The U.S. economy is strong, but what will be next?

Rapid global economic growth last year was one of the drivers for the US GDP increase in 2018. But the current weakness of such global giants as Japan and Germany, combined with the emerging markets’ problems, can well slow down the US economic expansion in 2019; these factors may be as strong as the fading out effect of the fiscal stimulus and the Fed’s monetary restrictions. Everything is connected in the world; if the Federal Reserve put off hiking the interest rate in 2016 because of the turmoil in the Chinese financial markets and the referendum on the UK membership in the EU, then why couldn’t it do the same next year?

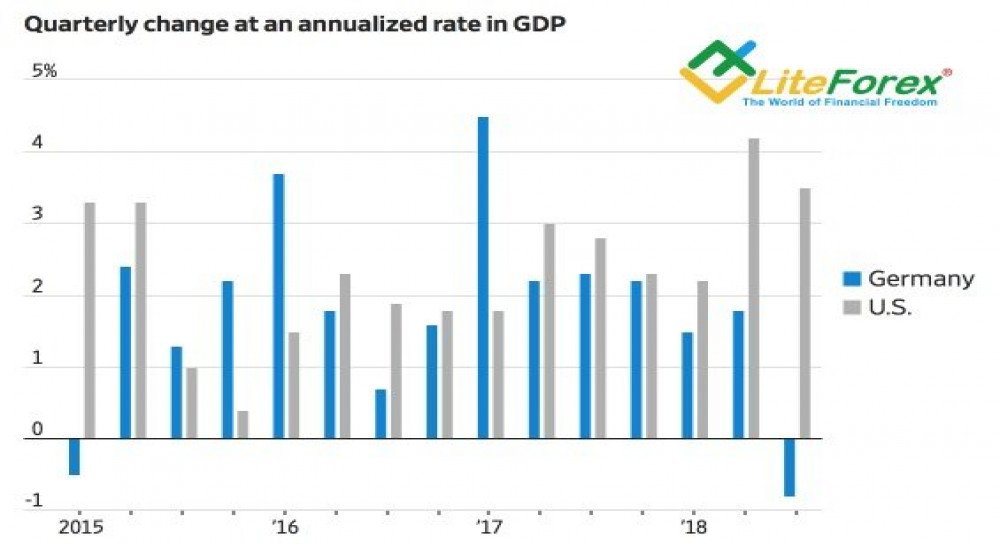

The released data on the GDP rate in Germany and Japan have become the further evidence that the economic growth-gap is still the growth driver for the USD rate. While the U.S. GDP growth pace performs one of the half-year results, the GDP rates in Germany and Japan are down by 1.2% and 0.8% Y-o-Y. The German index has been in the red zone for the first time over 3.5 years.

Dynamics of GDP rates in Germany and U.S.

Source: Wall Street Journal.

According to Jerome Powell, the U.S. economy is strong and sound. It is stronger than the others at the moment; the matter is what will be next. The troubles in Japan mostly result from natural disasters, and the disaster management will drive the GDP rate up. German car manufacturers are charged with tighter emission laws, and their adaptation to the new rule suggests that the German economy should surge in the near future. However, other countries are more sensitive to trade wars than the U.S. as they have larger shares of export in the GDP (29% for the global average, compared to 12% in the USA). These states should benefit from the deescalation of the US-China trade battle.

The US economy should face difficulties, resulted from the USD revaluation, tighter financial conditions, the weakening of the tax reform effect and the weakness of the US key trade partners. It should affect the pace of the Fed’s monetary normalization. The derivative market expects three federal funds rate hikes next year; however, if there are fewer of them, dollar is going to be under strong pressure. Even if the US consumer prices growth has been up at 2.5% Y-o-Y in October, it resulted from temporary factors, including a sharp increase in petrol prices, and higher costs of used cars after a decline in September. At the same time, the drop of WTI and Brent, slower growth of medical care costs and housing rentals suggest that the CPI growth is exhausting. And so, the Fed doesn’t need to rush and aggressively tighten its monetary policy.

Although the dollar bulls are gradually getting rid of it, fixing the profit, the euro isn’t bought as well. The Brussels’s response to Rome can be rather tough; and, if the UK parliament doesn’t support Theresa May’s plan, the GBP/USD and EUR/USD will drop rather deep. In this context, it makes some sense to consider selling the euro on the growth towards $1.1355 and $1.1445.