JPY crosses jumped to attention again as a more dovish candidate apparently moves to the fore. Meanwhile, GBP trades weaker on Moody’s downgrade while market awaits Bernanke testimony and (perhaps) Italian election results tomorrow.

The JPY tried to weaken overnight on the rumour/news that Haruhiko Kuroda of the Asian Development Bank is the favoured candidate to replace Shirakawa stop to the BoJ, with noteworthy doves also apparently in the running for the deputy governor spot. This was after the previous round of rumours that the less dovish candidate Muto appeared to be the front-runner. While JPY crosses jumped wildly higher at the Asian opening, much of that move had been undone by this writing. These headlines and rumours are the most tiresome aspect of the currency market – let’s see what this week brings, but it is interesting that this kind of move can’t hold and I still wonder whether the side of most potential volatility remains to the downside in the near term for the JPY crosses (even if I don’t want to touch these pairs due to the obvious headline risk).

UK Downgrade

Another low for the pound against the Euro and against the USD, with GBP/USD trading below 1.5100 briefly overnight after the news emerged late Friday of the downgrade of UK debt by Moody’s – an inevitability, perhaps, but still a move that was able to trigger further GBP weakness as we now have to wonder how long the 1.50 level will even hold here for GBP/USD.

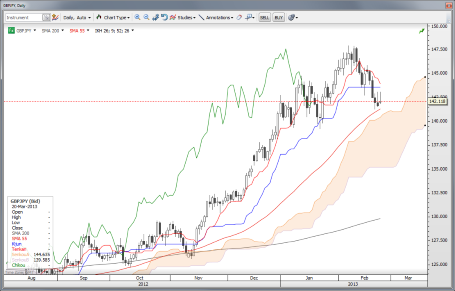

Chart: GBP/JPY

For those looking for a way to go long the JPY, it is perhaps worth noting that the GBP/JPY pair is one that has reversed course the most significantly in recent weeks. The pound’s fundamentals for weakening are actually far “better” than those for the yen, as the UK features large twin deficits and uncomfortable inflation already, while Japan has mostly internally funded massive public debt, a tiny budding trade deficit and deflation. As well, most of the JPY weakness is on anticipated, rather than actual measures. In other words, the consolidation could cut deeper (lower) for the pair in the near term. Note the approaching Ichimoku cloud level. GBP/JPY" title="GBP/JPY" width="455" height="291">

GBP/JPY" title="GBP/JPY" width="455" height="291">

Weak China flash Feb. Manufacturing PMI

The flash PMI for February from HSBC was weaker than expected, but there is the usual caveat this time of year that this may have been due to the Chinese New Year holiday, which would explain a surge of activity in January (highest reading in a long time) followed by slower activity as some take off early for the holiday. In other words – let’s see what the March data looks like before we draw too many conclusions.

Looking ahead

The highlight of the week besides the Italian election result will be the Bernanke semi-annual testimony to Congress, starting with tomorrow’s appearance before the Senate. There are two ways to look at this: on the one hand, it is clear that the likes of the FOMC minutes create a lot of noise on alternative views on the prospects of Fed policy and its appropriateness, but we have to remember that the Bernanke/ Yellen/ Dudley dovish triumvirate is in charge – so the default expectation should be that Bernanke will underline the usual dovish. On the other hand – there has to be an element of “feedback” from financial markets, i.e., Bernanke’s testimony could be on the hawkish end of his own dovish spectrum as the Fed seems to be encouraged by developments and Bernanke may hope that any near term weakness is merely a one-off adjustment from the fiscal cliff issues.

Bernanke apparently stated earlier this month that he sees little risk of a bubble forming here (how could he, when he proved in the past that he was incapable of seeing one of the greatest bubbles in financial history), but could we seem insert a small caveat somewhere in his testimony that there is the slight risk of unintended consequences at some point? If so, that could set off quite a storm of USD appreciation, even if the odds look small for this development. Otherwise, it will also be interesting to see whether the Republican opposition in Congress picks up on the “Fed enabling deficit spending” theme.

The other question here is the degree to which the market even has its eye on the Fed at the moment as we all obsess over the Italian election results. Those may begin to roll in tomorrow, though in a close vote count, not until early Wednesday. Anything besides a fairly clear Bersani/Monti coalition result is likely to weigh on the Euro in the shortest term on increased uncertainty.

Stay careful out there.

Economic Data Highlights

- China Feb. HSBC Flash Manufacturing PMI out at 50.4 vs. 52.2 expected and 52.3 in Jan.

- UK Jan. BBA Loans for House Purchase out at 32,288 vs. 34k expected and 33.44k in Dec.

- US Jan. Chicago Fed National Activity Index (1330)

- US Feb. Dallas Fed Survey of Manufacturing Activity (1530)

- Euro Zone ECB’s Weidmann to Speak (1530)

- Canada Bank of Canada’s Carney to Speak (1655)

- Australia RBA’s Debelle to Speak (2115)

- Sweden Riksbank’s Governor Ingves to Speak (2300)

- Japan Feb. Small Business Confidence (0500)