Volatility is making a serious comeback as G10 goes wild. USDJPY crosses 90 mark, EURGBP on a rampage on “Brexit” story and USDCAD pushing at 2-week highs and AUDUSD at 1.0500 despite “strong” China data.

JPY implosion continues

The JPY collapse continues, stretching beyond all normally correlated fundamental measures like yield spreads, etc., as it is all about anticipating the reality of an entirely new regime in Japan. It’s still hard to swallow the severity of this move from my perspective – I remain extremely suspicious of its sustainability in the near term even if I agree that a longer term JPY weakening is finally underway. As this move is taking place in an environment of spectacular complacency across global markets, I suspect that we risk a very ugly correction at some point in proportion to how violently the JPY has stretched weaker over the last several weeks. As well, we’re soon going to see bellyaching by other countries – particularly Europe, one suspects. China must be looking on with envy as well. This will turn into a more overt and dangerous global currency war very soon if the JPY crosses don’t soon stand down.

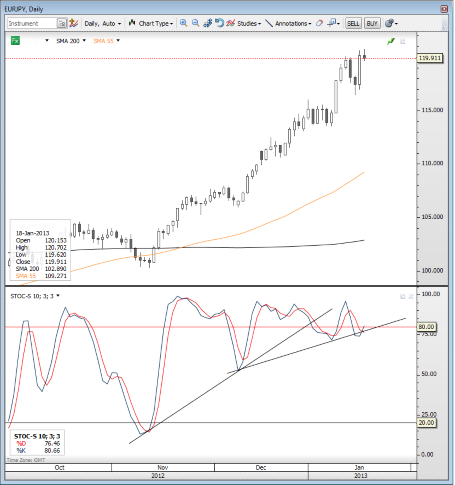

Chart: EURJPY

The highest momentum chart of late as Euro squeezes higher and JPY squeezes lower on the idea of massive intentional weakening of the JPY from Japanese authorities, including plans for ESM bond purchases. Meanwhile, the Euro squeezes higher on EU tail risks. Is the squeeze for now near completion? Seeing some signs of divergence and we have the BoJ upon us on Monday/Tuesday. The situation is ripe for a sell-the-rumour, buy-the-fact setup in the wake of that meeting next week – unless we see a sharp consolidation lower in anticipation late today/Monday. Stay tuned and don’t be fooled – there is two-way volatility danger in USDJPY crosses. EUR/JPY" title="EUR/JPY" width="455" height="485">

EUR/JPY" title="EUR/JPY" width="455" height="485">

Still weak Aussie

Chinese data surprised slightly to the upside overnight, but there isn’t enough belief invested in these numbers for the market to do anything with them but to confirm what it wants to do anyway, so after a brief pop back higher, for example, AUDUSD looked heavy by the end of the Asian session. I continue to note the divergently weak performance of the currency despite a strong day on Wall Street yesterday. It appears the tide may be turning a bit as the risk appetite correlation is losing some of its grip, though not fully so. As well, the continued aggravated rally in Euro crosses is a bit of an AUD negative as the single currency has been a favourite one to short in previous market cycles.

Brexit and all that

First it was the Grexit theme and now it’s the Brexit (UK exiting the EU) theme as speculation mounts on the UK’s status within the EU and whether it is about to undergo some kind of transformation – this is aggravating the upside to EURGBP, which was already sharp on the unwinding of EU tail risk. For more on this story – see Bloomberg’s article on Cameron’s major speech on the EU that has been delayed due to events in Mali/Algeria. I don’t have any “evolved” thoughts on this, except that this could quite possibly lead to a treaty terms renegotiation as Britain will inevitably seek to be excluded from much of the EU's banking oversight/regulation initiatives. Also, once it becomes clear that the ECB will need to open the monetary spigots in a big way, the upside could slow at some point (0.8400-0.8500 area looks important), though as I indicated earlier, my general sentiment toward GBP is becoming more bearish regardless. Today’s weak retail sales report for December didn’t help sterling’s case any.

Looking ahead

Practically nothing in the way of data for the rest of today. US Michigan Confidence is up later in the US session. It is interesting to note that after this survey posted post-2007 highs in October and November above 80, the December figure collapsed back to 73. This could have been related to the political showdown over the fiscal cliff and the lack of trust in US political leadership that it engendered. As the sequestration portion of the fiscal cliff has yet to be decided and with the ongoing debt ceiling game of chicken in the offing, it’s hard to see what has improved on that front. As well, the reality of smaller paychecks after the payroll tax cut expiry (though this effect may not be noticed by wage earners until the end of the month) could also hit confidence. Looking for confirmation elsewhere, the weekly figures have also turned, but not as much, and the Conference Board survey never posted the strong new highs late last year before dipping in December.

Economic Data Highlights

- New Zealand Q4 Consumer Prices out at -0.2% QoQ and +0.9% YoY vs. +0.1%/+1.2% expected, respectively and vs. +0.8% YoY in Q3.

- China Q4 GDP out at +2.0% QoQ and +7.9% YoY vs. +2.2%/+7.8% expected, respectively and vs. +7.4% YoY in Q3

- China Dec. Industrial Production out at +10.3% YoY vs. +10.2% expected and +10.1% in Nov.

- China Dec. Retail Sales out at +15.2% YoY vs. +15.1% expected and +14.9% in Nov.

- UK Dec. Retail Sales ex Auto Fuel out at -0.3% MoM vs. +0.1% expected and +1.1% YoY vs. +2.0% expected and vs. +2.0% YoY in Nov.

- Canada Nov. Manufacturing Sales (1330)

- US Jan. University of Michigan Confidence (1455)