We've updated our monthly workforce analysis to include last week's Employment Report for June. The unemployment rate ticked back up from 4.3% to 4.4%, and the number of new nonfarm jobs (a relatively volatile number subject to extensive revisions) surprised forecasts at 222K.

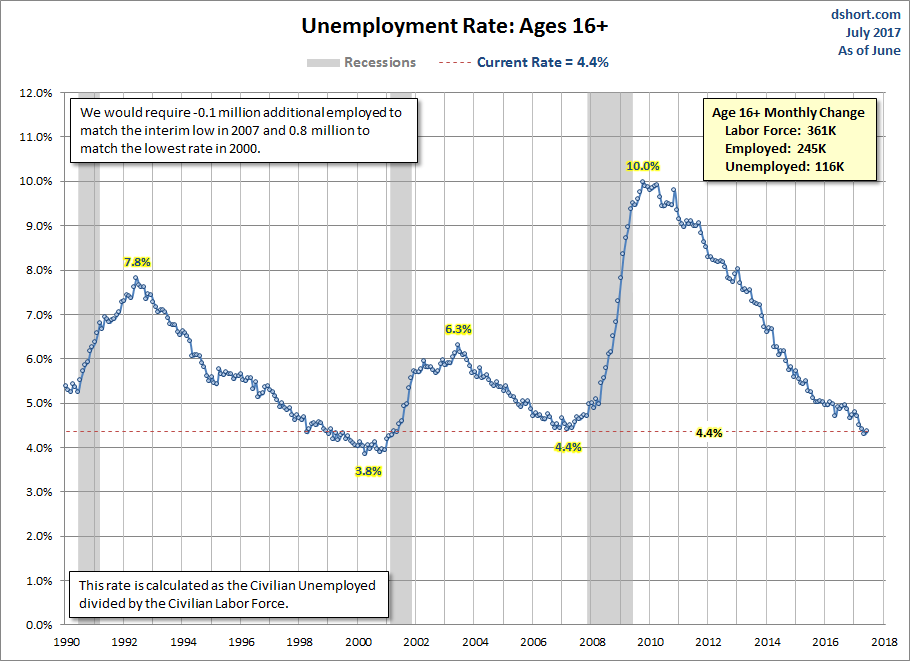

The Unemployment Rate

The closely watched headline unemployment rate is a calculation of the percentage of the Civilian Labor Force, age 16 and older, that is currently unemployed. Let's put this metric into its historical context. The first chart below illustrates this monthly data point since 1990.

In the latest report, this indicator inched up to 4.4%. The age 16+ population increased by 190 thousand, and the labor force (the employed and unemployed actively seeking employment) increased by 361 thousand. The number of employed increased by 245 thousand and the ranks of the unemployed jumped by 116 thousand. Essentially the increase in the unemployment rate was not the result of increased unemployment but rather the swelling labor force, especially the number employed.

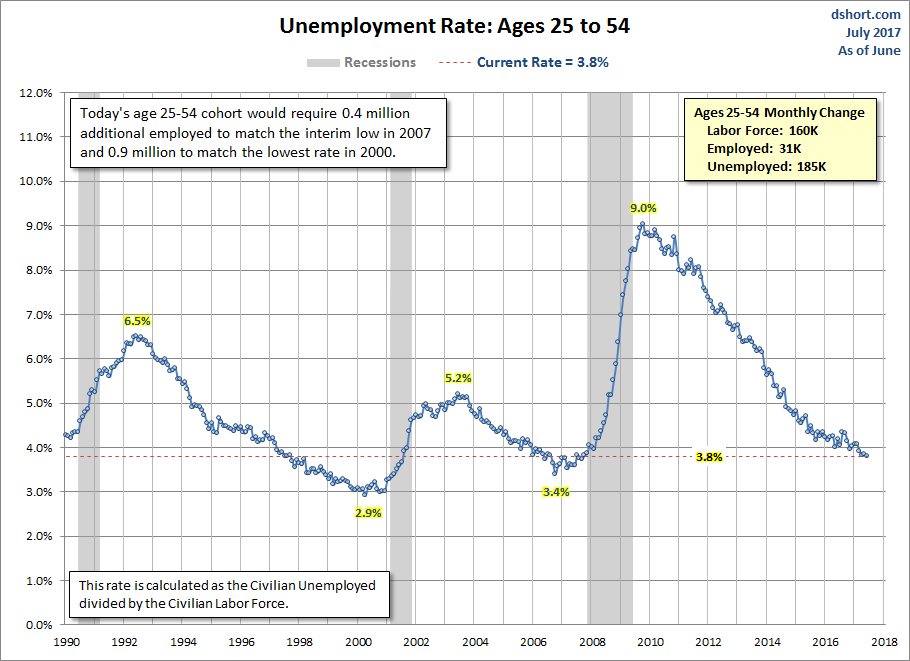

Unemployment in the Prime Age Group

Let's look at the same statistic for the core workforce, ages 25-54. This cohort leaves out the employment volatility of the high-school and college years, the lower employment of the retirement years and also the age 55-64 decade when many in the workforce begin transitioning to retirement ... for example, two income households that downsize into one-income households.

In the latest report, this indicator remained at 3.8% (to one decimal place) from the previous month. The cohort population increased by 65 thousand and the labor force increased by 160 thousand. The breakdown of the growth is an increase of 31 thousand employed and an 185 thousand increase in the unemployed. Most of the subdued labor force growth was due to the increase in the number unemployed.

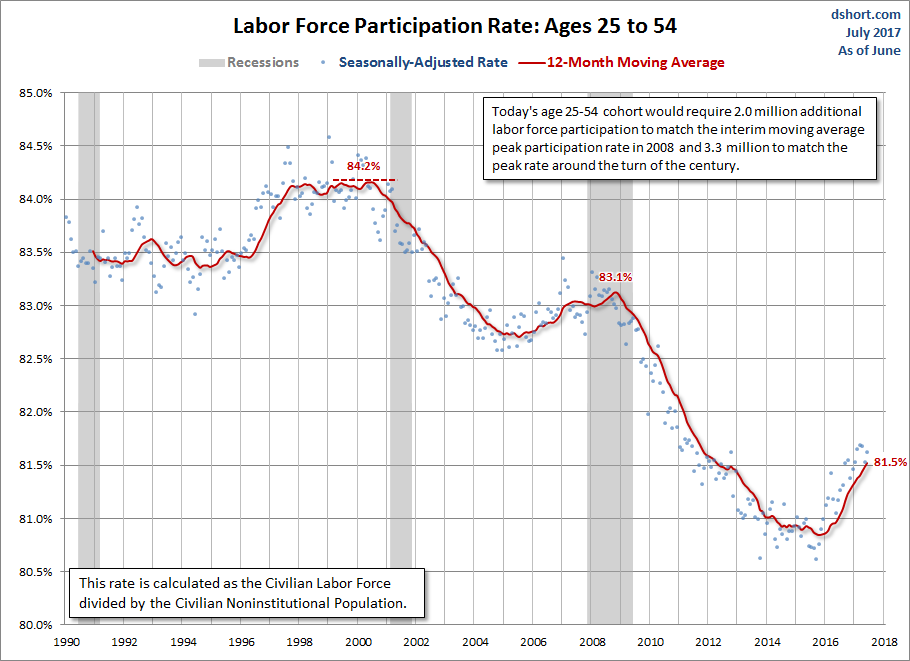

A More Sobering Measure

A wildcard in the two snapshots above is the volatility of the Civilian Labor Force — most notably the subset of people who move in and out of the workforce for various reasons, not least of which is discouragement during business cycle downturns. The chart below continues to focus on our 25-54 core cohort with a broader measure: The Labor Force Participation Rate (LFPR). The LFPR is calculated as the Civilian Labor Force divided by the Civilian Noninstitutional Population (i.e., not in the military or institutionalized). Because of the extreme volatility of the metric, our focus is the 12-month moving average.

Based on the moving average, today's age 25-54 cohort would require 2.0 million additional people in the labor force to match its interim peak participation rate in 2008 and 3.3 million to match the peak rate around the turn of the century.

Why are so many labor force participants needed for a complete LFPR recovery? When the economy is moving at full speed, as in the late 1990s, jobs are abundant, which encourages the population on the workforce sidelines to join the ranks of the employed. Today's economy doesn't offer that sort of encouragement.

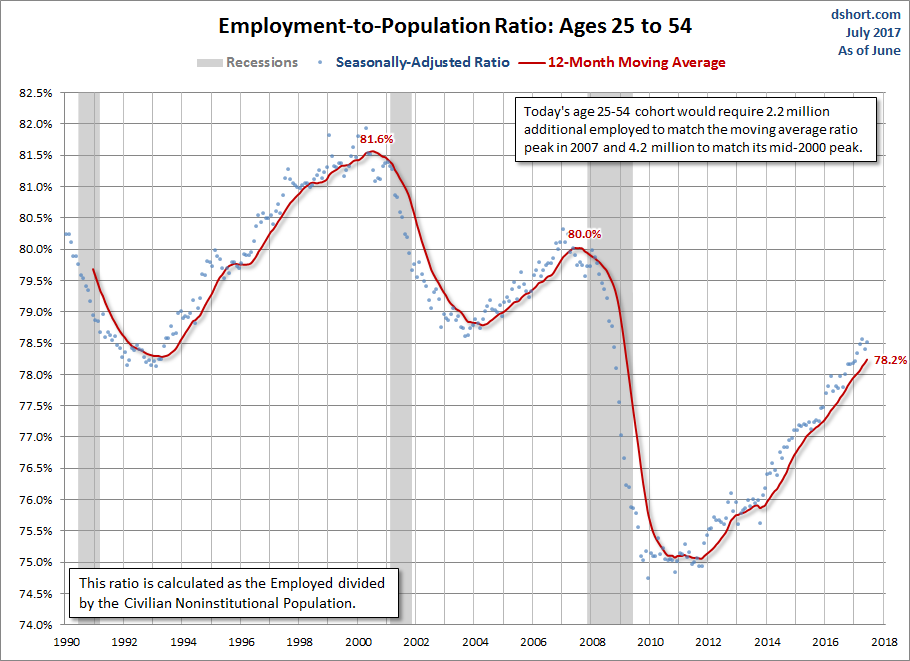

Employment-to-Population Ratio

The next chart below is calculated as the Civilian Employed divided by the Civilian Noninstitutional Population. Again our focus is the 12-month moving average. A significant feature of the Employment-to-Population Ratio is that it isn't affected by the volatility of labor force participants who, for various reasons, are unemployed.

First the good news: This metric began to rebound from its post-recession trough in late 2012. However, the more disturbing news is that the current age 25-54 cohort would require an increase of 2.2 million employed prime-age participants to match its ratio peak in 2007. To match its mid-2000 peak would require a 4.2 million participant increase.

A Structural Change in the Economy

The charts above offer strong evidence that our economy is in the midst of a massive structural change. Two of the three mainstream employment statistics — labor force participation and employment-to-population — document a structural change that seems deeper than just the result of a business cycle downturn. Unemployment has essentially reached its "natural" rate, but labor force participation and employment-to-population are both very low compared with other post-recession periods.

In order to discount the general belief that the aging of the baby boom generation is a major factor in weak employment, we've focused on the 25-54 age group. Also, by excluding the age 55-64 decade associated with early or pre-retirement, we've eliminated a cohort that might include a major source of discouraged or less-determined workers.

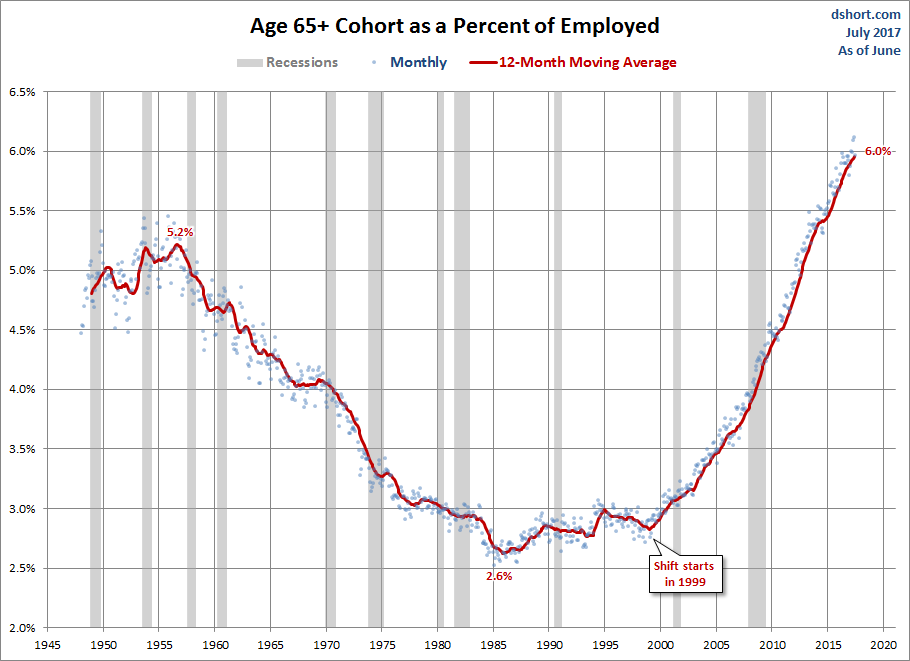

The Growth of the Elderly Workforce

Let's close this analysis with a chart that essentially demolishes the prevailing view of our aging population as a demographic drag on labor supply. Here is the ratio of the 65-and-over cohort as a percent of the employed civilian population all the way back to 1948, the earliest year of government employment data. Mind you ... these people are not only in the workforce but also actually employed.

The 12-month moving average of elderly employment remains at its historic high of 6.0% — now over double its low in the mid-1980s. This is a trend with multiple root causes, most notably longer lifespans, the decline in private sector pensions and frequent cases of insufficient financial planning. Another major factor is the often surprising discovery by many of the elderly that, financial consideration aside, the "golden years of retirement" are less personally satisfying than productive employment. Note that the growth acceleration began in the late 1990s, prior to the last two business cycle downturns (aka "recessions").

In Conclusion...

We are clearly experiencing a structural change in employment, one that continues to have a major impact on the overall economy. The fact this change was exacerbated by a business cycle downturn in late 2007 should not blind us to its structural nature.