Road transport contributes 20% of total CO2 emissions in Europe. EU legislation is progressively reducing average emissions allowed for new car fleets to 95g by 2020 (2011: 136g). SHW P&EC division will benefit from this secular trend as auto manufacturers implement technologies, co- developed with key suppliers, to meet these obligations. SHW Brake Discs is more cyclical in nature; however, management is changing the product mix to higher value composite discs. As a result, divisional EBITDA margins more than doubled to 7.9% in 2012. Following the sale of its stake in its Canadian oil pumps JV, STT Technologies, SHW will pay a special dividend of €3 per share this year. Management plans to re-enter the North American market, and cite balance sheet strength and superior European technology as key competitive advantages. There is also a demand from US OEMs for increased competition in the supplier market.

Comment On Full-Year Results

Preliminary results released on 12 February were broadly in line with expectations. Group sales grew by 2.5% to €325.4m and EBIT by 3.1% to €24.0m. Reported net income included an extraordinary gain of €31.9m related to the sale of its STT stake. Free cash flow (excluding STT proceeds) turned slightly negative in 2012, hampered by capex commitments and general working capital requirements.

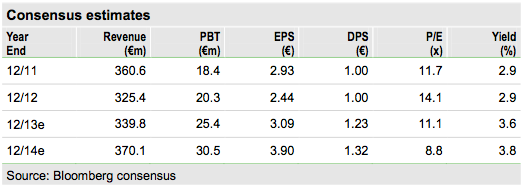

Consensus Estimates: PBT A Touch High Near Term

Management has guided for revenues of €325-€340m in 2013, which is in line with consensus. Sales growth year-to-date suggests 2013 consensus sales will be met unless end markets soften considerably. Consensus has PBT margins expanding to 7.5% in 2013, which is unlikely given the higher rate of depreciation expected this year.

Valuation: Potential For Premium Valuation

The P/E and dividend yield for 2013 are 11.1x and 3.6% respectively, which is close to the average for the sector. A premium rating could certainly be achieved if the secular growth story driven by emissions regulation starts to be reflected in the company’s results.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Quickview: SHW

Investment Summary: Long-Term Gain

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.