Asia stocks drift lower with Fed in focus; Australia falls with RBA hold on tap

What can you expect from a passive asset allocation strategy that owns all the major asset classes? More than you might think. Owning everything has a tendency to deliver average-to-above-average returns relative to a broad set of actively managed asset strategies across the risk spectrum. Surprised? You shouldn't be.

By The Numbers

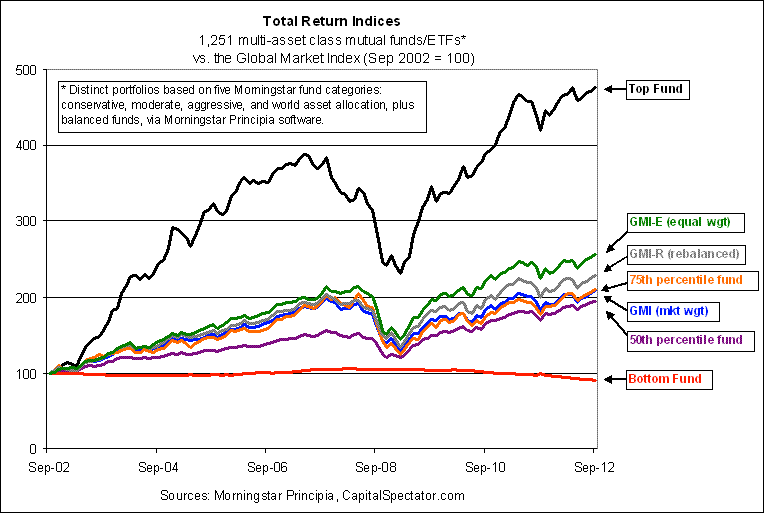

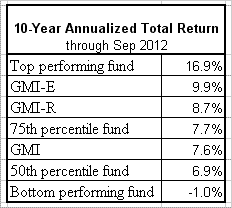

As the chart below shows, a market-value weighted mix of the standard asset classes (Global Market Index, or GMI) generated competitive returns over the last decade compared with more than 1,200 actively managed asset allocation mutual funds with at least 10 years of history. If that sounds familiar it's because it is. I update this data every so often on CapitalSpectator.com and the results don't change all that much. Back in May, for instance, I crunched the numbers on the asset allocation horse race and the message didn't look all that different from what you see in this chart:

If you simply bought and held a broad mix of asset classes, weighted the pieces by market value, you'd have done fairly well in absolute and relative terms. Rebalancing the mix back to the initial market weights every December 31 did a bit better. Equal weighting the asset classes--a model-free strategy, as I like to call it -- and rebalancing the portfolio back to equal weights at each year's end did even better.

For example, my proprietary GMI (a market-value asset allocation strategy that's never rebalanced) earned 7.6% a year for the 10 years through September 2012. That's just under the 75th percentile asset allocation fund, based on analyzing data supplied by Morningstar Principia software. The universe of active products here is comprised of 1,200-plus mutual funds that use a variety of active strategies to manage multi-asset class portfolios. This group ranges from traditional balanced funds all the way up to hedge fund-type strategies, and everything in between.

Degrees Of Mediocrity

As usual, there are a handful of funds that deliver stellar performance, along with the opposite extreme of abject failures that somehow manage to suffer unusually low and even negative returns over long spans. The vast majority, predictably, fall into varying degrees of mediocrity. As such, the operative question is: why pay more for average returns? That's a high-probability outcome if you're not careful. More than a few of the active allocation funds in Morningstar's database charge hefty fees of 1%, 2% and even higher in terms of net expense ratios. By contrast, you can replicate GMI or something comparable with ETFs for under 50 basis points.

Why not pick the best active performers and enjoy the ride? Easier said than done, of course, in part because the winners aren't a static list. Figuring out which active managers will soar in the next period, and avoiding the ones that dive, is no mean feat, which is why relatively few investors are able to routinely cash in on the leaders and earn impressive returns without taking on big risks.

Better Odds

By comparison, broadly defined asset allocation strategies offer better odds for average-to-above-average results vs. the playing field of active managers. Is the performance history in the chart above a random outcome? No, not at all, and for a variety of theoretical and empirical reasons, as I outline in my book Dynamic Asset Allocation: Modern Portfolio Theory Updated for the Smart Investor.

Can you lose money with a passive or quasi-passive strategy that owns everything? Yes, of course. Beta risk is a constant, with active and passive strategies. So, what’s the value proposition of an expansive, passive or quasi-passive definition of asset allocation? Mainly it’s a powerful tool for hedging the active risks that come in all shapes and sizes, ranging from choosing the wrong set of asset classes to reaching too high with timing rebalancing to attempting to identify winners and losers on an individual security level. Such ambitious efforts can deliver impressive results, of course, but all too often it ends up as a sizable opportunity cost for most folks.

The Takehome

The lesson here isn’t that you should slavishly own a passive mix of all the major asset classes, although you’d probably do fine with such a strategy in time. Rather, the point is that you should consider the two key factors in money management before assuming that more is always better. First, diversify broadly, across asset classes. We can have a healthy debate about what asset classes are reasonable, but I prefer to err on the side of caution by owning more rather than less.

Second, plan on implementing some form of rebalancing by trimming back on the winners and redeploying assets to the losers. That’s a dangerous proposition with individual securities, but it’s prudent when we’re talking of broadly defined asset classes. Again, the details are open for debate, but most investors can't afford to ignore this powerful tool for managing risk and, perhaps, boosting return.

Beta-Backing

I’ll be the first to admit that the finer points on how you structure and manage a portfolio are less important if -- and it's a big if -- you embrace a broad mix and put a limit on how high, or low, any one slice of the portfolio is allowed to travel. Within reason, there are many paths to engineering a satisfactory investment return over the long haul. Keep in mind, however, that not all of them come with relatively high expected odds of success.

One that does can be summed up as piggybacking on a wide mix of betas. We should certainly keep an open mind to the idea that Mr. Market’s asset allocation can be enhanced by customizing the portfolio to match each investor's risk tolerance, time horizon, etc. That’s a reasonable idea… up to a point. The problem is that too many investors (and institutions) go off the deep end.

Ultimately, all the positive alpha earned is financed by the negative alpha. The available returns going forward, in other words, are a zero sum game. It's a 'mathematical certainty', as Professor Bill Sharpe famously observed. Everyone would like to cut a bigger slice of this pie, of course, but there are constraints at the financial feeding trough. Meantime, the counterintuitive strategy of focusing on grabbing a modest slice has a habit of delivering above-average portions in the end. That’s not always obvious in the media circus of financial advice, but a sober review of the numbers helps us stay focused on how markets actually work, as opposed to how we’d like them to work.