Key Themes at Play in the Forex Market

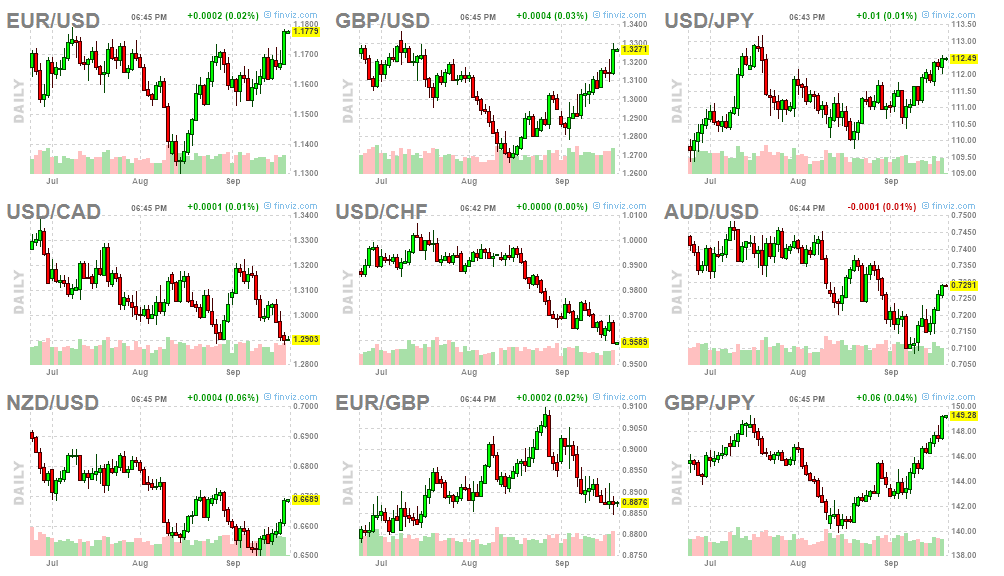

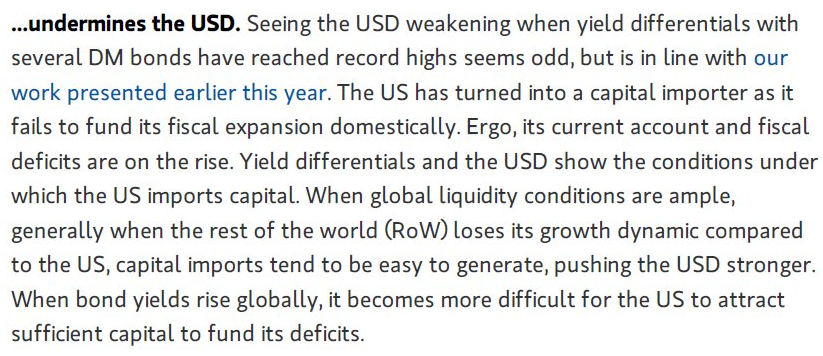

The main talking point in the forex market is the weakness in the US Dollar, with the DXY exhibiting some real technical damage just as the Euro clears the $1.1750 area with astounding ease. What’s causing this fragility in the USD even as expectations of a more hawkish narrative by the Fed into 2019 firm up? According to Morgan Stanley, it has to do with the new status of the US as a capital importer amid the inability of the country to fund its current account and fiscal expansion domestically. When the phenomenon of a rise in bond yields is not just US-centric but it’s broad-based, the US fails to attract sufficient capital.

The views by Morgan Stanley (NYSE:MS) marries quite well with the narrative of renewed momentum in global growth, which is invigorating major central banks to gradually return to a path of normalization on monetary policies. We’ve seen it in the case of the Fed, BoC, BoE, ECB is laying the foundation for a tightening campaign from mid 2019 – ECB’s Praet speech on Thursday highlights this view – and as a symbolic moment, Norway’s central bank was the last to hike rates on Thursday for the first time in 7 years. A Central Bank that still provides no hints of adjusting its expansionary policy any time soon is the SNB, mainly on fears of a Swiss Franc rise should the proverbial hit the fan and risk-off flows make a return into the CHF safe-haven appeal.

The views by Morgan Stanley (NYSE:MS) marries quite well with the narrative of renewed momentum in global growth, which is invigorating major central banks to gradually return to a path of normalization on monetary policies. We’ve seen it in the case of the Fed, BoC, BoE, ECB is laying the foundation for a tightening campaign from mid 2019 – ECB’s Praet speech on Thursday highlights this view – and as a symbolic moment, Norway’s central bank was the last to hike rates on Thursday for the first time in 7 years. A Central Bank that still provides no hints of adjusting its expansionary policy any time soon is the SNB, mainly on fears of a Swiss Franc rise should the proverbial hit the fan and risk-off flows make a return into the CHF safe-haven appeal.

The notion that even a trade war between the US and China may not have the detrimental effects initially feared is providing a cushion of hope on risky assets too. The S&P 500 closed at a fresh record high, while the Dow Jones is about to after rises of 0.78% and 0.98% respectively. The recovery in EM currencies on USD weakness is another encouraging sign. On a more broad note with direct implications on EM is a report by Bloomberg on Thursday, suggesting that China is planning to cut import taxes, applicable globally, effective in October. However, if that were to be the case, based on WTO rules, the US should also be included in this treat, which would be counter-intuitive to the retaliatory approach China probably wants to take to undermine the US competitiveness. This one is a major focal point for the markets as we head into the end of September, so keep a close eye.

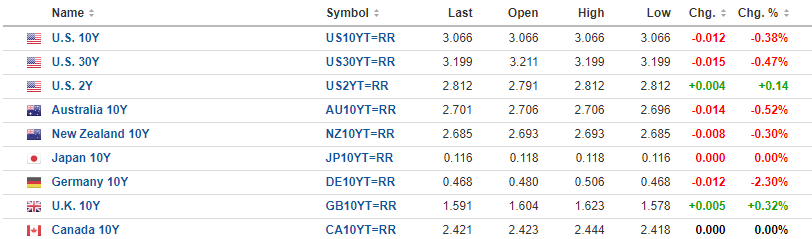

There is also an argument to be made, as Goldman Sachs (NYSE:GS) notes, that sooner or later, the continuous depreciation in the USD is going to provide some excellent opportunities to go long the currency. This view is backed by the notion that the market has an awful to reprice should, as it appears to be the case judging by US bond yields, the Fed raise its interest rate towards 3%. Clues of their intentions to hike above the long-term neutral level of 2.5% were well telegraphed by Fed’s Brainard at a speech in Detroit earlier this month and subsequently backed by Fed’s Evans. AsJan Hatzius, an economist at Goldman notes: “Many investors doubt that the FOMC will be comfortable taking the funds rate above its estimate of the ‘neutral’ level of 2.75-3.0%. We think this will be much less of a barrier than widely believed because most FOMC participants already see a restrictive stance as likely to be appropriate.”

The Sterling continues to defend its fortified position as the best performing currency in September. Judging by the price action, it’s behaving as a beacon of stability and one would think that’s a reflection of renewed optimism on the Brexit negotiations. However, after all said and done, the Brexit talks between the UK and the EU in Salzburg didn’t quite yield the results that would satisfy the Brexiteers camp, with the Irish border still a major sticking point. Even if the situation remains very convoluted, and as it becomes quite clear that the Chequers proposal won’t work, the Sterling found respite after another strong economic release, this time in the form of a +0.3% rise in UK retail sales vs -0.2% expected. The data in the UK has been so impressive that Viraj Patel, FX Strategist at ING, is now calling for 1.36-1.38 should three key conditions be met heading into October (read below). The next moment of truth in the Brexit talks is set to be on Oct 18th ahead of the Nov 17-18 summit.

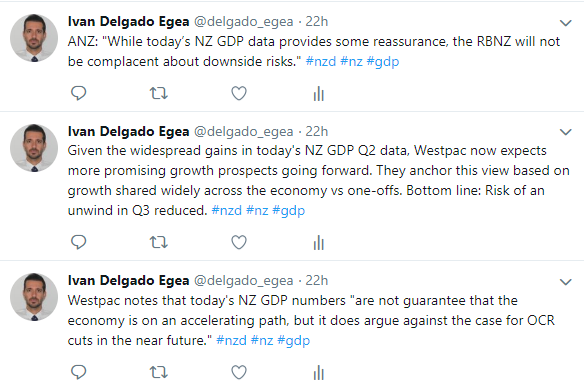

The economic growth numbers for Q2 in New Zealand came out impressively high at 1%, which led the Kiwi to rise above any other G10 FX on Thursday. The strength in the components that form the GDP was broad-based rather one-offs, encouraging NZ banks to now see strength in Q3 and Q4 numbers as well. Considering that the RBNZ had been quite cautious in its projection for growth in Q2 at 0.5%, the surprising data is probably going to see the unwinding of rate cut expectations priced into the NZD. Before the data release, the market had been discounting over 40% chances of a rate cut in the next 12 months. If economic growth starts to now develop some animal spirits and feeds through into business confidence – at depressed GFC-levels -, that’s what it may take to dispel any risk of a dovish RBNZ going forward. For now, the Central Bank is still taking comfort from the fact that the rest of the key economic indicators the likes of retail sales, inflation remain quite steady.

A currency that together with the Japanese Yen continues to be unloved as the uncertainty of a trade deal with the US continues is the Canadian Dollar. The latest we learnt, via Bloomberg, is that auto tariffs are one of the main sticking points preventing further progress. According to Bloomberg reports. “Canadian negotiators are seeking assurances the country will be exempt, or given some sort of preferential treatment, in Section 232 tariff investigations, three officials familiar with talks said. One of the officials said the 232 issue is emerging as the biggest problem, while another said it’s among a handful of key issues,” Bloomberg’s Josh Wingrove writes.

A currency that together with the Japanese Yen continues to be unloved as the uncertainty of a trade deal with the US continues is the Canadian Dollar. The latest we learnt, via Bloomberg, is that auto tariffs are one of the main sticking points preventing further progress. According to Bloomberg reports. “Canadian negotiators are seeking assurances the country will be exempt, or given some sort of preferential treatment, in Section 232 tariff investigations, three officials familiar with talks said. One of the officials said the 232 issue is emerging as the biggest problem, while another said it’s among a handful of key issues,” Bloomberg’s Josh Wingrove writes.