Taking a deeper look at the massive $1T U.S. market opportunity for AVs

- Mood sours amid hawkish Fed, recession fears and US shutdown risk

- Stocks mixed after last week’s losses as bond yields near cycle highs

- Dollar holds firm as yen under pressure after dovish Ueda

Subdued sentiment as uncertainties weigh

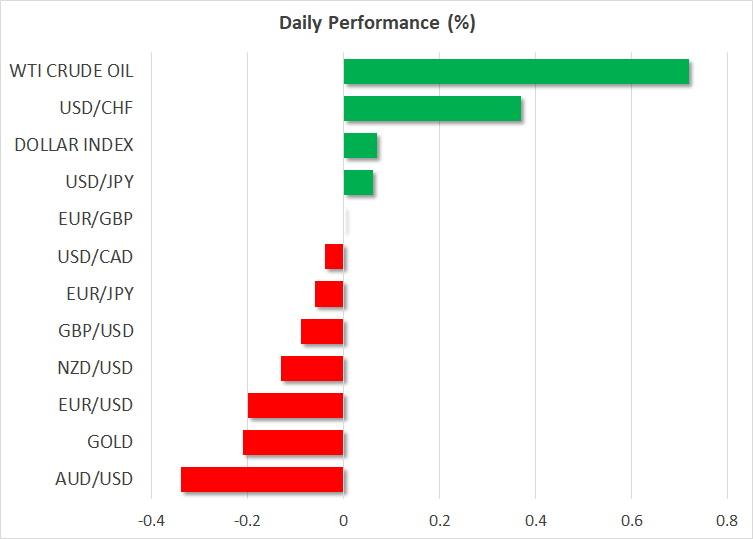

Trading got off to a mixed start on Monday as equities and the US dollar were lacking clear direction after the Fed doubled down on its ‘higher for longer’ stance and the flash PMIs reignited recession jitters.

Powell’s hawkish tone at last week’s FOMC meeting was backed by similar comments from other Fed officials on Friday, dampening hopes of a quick end to restrictive policy even if rates have peaked. More Fed policymakers will be hitting the podium this week including Kashkari today and Chair Powell on Thursday.

The September policy decisions by the Fed, European Central Bank and Bank of England likely paved the way for a pause for the rest of the year – something that the markets had been waiting for all year. However, there’s been no relief rally this time around on the back of the pause signals as the overriding message from all three central banks has been that high rates are here to stay.

What’s probably different this time is that recession risks seem more real as the Eurozone and UK economies are headed for contraction in the third quarter if the S&P Global PMI readings are any indication. Even growth in the US economy appears to have stalled in September, and with energy prices so elevated heading into the winter, the outlook has darkened substantially in the last few weeks.

Dollar hits 148.50 yen after Ueda comments

The odd one out of course from the latest round of policy meetings has been the Bank of Japan, which maintained its easing bias on Friday even as inflation continued to hover above 3% in August. What’s more significant, however, is that there were no subtle hints from Governor Ueda about the possibility of exiting from stimulus anytime soon. If anything, Ueda sounded more pessimistic in fresh remarks earlier today about the likelihood of achieving wage-driven inflation in Japan, saying there is “very high uncertainty” about whether or not the current wave of wage and price hikes by some Japanese firms would broaden across the economy.

The yen slid across the board last week, gaining only against the pound and Swiss franc after the surprise pauses by both the BoE and Swiss National Bank. But the focus is on dollar/yen today as the pair has risen to near 11-month highs, climbing above 148.50. The move comes as the 10-year JGB yield fell back today from Friday’s 10-year highs.

It’s unclear how willing officials at Japan’s Ministry of Finance are to give the intervention order as the yen’s latest decline against the greenback has been very gradual. But traders nevertheless are likely to tread with caution as the pair approaches the 150 level.

Growing headwinds for stocks

In equity markets, many Asian indices managed to recoup earlier losses to close in positive territory, although shares in China and Hong Kong slipped amid renewed concerns about China’s property market. Monday’s selloff in property stocks came after Evergrande’s debt restructuring plan ran into a roadblock.

Stocks in Europe reversed lower after a mixed open as recession fears as well as the possibility of EU-China trade frictions after Brussels opened a probe into subsidized Chinese EVs dampened sentiment.

US stock futures also swung in and out of losses, as aside from Treasury yields rising to new cycle highs, Wall Street additionally has to contend with a looming government shutdown. Time is quickly running out for Congress to agree to a funding deal before the October 1 deadline. Amidst the infighting, House Republicans are no closer to reaching an agreement on a bill that could realistically be approved by the Democrat-led Senate.

With the US economy losing some steam lately, a government shutdown coupled with worker strikes and the resumption of student debt repayments could lead GDP to contract in the fourth quarter.