Paycom Software (NYSE:PAYC) reported impressive first-quarter 2018 results, surpassing the Zacks Consensus Estimate for both the top and the bottom lines. The figures also came ahead of the guided range.

Fortinet, Inc. (FTNT): Free Stock Analysis Report

Paycom Software, Inc. (PAYC): Free Stock Analysis Report

Twitter, Inc. (TWTR): Free Stock Analysis Report

Arrow Electronics, Inc. (ARW): Free Stock Analysis Report

Original post

Notably, the company adopted the ASC606 accounting standard effective Jan 1, 2018 and adjusted prior-year figures per the new standards for the ease of comparison.

The company’s non-GAAP earnings per share came in at 95 cents per share, which beat the Zacks Consensus Estimate of 90 cents. Also, reported earnings increased from the adjusted figure of 61 cents in the year-ago quarter.

Quarter Details

Paycom Software reported revenues of $153.9 million, which increased 29% from the year-ago quarter. Revenues also surpassed the Zacks Consensus Estimate of $151 million. The year-over-over increase can be attributed to new business wins and product development initiatives.

Moreover, revenues were impacted positively by a 29% year-over-year increase in recurring revenues, which comprised around 99% of total revenues.

The company’s adjusted gross margin increased 40 basis points (bps) on a year-over-year basis to 86.5%, primarily due to a higher revenue base.

Total adjusted administration expenses were $58.7 million, compared with $46.9 million in the year-ago quarter. Paycom Software’s adjusted EBITDA increased 33.8% year over year to $80.7 million.

Non-GAAP net income came in at $55.8 million compared with the adjusted figure of $35.5 million in the year-ago quarter.

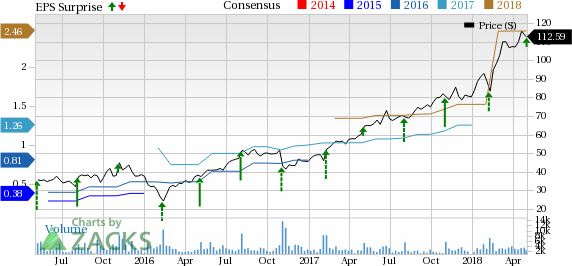

Paycom Software, Inc. Price, Consensus and EPS Surprise

Paycom Software, Inc. Price, Consensus and EPS Surprise | Paycom Software, Inc. Quote

Balance Sheet & Cash Flow

Paycom Software exited the first quarter with cash and cash equivalents of $68.1 million compared with $46.1 million in the previous quarter. Accounts receivables were $2.5 million compared with $1.6 million in the previous quarter.

The company’s balance sheet comprises long-term debt of $35.3 million compared with $34.4 million reported in the previous quarter.

It generated cash flow from operations of $57.6 million in the first quarter.

Guidance

For second-quarter 2018, Paycom Software expects revenues in the range of $123-$125 million. The Zacks Consensus Estimate is pegged at $124.6 million. Adjusted EBITDA is expected to be in the range of $43-$45 million.

Paycom Software raised its guidance for fiscal 2018. The company now anticipates revenues in the range of $545-$547 million, up from the previous expectation of revenues in the range of $541-$543 million. The Zacks Consensus Estimate is pegged at $673.7 million. Adjusted EBITDA is expected to be in the range of $220-$222 million, up from previous guidance range of $213-$215 million.

Bottom Line

Paycom Software’s management is positive about the company’s single database human capital management (HCM) solution, which is gaining clients on a regular basis. Management noted that the “actionable insights on the workforce” provided by its solutions is helping in overall improvement of human resource management.

The company received a positive feedback on the newly released redesigned “employee self-service desktop and mobile application.” The company also introduced a host of new features to the software solution that have made it more user-friendly, thereby increasing employee engagement and satisfaction.

Management was positive about its training and development as well as marketing initiatives being recognized and honoured with awards. The company is excited about the sales team count increasing to 47 with a new office recently opened in Rochester, NY.

Paycom Software is banking on increasing number of companies becoming aware of the benefits of new age human resource technologies, which will continue to positively impact the financials of the company.

Zacks Rank and Stocks to Consider

Paycom Software currently carries a Zacks Rank #2 (Buy).

Some other top-ranked stocks in the broader technology sector are Twitter, Inc. (NYSE:TWTR) sporting a Zacks Rank #1 (Strong Buy), and Arrow Electronics, Inc. (NYSE:ARW) and Fortinet, Inc. (NASDAQ:FTNT) , with a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank stocks here.

The long-term earnings growth rates for Twitter, Arrow Electronics and Fortinet are projected to be 23.1%, 10.1% and 16.75%, respectively.

Looking for Stocks with Skyrocketing Upside?

Zacks has just released a Special Report on the booming investment opportunities of legal marijuana.

Ignited by new referendums and legislation, this industry is expected to blast from an already robust $6.7 billion to $20.2 billion in 2021. Early investors stand to make a killing, but you have to be ready to act and know just where to look.

Paycom Software (PAYC) reported impressive first-quarter 2018 results, surpassing the Zacks Consensus Estimate for both the top and the bottom lines. The figures also came ahead of the guided range.

Notably, the company adopted the ASC606 accounting standard effective Jan 1, 2018 and adjusted prior-year figures per the new standards for the ease of comparison.

The company’s non-GAAP earnings per share came in at 95 cents per share, which beat the Zacks Consensus Estimate of 90 cents. Also, reported earnings increased from the adjusted figure of 61 cents in the year-ago quarter.

Quarter Details

Paycom Software reported revenues of $153.9 million, which increased 29% from the year-ago quarter. Revenues also surpassed the Zacks Consensus Estimate of $151 million. The year-over-over increase can be attributed to new business wins and product development initiatives.

Moreover, revenues were impacted positively by a 29% year-over-year increase in recurring revenues, which comprised around 99% of total revenues.

The company’s adjusted gross margin increased 40 basis points (bps) on a year-over-year basis to 86.5%, primarily due to a higher revenue base.

Total adjusted administration expenses were $58.7 million, compared with $46.9 million in the year-ago quarter. Paycom Software’s adjusted EBITDA increased 33.8% year over year to $80.7 million.

Non-GAAP net income came in at $55.8 million compared with the adjusted figure of $35.5 million in the year-ago quarter.

Balance Sheet & Cash Flow

Paycom Software exited the first quarter with cash and cash equivalents of $68.1 million compared with $46.1 million in the previous quarter. Accounts receivables were $2.5 million compared with $1.6 million in the previous quarter.

The company’s balance sheet comprises long-term debt of $35.3 million compared with $34.4 million reported in the previous quarter.

It generated cash flow from operations of $57.6 million in the first quarter.

Guidance

For second-quarter 2018, Paycom Software expects revenues in the range of $123-$125 million. The Zacks Consensus Estimate is pegged at $124.6 million. Adjusted EBITDA is expected to be in the range of $43-$45 million.

Paycom Software raised its guidance for fiscal 2018. The company now anticipates revenues in the range of $545-$547 million, up from the previous expectation of revenues in the range of $541-$543 million. The Zacks Consensus Estimate is pegged at $673.7 million. Adjusted EBITDA is expected to be in the range of $220-$222 million, up from previous guidance range of $213-$215 million.

Bottom Line

Paycom Software’s management is positive about the company’s single database human capital management (HCM) solution, which is gaining clients on a regular basis. Management noted that the “actionable insights on the workforce” provided by its solutions is helping in overall improvement of human resource management.

The company received a positive feedback on the newly released redesigned “employee self-service desktop and mobile application.” The company also introduced a host of new features to the software solution that have made it more user-friendly, thereby increasing employee engagement and satisfaction.

Management was positive about its training and development as well as marketing initiatives being recognized and honoured with awards. It is excited about the sales team count increasing to 47 with a new office recently opened in Rochester, NY.

The company is banking on increasing number of companies becoming aware of the benefits of new age human resource technologies, which will continue to positively impact the financials of the company.

Zacks Rank and Stocks to Consider

Paycom Software currently carries a Zacks Rank #2 (Buy).

Some other top-ranked stocks in the broader technology sector are Twitter, Inc. (TWTR) sporting a Zacks Rank #1 (Strong Buy) and Arrow Electronics, Inc. (ARW) and Fortinet, Inc. (FTNT), with Zacks Rank #2.

The long-term earnings growth rates for Twitter, Arrow Electronics and Fortinet are projected to be 23.1%, 10.1% and 16.75% respectively.

Looking for Stocks with Skyrocketing Upside?

Zacks has just released a Special Report on the booming investment opportunities of legal marijuana.

Ignited by new referendums and legislation, this industry is expected to blast from an already robust $6.7 billion to $20.2 billion in 2021. Early investors stand to make a killing, but you have to be ready to act and know just where to look.

See the pot trades we're targeting>>

Fortinet, Inc. (FTNT): Free Stock Analysis Report

Paycom Software, Inc. (PAYC): Free Stock Analysis Report

Twitter, Inc. (TWTR): Free Stock Analysis Report

Arrow Electronics, Inc. (ARW): Free Stock Analysis Report

Original post