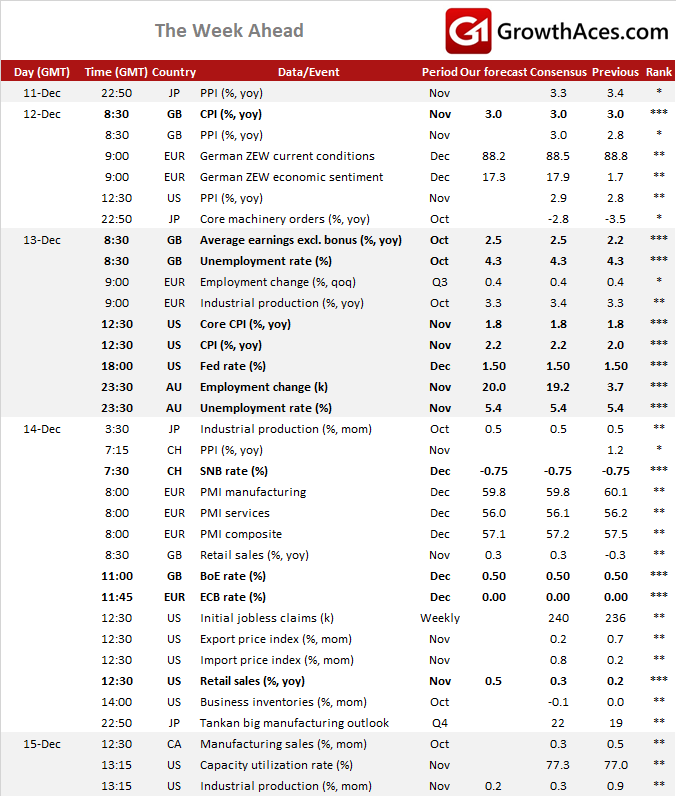

Yellen’s final rate hike

- Next week, the Federal Reserve will end its eighth and final regular FOMC meeting of the year. We expect the committee to announce another 25bp rate hike, which lifts the target range for the federal funds rate from 1.25% to 1.50%. By hiking for the third time this year, the Fed will have met its forecast made in late 2016. This is an important shift compared to the previous two years, when the FOMC had projected a total of four hikes for the following calendar year, but ended up raising its target rate only once.

- Behind this positive development is, of course, a much more stable global economy that has produced no meaningful shock this year that was strong enough to affect the US economy. Moreover, as the labor market has continued to tighten, the Fed was even willing to look through what it deemed to be a transitory weakness in core inflation readings, and continued its policy normalization during the summer. Furthermore, the most recent improvement in both the core CPI and the core PCE deflator should have alleviated the biggest concerns of the more skeptical FOMC members and strengthened the committee’s confidence in its own, rather sanguine inflation outlook. We, therefore, do not anticipate any major changes in the statement or the updated Summary of Economic Projections.

- Most importantly, we anticipate that the FOMC members’ median interest rate projections (the “dots”) continue to show another three rate hike for next year, followed by two more in 2019 and another one in 2020. Certainly, the distribution of the dots for 2019 and 2020 has been pretty wide in September, which means that forecast changes of just a couple of FOMC members can shift the median dots in the one direction or the other. But the most important forecast for 2018 should stay the same, and the outlook for a gradual normalization remain in place as well. That is also reflected in the fact that the economic and inflation projections should be largely unchanged compared to September. That implies ongoing GDP growth of around 2%, a decline in the unemployment rate towards 4%, and – most importantly – a return to 2% inflation by the end of 2018. Finally, the post-meeting statement is unlikely to contain important changes either. Most importantly, it will reiterate that the committee expects that “economic conditions will evolve in a manner that will warrant gradual increases in the federal funds rate”, while it “is monitoring inflation developments closely.”

- With all the written releases being almost unchanged, the market will also focus on Janet Yellen’s press conference. We think that the tone of her comments should be a little more sanguine. This is mostly due to the fact that inflation has been moving in the right direction, thus vindicating the Fed’s ongoing policy normalization during the summer. In addition, it is Janet Yellen’s final press conference in her current role. After a turbulent time, and after having successfully set the course for the Fed’s policy normalization, she may actually be slightly relieved that she will soon hand over the responsibility to her successor.

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

ECB policy on autopilot

- The ECB monetary policy is on autopilot, following the October decision to extend QE until at least September 2018 at a reduced monthly pace of EUR 30 billion. Therefore, next week’s Governing Council meeting is likely to be relatively uneventful. In our view, investors should focus on two things: 1. the ECB’s new macroeconomic projections; and 2. Possible remarks by Mario Draghi on the range of views within the Governing Council about the termination date of QE.

- The new macroeconomic projections are likely to see stronger GDP growth and an oil-driven upward revision to the short-term inflation path. Contrary to the September round of forecasts, this time the exchange rate is not going to be an issue, given that at the cut-off date of mid-November the trade-weighted euro was 1% weaker than in the previous set of assumptions. Accelerating global growth and trade, as well as surging sentiment indicators at home are likely to convince the ECB to raise its growth trajectory. We expect the new forecasts to show 2.3% expansion this year (previous: 2.2%), 2.3% in 2018 (1.8%), 1.8-1.9% in 2019 (1.7%) and 1.6-1.7% in 2020. On the inflation front, two things stand out: the strong increase in oil prices relative to the September exercise, and renewed weakness in core inflation, which has erased all the improvement recorded during the summer. Oil prices have jumped, mainly in the wake of tensions in the Middle East, with the front-end of the oil future curve up by about 20% from September assumptions, while the longer-dated contracts are about 10% higher. This is likely to lead to a hump-shaped trajectory for energy inflation.

- With regard to core inflation, the downward adjustment to 0.9% after the acceleration in the summer to 1.2% is unlikely to flag a trend reversal. Rather, it probably reflects stronger seasonality in holiday-sensitive price items compared to last year. We think that the "real" level of core inflation lies in the middle of the 0.9-1.2% range, which implies some downside risk to the ECB’s forecasts for core prices – currently at 1.3% in 2018 and 1.5% in 2019 – despite a faster narrowing of the output gap. Overall, we expect the ECB to raise its 2018 forecast for headline inflation to 1.5-1.6% from 1.2%, with the number for 2019 likely to be confirmed at 1.5% and for 2020 seen at 1.6-1.7%. These projections would continue to vindicate prudence, patience and persistence in monetary stimulus.

- In the last few weeks, a number of Governing Council’s members (including Benoit Coeure) have made statements signaling that QE should end in September. This sends a more hawkish message than that of Mario Draghi at the October press conference and probably reveals an increased split within the Governing Council about the pros and cons of QE while the recovery is clearly proceeding above potential and fully sustainably. However, this is unlikely to lead to any meaningful change in ECB rhetoric in the short term. Regardless of the exact termination date of QE – which we think will be December 2018, after a quick tapering in the fourth quarter of 2018 – it seems that we are getting more clarity on what could be the next “hawkish step” in ECB communication on the way to the exit. In his Handelsblatt interview, Benoit Coeure stated that he expects that the link between a continuation of net asset purchases and sustainable converge of inflation towards target will change when the GC is sufficiently confident about the inflation progress it has achieved. This is probably an indication that the ECB may eventually opt for more flexible language, where not just net purchases, but the overall monetary stance – given by the level of interest rates, the forward guidance, bank liquidity provision, the pace of net purchases and the size of the QE portfolio –– is linked to inflation progress. This would be a hawkish twist that reduces the importance of additional QE relative to the rest of the easing tools. We do not expect this change will happen before June.

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

BoE to stay on hold

- At its meeting in early November, the Bank of England’s MPC voted by a majority of 7-2 to raise the bank rate by 25bp to 0.50%. This was the first increase in a decade.

- Next week, we get the monetary policy announcement and MPC minutes – December is not an Inflation Report month and there will be no press conference. We expect a 9-0 vote to remain on hold. Overall, this should be a non-event.

- Investors will focus on whether there are any changes to the policy section of the minutes, after the committee said in

- November that “resolution of uncertainty about the nature of, and transition to, the United Kingdom’s future relationship with the European Union would prompt a reassessment of the economic outlook”. Brexit negotiations are slowly moving in the right direction, but it is unlikely that the latest news would convince the MPC to rethink its outlook for growth and inflation.

- UK economic activity is slowing, headline inflation will probably fall next year, domestically-generated inflationary pressure is weak, inflation expectations are well anchored and Brexit-related uncertainty remains high. Therefore, we expect the MPC to remain on hold in 2018 and hike just once in 2019.