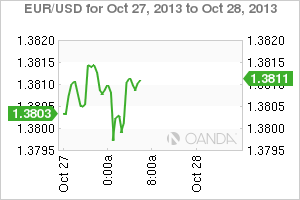

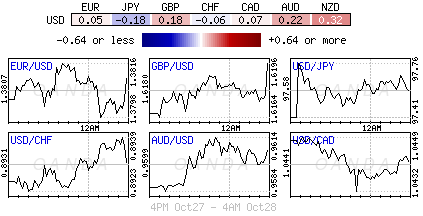

It looks like an unscheduled event is required to force any significant breakout of the current forex range. Could it be as simple as Janet Yellen beginning her Fed confirmation meetings this week? Obama's nomination for top banker in the free world will meet with US Senators this week as part of the process to install her as the next "Fed head." Everyone seems confident that she will secure the 51 Senate votes needed to confirm her position. However, the hearings are expected to be contentious- with several Republican Senators looking for their 'own' airtime and have already indicated that they will oppose her nomination. Maybe what's required is confirmation of her monetary and tapering viewpoint to get price action moving once again? EUR/USD" height="200" border="0" width="300">

EUR/USD" height="200" border="0" width="300">

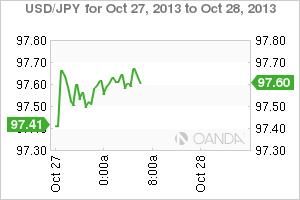

Aside from any Washington political antics not scheduled, a busy last week of the month not only sees the release of many key economic indicators but also includes four-key central bank policy announcements. The Reserve Banks of New Zealand (RBNA) and India (BoI) are expected along with the Bank of Japan (BoJ). Stateside, Bernanke and the "Boys" Fed Reserve announcement will be this week’s economic highlight. On the US data front, investors are still playing catch up and have returned to scrutinizing economic numbers and earnings reports in haste. One obvious note was that consumer sentiment was very much tainted by the recent government closure while elsewhere data, including the flash PMIs below, were mixed.  USD/JPY" height="200" border="0" width="300">

USD/JPY" height="200" border="0" width="300">

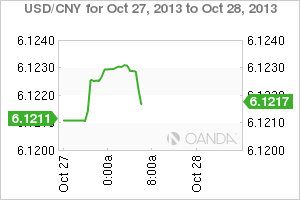

The "cheaper" global cash pool is seen as a constant ally for equity markets everywhere. Overnight saw Asian bourses moving higher, with Australia hitting a five-year high, as share prices rebounded from last week's closing-out US down-move. Equities are in recovery mode, especially after China alarmed investors with their elevated money market yields last week. Higher interbank lending rates saw bourses struggle, allowing the Yen to dominate outright, and help the Nikkei to end down -3.3% on the week.  USD/CNY" height="200" border="0" width="300">

USD/CNY" height="200" border="0" width="300">

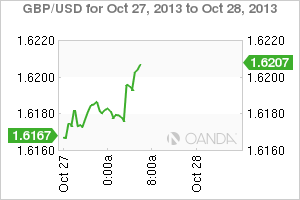

The theme of elevated Chinese yields has not changed – bonds end lower this Monday, as liquidity remains tight. Tomorrow's upcoming 'open market operations' by the PBoC will be watched with interest. Expectations will not have changed; Chinese policy makers are expected to refrain from any influencing. By day's end and a similar global theme is that the bond market remains depressed due to the lack of demand – most fixed income products provide a paltry return. Only when global yields have moved significantly higher will money market and bond instruments again look appealing to the average investor. The positive US handover from financial markets (S&P's shutout record) have aided global equities to return to a winning form thus far. This week promises to be another busy week on the US earnings front and is sure to make an impact on the various asset class prices. GBP/USD" height="200" border="0" width="300">

GBP/USD" height="200" border="0" width="300">

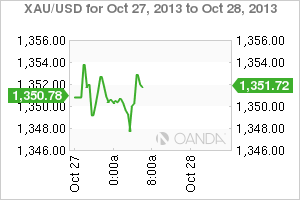

Last week saw the once "mighty" US dollar retreat against the JPY, EUR, GBP and the CHF but advanced against the growth and commodity sensitive currencies — the AUD and CAD in particular (vocal central banker in particular). Mixed economic data and US earning reports, thrown in the Fed maybe delaying its $85b-a-month stimulus program, has had a huge negative impact on the USD. But the combination of weaker economic data along with the negative fallout of the US partial government shutdown on growth provided reasons why the FOMC is expected to leave its monetary policy unchanged when it meets mid-week.  XAU/USD" height="200" border="0" width="300">

XAU/USD" height="200" border="0" width="300">

Do not be surprised to see this week's monetary policy meet as having less of an impact on the market now that investors have pushed their expectations for tapering to the end of Q1 in 2014. A December taper is still a possibility, but the odds for this taking place are very, very long. What is key about this Fed meet is how US policy makers choose to "characterize the economic and labor market environment as well as the delayed fiscal battle in Washington." A delayed budget and a problematic declining trend in US payrolls could easily push the "timing-to-taper" even further out next year, well beyond Q1. However, the market requires more transparent Fed guidance before it can push timing any further out. Until otherwise dissuaded, the rally on risk remains in play – a phenomena that should worry the "hawk." QE "infinity syndrome" makes the Fed's job of turning off the tap without causing much asset price damage very difficult indeed.

Original post

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Fed Meet Forces Dollar To Do Little

Published 10/28/2013, 07:01 AM

Updated 07/09/2023, 06:31 AM

Fed Meet Forces Dollar To Do Little

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.