Asset class prices continue to fluctuate, mostly on the market’s expectation of Fed tapering through QE easing later this year. The degree of ‘swaying volatility’ has already tapered somewhat, on the back of last week’s major positioning. Mind you, there are always a few last minute requirements that unnerve the weaker of market positions. This week’s highlights are primarily Fed related, including the FOMC statement, FOMC forecasts, and the chairman’s press conference.

The Fed’s communication skills had better be sharp, any miscommunication and the bleeding starts again. Investors will be looking for any changes in the regular statement and forecasts from ‘helicopter’ Ben and his fellow cohorts.

Despite having already done some significant pre-meeting asset price damage and rebalancing last week, the market hemorrhaging only stopped after a few Fed watch reports. They suggested that any bond tapering would be gradual in nature, and that rates would remain “low” for a considerable period of time. It was more about who delivered the message rather than the message itself – Hilsenrath’s piece (the Fed’s friend) at the WSJ. EUR/USD" width="400" height="300">

EUR/USD" width="400" height="300">

A communication challenge remains for the Fed’s team. Future Fed policy should undertake three distinct phases: tapering, pause and tightening. For many individuals the unknown variable is the length of time between each of the above phases. The market is expecting Bernanke to press home the point mid-week that there will be a considerable amount of time between ‘ending’ (note, not tapering) QE and raising rates. Ben needs to be very transparent when highlighting the point between “taking the foot off the gas and applying the brakes.”

“Tapering is not tightening”- Getting its message across in a clear and precise manner, with the least amount of market destruction, is not an easy task for central bankers. Separating the above three phases, especially as unemployment eases, is a trick not yet learned by any of them. However, it’s the Fed’s job to make the transition from each phase as smooth as possible, and investors will get to see how successful they have been doing this by mid-week. Leading into the Fed’s policy decision on Wednesday, the US CPI report and housing starts report could affect the “tenor of the hawks within the FOMC.” EUR/JPY" width="400" height="300">

EUR/JPY" width="400" height="300">

Some early euro data this morning continues to show signs of mild improvement within the region. Wage growth in Q1 picked up (+1.6%), as did April import numbers (€146.4b vs. €143b, m/m), which suggests that maybe Euro consumer demand is not yet dead. However, exports data for the region was down for the same time period (April exports €161.3b vs. €165.6b), making a “sustainable and even economic recovery that more elusive.” This was obviously something that the ECB was well aware of beforehand, otherwise they would not have cut their growth forecasts a few weeks ago.

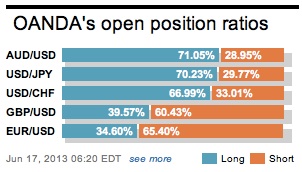

After having stayed short of the 17-member single currency for most of Q2, many speculators have been squeezed to square ahead of the Fed announcement. Despite the EUR managing to hold just above the accelerated trend support of 1.3300, weak Eurozone fundamentals and an improving US economy has bears thinking about reestablishing some of their ‘short’ positions again. Even with the technicals indicating that Euro longs should be favored, diverging data and rate differentials are supporting owning the USD. This market is anticipating a Fed to “talk a dovish book,” to ease some of the moves that have been supported by tapering expectations – creating a false EUR bid into FOMC?

According to technical analysts it’s hoping to stage a clear break above resistance at 1.3342 – the 61.8% retracement and late February high. If achieved, this would leave the immediate risks marginally higher and possible push through the optioned protected next big figure – 1.3400. Any momentum forcing the EUR below 1.3310, for a period of time, will open the door for the currency to test last weeks low at 1.3279. All jargon aside; many investors will prefer to wade to the sidelines until after the Fed. Some prior price action will make no sense and could be costly. Investors need clear and concise direction – let’s hope Ben and company is transparent enough.

Original post

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

False Euro Bid Into FOMC?

Published 06/17/2013, 08:22 AM

Updated 07/09/2023, 06:31 AM

False Euro Bid Into FOMC?

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.