The recent rally in equities is beginning to show some renewed signs of pressure. Investors should expect the few fresh catalysts to steer market direction for the remainder of this quiet holiday-shortened trading week – note, trading volumes on Wall Street yesterday were relatively low.

The safer-haven USD continues to be well supported versus risky assets as both investors and dealers struggle with the fallout of the Brussels atrocities yesterday.

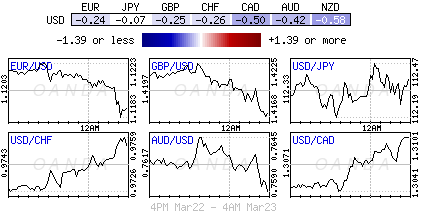

The 19-member single currency remains on the back foot (€1.1187), further pressured by upbeat comments on the U.S. economy from various Fed members (Chicago Fed President Charles Evans).

1. China’s Premier Li hints reform needed to achieve targets

China data reporting continues to be the ‘questionable variable’ with capital market fears. For dealers, analysts and speculators, there are suspected weakness regarding GDP, investment, the currency, and capital outflows, even the employment data is supposedly insufficient. Nevertheless, the call from the “top” still has the strongest influence.

Overnight, Premier Li again hinted that China’s economy would rely on reform to achieve its +6.5-7.0% GDP target range and not monetary stimulus. With that, China Securities Regulator had reportedly compiled a list of troubled companies for potential delisting and started talks with local officials to push toward exclusion from the various exchanges.

China’s yuan ended lower outright this morning, and this despite the People’s Bank of China (PBoC) setting the currency slightly stronger at the fix. The dollar closed at ¥6.4969 vs. Tuesday’s close of ¥6.4926.

According to a PBoC adviser – Huang Yiping – The future yuan direction depended on economic performance and he reiterated that currency depreciation was not in line with the goal of China.

2. Hungarian Central Bank (MNB) sideswipes markets

Hungary’s MNB has pledged to keep “cutting interest rates” until monetary conditions become sufficiently loose to ensure meeting the desired +3% inflation target for good.

In a surprise move yesterday, policy makers cut the overnight bench rate -15pbs to +1.20%. Voting members continue to see the risks of “undershooting their inflation target for a sustained period” on the back of low costs such as crude prices (Brent $41.77).

Central bank officials indicated that they would reach their inflation target much later than forecast. Staff economists have aggressively slashed this year’s inflation forecast to +0.3% from +1.7% earlier, while raising this year’s growth forecast to +2.8% from +2.5% (EUR/HUF €312.0).

3. Emerging Markets – Turkey

Naturally, after yesterday’s series of explosions in Belgium various Emerging Market currencies have come under renewed pressure and USD/ TRY ($2.8714) is not an exception. With other EM or Tier II central banks having orchestrated a surprise proactive easing move (Hungary’s MNB see above), all market eyes will be on Turkey’s central bank who convenes on Thursday to decide it’s own monetary policy.

The market consensus expects rates to remain unchanged this time around, but many analysts do see downside risks to the overall stance of monetary policy – there is considerable political pressure of late to cut rates again.

4. Brussels attacks set to intensify Brexit fears

The pound’s decline this week (£1.4170) suggests that the attacks in Belgium is set to intensify worries about a U.K exit ahead from Europe in the Brexit vote on June 23.

Sterling has continued this week’s fall, down -0.36% outright ahead of the U.S open as yesterday’s terrorist attacks on mainland Europe offer another reason for the English to vote to leave.

The technical bears are not ruling out GBP revisiting last month’s lows (£1.3835 February 16) in the short-term.

The latest Brexit ICM poll: +41% for staying in E.U vs. +43% for leaving (prior to Brussels: +43% support staying while +41% support leaving the E.U).

5. Commodities prices soften, dealers eye stockpiles

The prospect of further interest-rate tightening by the Fed is lifting the USD across the board for a fourth consecutive day – the longest winning streak in four-weeks.

A stronger dollar is also pushing down the price of commodities lower – oil (down -1% Brent $41.65, WTI $41.19, gold falling -1.2% to $1,234).

Traders are waiting for this morning’s EIA stockpile data for directional clarification. Earlier, weekly API oil inventory data showed that crude supply jumped by +8.8m barrels vs. +1.5m prior – the fifth consecutive week of build and the largest increase in three-weeks.