Exelixis, Inc. (NASDAQ:EXEL) is scheduled to report third-quarter 2019 results on Oct 30, after market close.

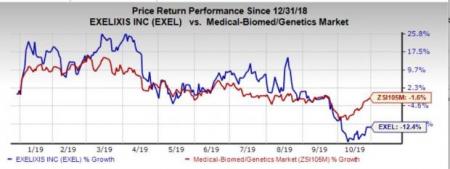

The company’s shares have lost 12.4% in the year so far compared with the industry’s decline of 1.6%.

Exelixis has an excellent earnings surprise history, having surpassed expectations in the trailing four quarters, with average positive surprise of 46.25%. In the last reported quarter, the company beat expectations by 8.70%.

Factors Likely to Impact Q3 Results

Strong sales of Exelixis’ lead drug Cabometyx boosted the company’s second-quarter 2019 results despite stiff competition. The upside was driven by continued growth in demand in the United States for the treatment of advanced renal cell carcinoma, a trend that most likely continued in the third quarter. Moreover, Cabometyx received another FDA approval for the treatment of patients with hepatocellular carcinoma in January and the demand is likely to have picked up well for the same in the to-be-reported quarter.

However, expenses are likely to have increased in the third quarter due to higher expenses associated with the company’s collaboration with Aurigene. In July, Exelixis announced an exclusive option and license agreement with Aurigene, a biotechnology company based in India focused on oncology and inflammatory disorders. Per the agreement, Exelixis will in-license up to six oncology programs from Aurigene.

Research and development expenses increased significantly in the second quarter, owing to high clinical trial costs, license and other collaborations, and the same is likely to have continued in the third quarter.

Meanwhile, investors are expected to focus on pipeline development. In July, Exelixis announced that two original cohorts are being expanded and four new cohorts are being added to the protocol for COSMIC-021, the phase Ib trial of Cabometyx in combination with Roche’s (OTC:RHHBY) Tecentriq in patients with locally advanced or metastatic solid tumors.

Apart from Cabometyx, Exelixis has other sources of revenues. In January, partner Daiichi Sankyo announced that Minnebro (esaxerenone) tablets were approved by the Japanese Ministry of Health, Labour and Welfare as a treatment for patients with hypertension. The compound was identified during the prior research collaboration between Exelixis and Daiichi Sankyo and has been subsequently developed by the latter. In May, Daiichi Sankyo launched Minnebro tablets in Japan and hence Exelixis will earn royalties on the sales of the same.

Earnings Whispers

Our proven model does not conclusively predict an earnings beat for Exelixis this season. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. Unfortunately, that is not the case here, as you will see below. You can uncover the best stocks to buy or sell before they're reported with our Earnings ESP Filter.

Earnings ESP: Earnings ESP for Exelixis is 0.00% as both the Zacks Consensus Estimate and the Most Accurate Estimate stand at 20 cents.

Zacks Rank: The company currently carries a Zacks Rank #4 (Sell).

Exelixis, Inc. Price, Consensus and EPS Surprise

Exelixis, Inc. price-consensus-eps-surprise-chart | Exelixis, Inc. Quote

Stocks to Consider

Here are some companies you may consider, as our model shows that these have the right combination of elements to deliver a beat this quarter.

United Therapeutics Corporation (NASDAQ:UTHR) has a Zacks Rank #1 and an Earnings ESP of +38.18%. The company is scheduled to release third-quarter results on Oct 30. You can see the complete list of today’s Zacks #1 Rank stocks here.

Amgen, Inc. (NASDAQ:AMGN) has an Earnings ESP of +0.04% and a Zacks Rank of 2. The company is scheduled to release third-quarter results on Oct 29.

Breakout Biotech Stocks with Triple-Digit Profit Potential

The biotech sector is projected to surge beyond $775 billion by 2024 as scientists develop treatments for thousands of diseases. They’re also finding ways to edit the human genome to literally erase our vulnerability to these diseases.

Zacks has just released Century of Biology: 7 Biotech Stocks to Buy Right Now to help investors profit from 7 stocks poised for outperformance. Our recent biotech recommendations have produced gains of +98%, +119% and +164% in as little as 1 month. The stocks in this report could perform even better.

Roche Holding (SIX:ROG) AG (RHHBY): Free Stock Analysis Report

Amgen Inc. (AMGN): Free Stock Analysis Report

Exelixis, Inc. (EXEL): Free Stock Analysis Report

United Therapeutics Corporation (UTHR): Free Stock Analysis Report

Original post

Zacks Investment Research