Today is all about resolving the tension between the still relatively weak euro currency while other indicators show strong optimism on the prospects for further stability. Also – AUD breaking key trend line today.

The aussie jumped higher through resistance (after a false break yesterday) around 1.0525 and traded above 1.0550 ahead of the European trading session after strong Chinese trade data showed a huge and unexpected rise in exports. Sure, data is what it is – but who is China exporting to in a world of weak demand, I’d like to know?

One of the CNBC guests being interviewed yesterday made the basic valid point that there are too many people producing too much stuff (overcapacity) and China is certainly at the center of the overcapacity problem. But this is a market that is not particularly interested in thinking and is more interested in reacting, though support for the aussie also came in the form of a strong performance put in by equities yesterday, which snapped back from Tuesday’s attempt at a small sell-off.

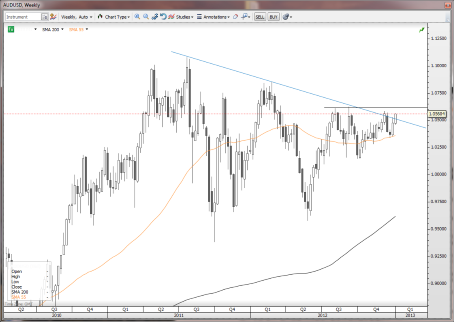

Chart: AUD/USD

A break is a break, and after several days of choppy indecision and false probes, AUD/USD has broken higher – only to be confronted by the bigger overhead resistance area presented by 1.0600+. But from a trend line perspective, the pair is already beginning to push the envelope and if asset markets continue to push higher, it’s hard to see what is going to stop an attempt at even more significant old range resistance starting with the old 1.0800+ and even 1.1000+ if we get a real third wave kind of rally going here – that’s a tough call as the pair has been a ranging mess for 18 months, but we are potentially breaking out of a major formation here. AUD/USD" title="AUD/USD" width="455" height="322">

AUD/USD" title="AUD/USD" width="455" height="322">

ECB preview

A small minority are looking for a rate cut today (I see it as unlikely as euro is riding quite a wave of optimism and I would think Draghi would save this cut for a rainy day) and there is discussion of negative deposit rates, but as Steen mentioned yesterday, a move to negative rates is far too contentious at this point in time as a way to force banks to lend (besides the fact that it’s crazy to force anyone to lend when you are on the downside of a credit cycle).

As I mentioned yesterday, various risk factors (bond yields, swap spreads, bank equity pricing) suggest that euro should be much stronger here, so I would expect we see some kind of resolution of the tension today and tomorrow in euro – either these factors begin to show some signs of fear or we see the euro beginning to recover again.

Remember that the longer term view remains worrisome: how will ECB/EU recapitalize its banking system without massive money printing and how will the periphery be able to withstand the ongoing crushing depression and even more austerity if the current course is to be maintained?

In a balance sheet recession – the only demand available is from the fiscal side due to the paradox of thrift, and there is no talk of new stimulus. The center can’t hold in the long run, even if the ECB is busy congratulating itself on its success in shoring up confidence in EU bond markets and the banking system in the short run. The work has only started if the EMU and the EU is to remain a going concern.

One key test besides Draghi’s press conference today will be the auction of Spanish debt today, with a few billion euro of 3-year to 10+ year debt to be auctioned at 0930 GMT today.

Technically, if we look at the most important EUR/USD cross, we have the obvious actual and psychological support at 1.3000 to the downside, while the zone of resistance to the upside remains up in the 1.3140-70 area. If we zoom back through that higher zone by the end of tomorrow, the chart is likely to look higher again, while the setup is nominally bearish if we remain below that area, with confirmation on a close below 1.3000.

Economic Data Highlights

- New Zealand November Trade Balance out at -700M vs. -698M expected and -666M in October

- New Zealand December QV House Prices out at +5.7% YoY vs. +5.7% in November

- Australia November Building Approvals out at +2.9% MoM and +13.2% YoY vs. +3.0%/+11.6% expected, respectively and vs. +19.2% YoY in October

- China December Foreign Exchange Reserves out at $3310B vs. $3317B expected and $3285B in November

- China December New Yuan Loans out at 454.3B vs. 550B expected and 522.9B in November

- China December Trade Balance out at +$31.62B vs. +$20B expected +$19.6B in November

- Sweden December CPI (0830)

- Sweden November Industrial Orders/Production (0830)

- Norway December CPI (0900)

- Spain debt auction (0930)

- UK Bank of England Announces Rate/Asset Purchase Target (1200)

- Eurozone ECB Announces Interest Rate (1245)

- Eurozone ECB Draghi Press Conference (1330)

- Canada November New Housing Price Index (1330)

- Canada November Building Permits (1330)

- US Weekly Initial and Continuing Jobless Claims (1330)

- US Weekly Bloomberg Consumer Comfort Index (1445)

- Japan November Current Account/Trade Balance (2350)

- China December CPI / PPI (0130)