The future’s always uncertain, and that’s not going to change when attempting to weigh the risks and opportunities for the year ahead. But this much is obvious: inflation will be front and center in 2022 as a catalyst for surprises.

The main issue is whether the recent spike in inflation will peak or not in the new year. No one knows as 2021 draws to a close, but how the answer unfolds will determine quite a lot of what happens in financial markets and the US economy in 2022. Forecasters aren’t shy about sharing their views on what they think is coming. Unfortunately, expectations are anything but uniform.

Gus Faucher, chief economist at PNC Financial Services Group, sees relatively good news ahead on the inflation front:

“I do think that we’ll see a gradual slowing in inflation throughout 2022,” he told Yahoo Finance earlier this week. “After a big run-up in energy prices, they’re going to stabilize or come down next year. I do think that a lot of the higher price pressures from the reopening of the economy are going to fade—things like airfares, hotel rooms, new cars, used cars.”

Economists at the Capital Group, however, are more cautious. “High inflation should persist longer than expected,” says Ritchie Tuazon, the firm’s fixed-income portfolio manager. In his 2022 Outlook he advises:

“Inflation levels should remain elevated through late 2022, fueled by labor shortages and broken supply chains.” In time, pricing pressure will ease, “but that process may take longer than Fed officials are expecting.”

And so it goes. The end of the year brings a surplus of year-ahead forecasts and reviews, and on the critical issue of inflation, there’s a wide range of expectations. Part of the problem is that the pandemic is creating more uncertainty than usual. That inspires a scenario-based outlook that considers several paths ahead, putting the interaction between inflation and economic activity at the core of the analysis.

Deloitte recently modeled four scenarios, each creating “unique opportunities and challenges,” as the consultancy explains:

1. Blue Skies: Prepare for post-pandemic growth opportunities by going long on debt to invest in foundational capabilities and growth-oriented M&A. Increase enterprise resiliency by diversifying supply chains.

2. Sun Showers: Mitigate rising input costs and use performance improvement to invest in growth. Take advantage of inexpensive debt early on to disrupt weaker competitors or address current weaknesses to avoid disruption.

3. Stormy Weather: Focus on increasing efficiency and lowering risk through economies of scale and cost savings strategies (e.g., automation). Diversify business models and use financial hedges to mitigate the risk of rising inflation.

4. Downdraft: Drive demand and emphasize value through new experiences and differentiated offerings. Rationalize suppliers and partnerships and consider restructuring to increase efficiency and savings.

Which scenario is likely to dominate? Good question.

“All these scenarios are consistent with the data available at the end of 2021, and any of them could begin with CPI reports continuing to show high inflation into early 2022—even higher than we see today,” Deloitte advises.

For what it’s worth, The Capital Spectator sees a case for peaking inflation, based on our Inflation Trend Index (ITI), which uses 13 indicators to estimate inflation pressure in real-time (see the list here). The current run of ITI modeling for December shows the median estimate holding steady at 4.9% for the year-over-year change.

The full range of inputs for ITI, however, remind that estimates for inflation pressure for this month come with a high degree of uncertainty.

Even if inflation is peaking, the topping-out process could extend deep into 2022. So while there’s a case for expecting the recent surge in pricing pressure to fade, that’s separate and distinct from the question of whether inflation will return to the pre-surge levels any time soon.

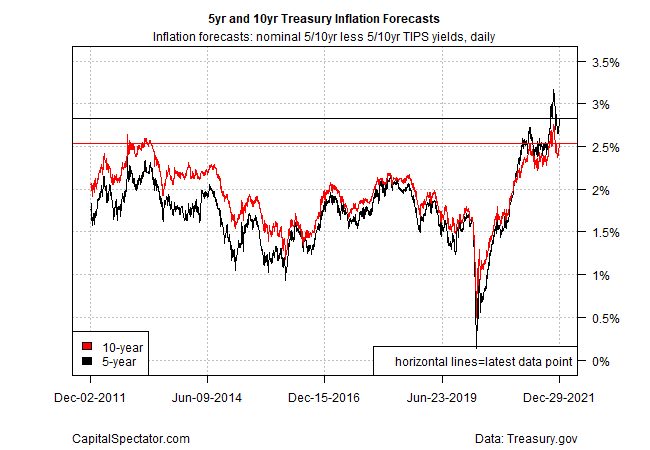

Using the US Treasury market as a guide suggests the case for peaking, while far from certain, is at least viable at the moment. In recent weeks, the market’s implied inflation forecast (based on yield spreads between nominal and inflation-indexed Treasuries) shows a modest pullback. The 5-Year maturities, for instance, are currently pricing in inflation at roughly 2.8% (as of Dec. 29), down from nearly 3.2% in mid-November.

As for hard data, the next stress test arrives on Jan. 12, when the December report for the Consumer Price Index is released. It’s anyone’s guess what the numbers will reveal, but it’s a safe bet that the upcoming CPI results will set the tone for US economic expectations in the new year. In the search for certainty on matters of inflation, that’s about as good as it gets as we bid farewell to 2021.