rising channel.

Alternatively, if the lower bound of the aforementioned pattern breaks and the rate also slides below the 0.7310 zone, marked by an intraday swing low of November 24th, that would also place the pair below the 100 EMA on our 4-hour chart. More sellers could see this as a good opportunity to step in. AUD/USD might then slide to the 0.7254 hurdle, marked by the low of November 19th, a break of which may clear the way for a test of the 0.7222 level, marked by the low of November 13th.

AS FOR THE REST OF TODAY’S EVENTS

Today, oil traders were expecting to learn the outcome of the OPEC+ meeting. However, the group has decided to delay talks until Thursday, according to sources, as members still disagree on whether they should increase output or extend the existing cuts. The group had been expected to increase oil production by 2mn barrels per day from January, but according to media chatter, it is now expected to delay those plans for at least three months. So, what does this mean for oil prices? Given that this is the current consensus, a three-month extension is unlikely to rock the boat and thus, we don’t expect any major market reaction. Now in case the extension is six months or more, oil prices are likely to gain, while in case we do get an output increase, we may see an extension of yesterday’s setback.

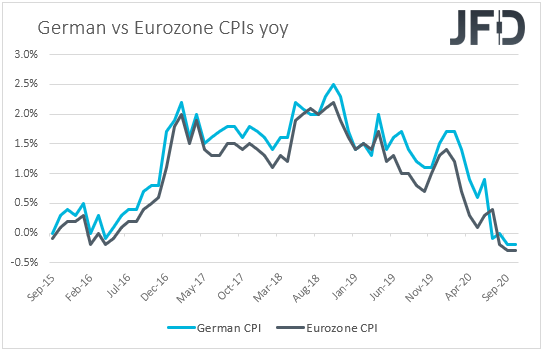

As for the data, from the Eurozone, we get the preliminary inflation data for November. The headline CPI rate is forecast to have ticked up to -0.2% yoy from -0.3%, while the HICP ex. energy and food print is expected to have stayed unchanged at +0.4% yoy. At its latest meeting, the ECB noted that in December, the new macroeconomic projections will allow a thorough reassessment of the economic outlook and that the Governing Council will recalibrate its instruments as appropriate. In other words, the ECB is very likely to expand its stimulative efforts at the upcoming gathering, and subdued inflation metrics will only add to that likelihood.

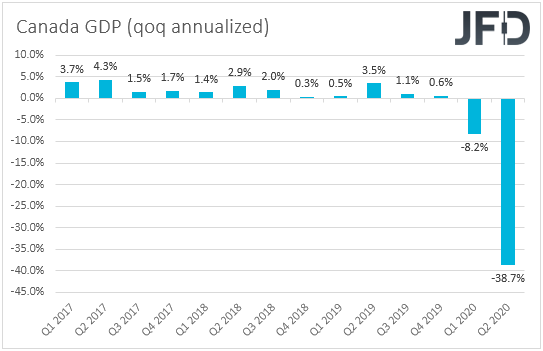

Later in the day, Canada’s GDP data for September and Q3 are due to be released. Following a tumble to -38.7%, the qoq annualized rate is forecast to have rebounded to 47.0%, though the mom rate for September is anticipated to have slid to +0.9% from +1.2%. At its latest meeting, the BoC kept interest rates unchanged and scaled back its QE program, noting that the economic outlook has evolved largely as anticipated in the July Monetary Policy Report. Thus, following the acceleration in Canada’s CPIs for October, a small slide in September’s GDP and a relatively decent employment report for November, due out on Friday, are unlikely to raise speculation for BoC officials reversing their decision at the upcoming gathering, namely expanding their QE purchases.

In the US, the most important data release on the agenda may be the ISM manufacturing PMI for November, which is expected to have slid to 57.9 from 59.3.

With regards to the speakers, apart from Powell and Mnuchin, we will also get to hear from San Francisco Fed President Mary Daly and Chicago Fed President Charles Evans.