In Part 1 and Part 2 of this research article, I shared my research into the state of past and current U.S. and global economies, Rest Of World Debt, DGP Implicit Price Deflator, Fed Funds Rates and other technical data charts. The purpose of this article is to share with you two key components of the current U.S. and global market trends; higher inflationary trends and a potentially trapped Federal Reserve.

I will share more data/charts, and my proprietary U.S. economy/Fed modelling systems results. My objective is to share my belief that the Federal Reserve still has room to adjust interest rates (within reason) and how the U.S.-global economy is starting to trend into the highest inflationary levels since 1975~1985. These levels could frighten traders/investors, but given the global economic constraints of the COVID lockdowns, I consider the current economic trends a symptom of the stimulus/solution – not necessarily an inherent economic trend. Allow me to explain my thinking in more detail.

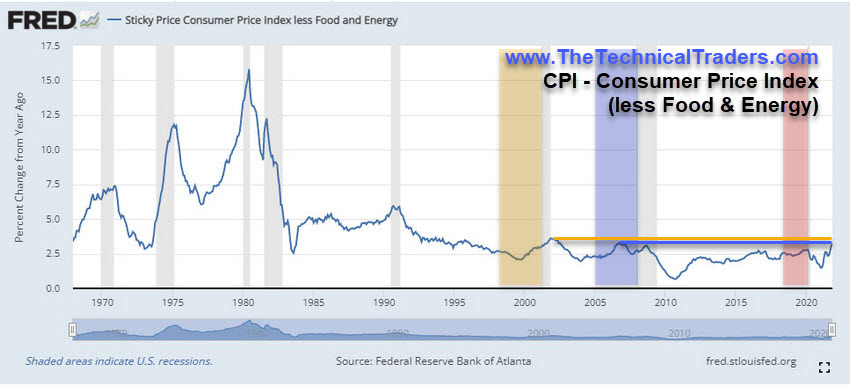

Consumer Price Index (Less Food & Energy) Climbs To Highest Levels Since 2007-08

This Consumer Price Index (Less Food & Energy) paints a powerful picture. As you are well aware, the energy sector (oil and natural gas) has rallied more than 300% over the past 18+ months. Food, in particular beef and other staple products, have rallied more than 80% over the past 18+ months. So this Consumer Price Index chart that is excluding two of the highest inflationary consumer components should already be well above the 1999-2000 levels if we consider real consumer price factors.

Take a minute to review all of these charts and consider the current U.S. and global economic environment and where you think these trends may continue into early 2022.

(Source: Fred Economic Data)

The extreme U.S. and global market debt levels, which have risen more than 500% over the past 15+ years, complicate the process of combating inflationary trends. The Fed, and many global central banks, risk a broad wave of defaults if they attempt to raise lending rates too fast. They want an orderly deleveraging process to occur, which will prompt a moderate deflationary trend in assets.

Consumer Price Indexes rallying to levels not seen since the 1970s or 1980s when the Federal Reserve continues stimulus programs and keeps the FFR levels near zero seems counterproductive. But what if the Federal Reserve is trapped behind a wall of debt and a very keen understanding that any aggressive moves may topple the global growth phase we've experienced over the past 8+ years? What if the Fed knows it should be raising interest rates right now but is frightened to take this action because of what may happen to the rest of the world?

Proprietary Modelling Of U.S. Economy/Fed

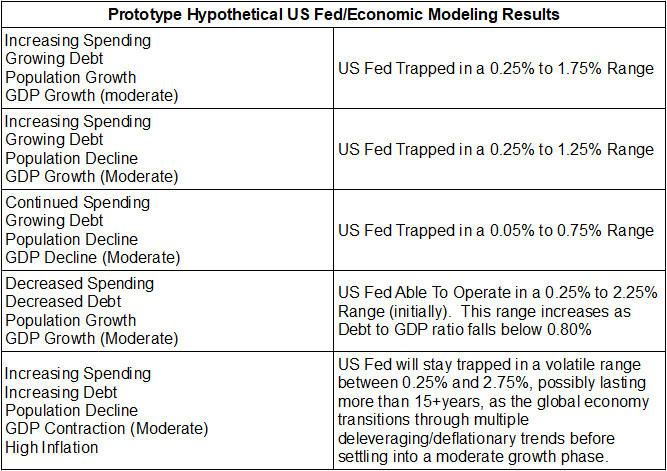

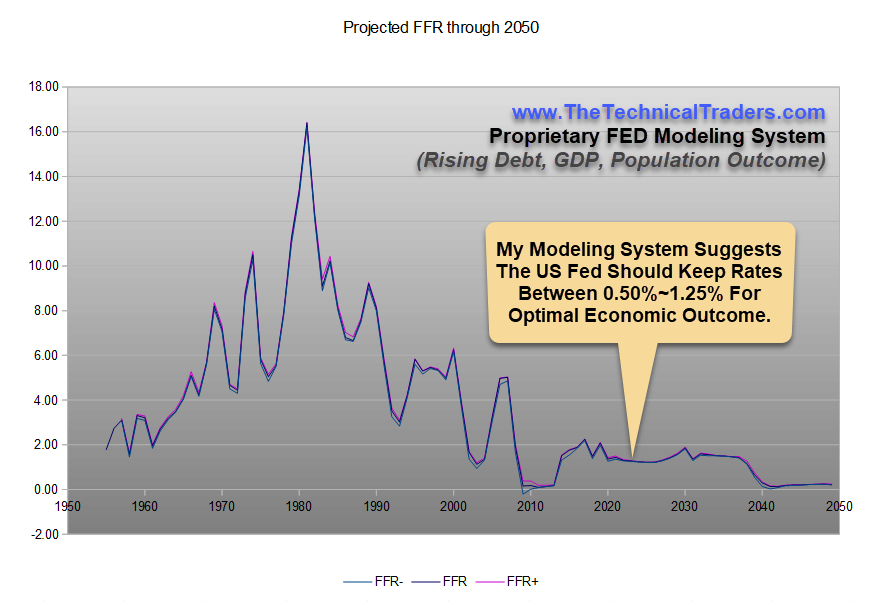

Many years ago, I completed some prototype research related to U.S. debt levels as it related to GDP, population and economic activity. At that time, I attempted to model different outcomes over the next 20 to 25+ years. I tested various hypothetical outcomes to see how my modelling system would allow the Fed to raise or lower rates within an "optimum range." I've organized the results of my theoretical modelling into a table (below).

I believe this data, and all the charts I've shared with you in the whole of this research article, suggests the Fed is trapped in a very strenuous position right now. The inflationary data suggests the Fed should be aggressively raising rates. The global markets and the fragility of the global economy based on years of stimulus and easy-money policy may prompt a shattering of market trends if the Fed acts too aggressively. What is the Fed most likely to do over the next 4 to 12+ months?

Maybe the Federal Reserve is willing to push the envelope by:

- keeping rates low

- allowing foreign markets to deleverage and devalue in an orderly process

- allowing the markets to divest of the excess liabilities/debts

At the same time, it continues to support the U.S. economy with easy-money policies, thus allowing the foreign markets to shake off the liabilities and debt levels on their own.

Telegraphing Long-Term, Slow-Motion, Fed Actions Going Forward

It makes sense that the Federal Reserve may attempt to raise interest rates very slowly in 2022, possibly moving 1/8% or 1/4% at a time, while keeping the FFR lending rate below 1.0% to 1.25%. Remember, my research suggests any aggressive moves by the Fed could topple the U.S. and global markets fairly quickly at these extended inflationary and consumer price trends.

A prolonged and properly telegraphed U.S. rate rise, moving interest rates up above 0.50% would be a suitable solution, in my opinion, to attempt to eliminate the excessive leverage that has taken place throughout the developing world. As we see in China, Asia, Africa, the U.S., and other places, economic functions tend to have a natural process of handling extreme excesses.

My opinion is the world is experiencing and seeing the symptoms of excessive stimulus, extended easy monetary policy, COVID lockdown supply issues, and the effects of manufacturing globalization through the process of a virus/pandemic event. Almost like a perfect storm, the global markets before COVID in February 2020 were uniquely positioned to be highly dependent on China/Asia for certain medical, chip and other manufacturing components while shipping and supply trends collapsed. For the first four to 6+ months, the U.S. worked through existing inventory/supplies. But after those supplies were exhausted, the US economy became dependent on new shipments to replenish inventory and to supply much-needed manufacturing components. This perpetual supply-side shortage has continued to prompt higher inflationary trends worldwide.

Slowly Changing Direction

I expect the Federal Reserve to very clearly telegraph next year's expectations with an evident intent to move away from extended stimulus and support programs slowly. A very slow rate increase, possibly moving rates above 0.50% before August 2022, could be in the works. The Federal Reserve will want to adjust rates and policy to assist the global economy in efficiently transitioning through the current inflationary, deleveraging, and deflating the excessive price trends – not breaking the markets.

Expect the Federal Reserve to announce very clear longer-term “intentions” and to telegraph its expectations related to inflation and supply issues. Here are my expectations in a nutshell:

- Potentially cut the bond-buying rates by another 15% to 45% in early 2022 (Q1:2022 through Q3:2022).

- Announce intentions to raise rates very slowly in late Q1:2022 or late Q2:2022 (possibly raising in tiny increments over many months).

- Announce the Fed is watching the global markets and credit markets quite intently - attempting to identify subtle shifts in trends and activity while adjusting future actions/expectations.

The Federal Reserve has room to raise rates 0.50% or a bit higher. It also has many other tactics to tighten (bond-buying, liquidity features, financial stress-based requirements). I believe the Fed will make very clear “baby steps” known – but not take any immediate actions.