EUR/USD fell on Draghi’s warning, then rose for hours as the ESM boat was floated, and then fell again on German Finmin comments. The technicals are inconclusive until we get a bigger move out of the range.

Overnight, the Shanghai composite continued its recent sharp rally and the Antipodean currencies responded with a strong tick higher before they weakened again in early European trading. The euro was weak as the ECB’s Draghi said that the EU faces risks from financial instability. The dip was sharp, but was over within half an hour and then EUR/USD spent most of the rest of the day meandering back higher.

Today sees Angela Merkel arriving in Athens for a visit with Greek leadership as the EU summit comes into view late next week (18th and 19th) and Greece tries to show that it has made enough progress to earn another round of financing from the Troika, which it might just receive, even if in the longer term Greece will need significant further debt reduction. Meanwhile, we’re in an odd sort of limbo on Spain, which has yet to request a bailout, and might not find it interesting to do so until/unless the market pressures it to do so.

And let’s consider who is behind Spain if it does indeed request a bailout – a rest-of-Europe funded ESM. Of that rest of Europe, France is a significant worry, not to mention Italy and increasing popular disgust there with the EU. But that’s for the longer term – for the short-term – bears must be frustrated that today’s low in EUR/USD failed to hold as the chart has been treacherous for both bears and bulls in a tactical sense.

JPY and Intervention and interest rates

The Japanese economics minister Seiji Maehara was out today saying that the BoJ needs to do more to achieve its goal of a 1 per cent CPI rate. He also said the law changes would be required if the BoJ is to purchase foreign assets in its easing (and currency weakening) efforts. It seems that BoJ intervention might remain ineffective if interest rates continue to fall globally and the focus is on merely buying up domestic debt, as Japan is still self-funding.

So, while the JPY might weaken anyway if interest rates push back higher again, a different avenue of JPY weakness could certainly arrive via such a change in the BoJ’s policy options. This is certainly something we should all have on our radar, as it would pave the way for intervention that would include buying up foreign bonds – possibly even ESM bonds as the noise goes.

Technically speaking, USD/JPY’s downside momentum is dead, with upside interesting on a follow up rally through 79.00. Meanwhile, it is interesting that the EUR/JPY has survived the attack on the 101.10 area support.

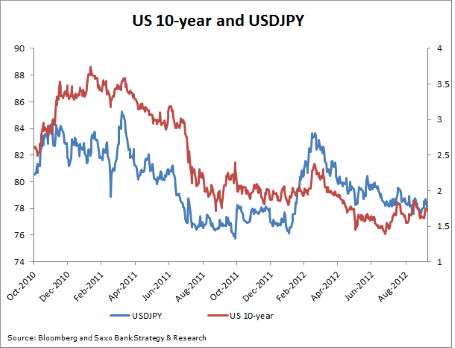

Chart: USD/JPY vs. US 10-year yields

USD/JPY failed to fall as much as the low yield environment suggested it should have over the summer as the market feared BoJ intervention when USD/JPY was working its way back toward the cycle lows, but more recently, yields suggest that the USD/JPY risk is more to the upside. A stronger signal is probably needed in bond markets, or from the BoJ/MoF before we get USD/JPY to sustain anything above 79.00. USD/JPY" title="US 10-Year And USD/JPY" width="455" height="348">

USD/JPY" title="US 10-Year And USD/JPY" width="455" height="348">

Looking ahead

The euro fell apart this morning and has since recovered somewhat as the jury is still out on where we are headed short term. 1.2800 is the important lower end of the range. To the upside, this morning’s highs are important resistance and If we reverse back above 1.3000 from here, it may keep the pair in the overall range for a good while longer.

Just before we are posting this, we have German Finance Minister Schaeuble declaring that Greece has not been fulfilling its obligations and saying that the ESM treaty doesn’t cover “legacy assets” (old bad debts as opposed to new issuance, though what happens if a country issues new debt to deal with old, bad assets, one wonders…), which might be considered somewhat of a stumbling block. The timing of his comment on Greece is rather interesting, given Merkel’s visit today.

Economic Data Highlights

- UK September BRC Sales Like-for-Like rose +1.5% yoY vs. -0.2% expected and -0.4% in August

- UK September RICS House Price Balance out at -15% vs. -20% expected and -18% in August

- Japan August Adjusted Current Account Total out at ¥722.3B vs. ¥520B expected and ¥335.4B in July

- Australia September NAB Business Conditions out at -3 vs. 0 in August

- Australia September NAB Business Confidence out at 0 vs. -3 in August

- UK August Visible Trade Balance out at -£9844 vs. -£8500 expected and -£7337 in Jul.

- US September NFIB Small Business Optimism out at 92.8 vs. 93.5 expected and 92.9 in August

- Canada September Housing Starts out at +220.2k vs. 205k expected and 225.3k in August

- UK September NIESR GDP Estimate (1400)

- Australia October Westpac Consumer Confidence (2330)

- US Fed’s Yellen to Speak (0030)