We’ve seen a further run higher in the US dollar, and again, much of the strength came at an odd time of day – late US and the Asian session overnight. As these are normally rather thin trading hours and this is an extremely low volatility environment, it’s tough to take the action at face value, i.e., that this is near-term encouragement for the USD bulls.

Yesterday’s news out of the US was largely supportive, with reasonable durable goods orders data for July (mostly in the revisions were to the June numbers, though there is hardly ever a durable takeaway from this release), and a strong US Conference Board Consumer Confidence reading - a new high for the post-GFC cycle, in fact.

The latter is curious as it sees the divergence between this survey and the University of Michigan survey, where the August num. A look at the historical record suggests that the Conference Board number often lags at large turning point. An example of this was in early 2009, when the University of Michigan Confidence readings were stabilising near mid-2008 lows while the Conference Board survey continued to shoot dramatically lower – posting an incredible 25.3 reading in February of 2009.

Russian president Putin was out making positive noises on the potential for peace negotiations with Ukraine.

The cabinet office in Japan expressed concerns on domestic demand and a minister warned against the effects of the next planned hike in the VAT.

Today’s calendar is about as barren as they come, with little of note on the agenda through tonight’s Asian session. We do have some Swedish confidence data out this morning that could trigger interest in trading EURSEK as it trades near the pivotal 9.14/15 area. Sweden’s 2-year government paper is trading at a record low just below 0.20% this morning. I think the risk for SEK tends to the downside.

Looking further ahead, the key focus for Euro pairs this week ahead of next Thursday’s European Central Bank meeting will be tomorrow’s German CPI data and Friday's Eurozone CPI data. On the other side of the EURUSD equation, we’ll need to see reasonably strong data out of the US with next week’s ISM survey releases and employment report to continue to drive the USD stronger.

The other factor affecting markets at the moment is risk appetite as we trade at 2000 in the S&P500 after an incredibly persistent

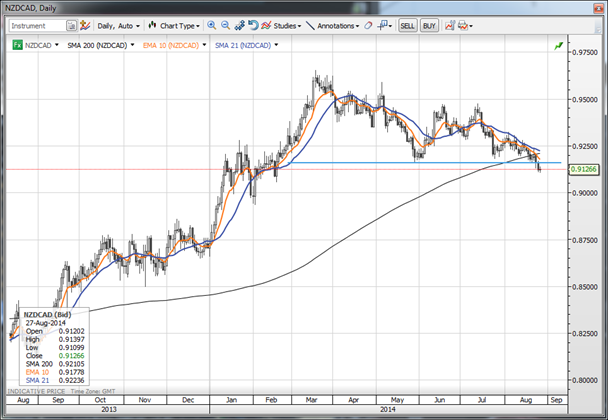

Chart: NZDCAD

Obscure cross of the day is NZDCAD, which is breaking down to new multi-month lows here. Only bringing this up as a long-term value play that could have much farther to run and because the weak NZD is one of the few clear trends going at the moment, perhaps even more so against the AUD.

CAD may enter a phase, common in its history, where its relative prospects are aided by the strength of the US economy and the USD, while NZD’s star may have peaked as further projections of Reserve Bank of New Zealand tightening have come crashing down on RBNZ protests against the strong currency, falling milk prices, and slowing housing activity.

Upcoming Economic Calendar Highlights (all times GMT)

Upcoming Economic Calendar Highlights (all times GMT)

- Sweden Aug. Consumer, Manufacturing Confidence (0600)

- Sweden Jul. Trade Balance (0730)

- Australia Jul. HIA New Home Sales (0100)