A weak inflation number in yesterday’s December report for the EU will sharpen attention on today’s Eurozone updates for retail sales and unemployment. Another round of discouraging data may force the European Central Bank to unveil more monetary accommodation at tomorrow's interest rate announcement. Following the macro news in Europe, ADP today publishes its estimate of private-sector payrolls for the US.

EU Retail Sales (10:00 GMT): The unexpected dip in the year-over-year pace of consumer inflation in the flash estimate for December raises the stakes with today’s update on retail sales. The 0.8 percent annual rise in the headline consumer price index (the market was expecting inflation to remain unchanged at 0.9 percent) is a reminder that the threat of disinflation/deflation continues to stalk the Eurozone. Particularly troubling is the drop in core CPI (ex-food and energy) to an annual rate of 0.7 percent—the slowest gain in the EU’s inflation history, which dates to 1996.

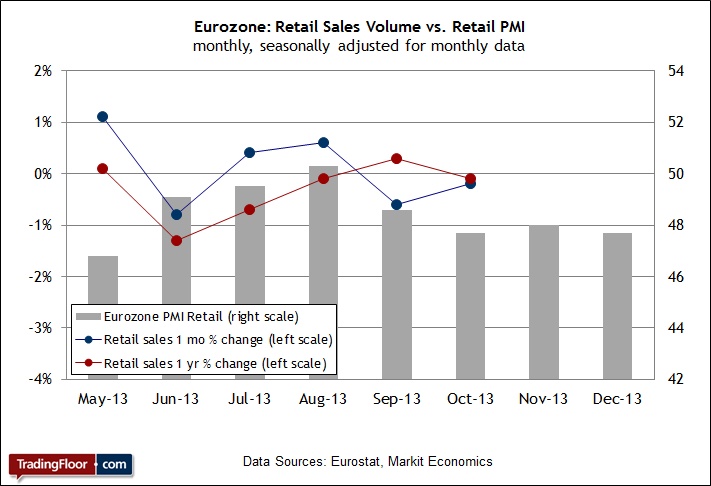

The antidote, of course, is growth, and so today’s release on retail spending will be closely watched for deciding if yesterday’s CPI news is noise or a sign that Europe’s prospects for recovery are fading once again. The retail numbers will also influence thinking on whether the European Central Bank (ECB) will roll out a new phase of monetary stimulus at tomorrow's monthly announcement.

Economists think we’ll see retail spending turn higher in today’s update for November, which would offer a degree of relief from October’s red ink. But looking ahead via the Eurozone’s retail purchasing managers index (PMI) doesn’t offer much support for thinking positively. In the November and December reports, the retail PMI data remained under the neutral 50 mark, which is a sign of falling retail sales. A higher level of spending in today’s hard data would help minimise the worry, but the PMI trend suggests caution for projecting a meaningful recovery in the near term.

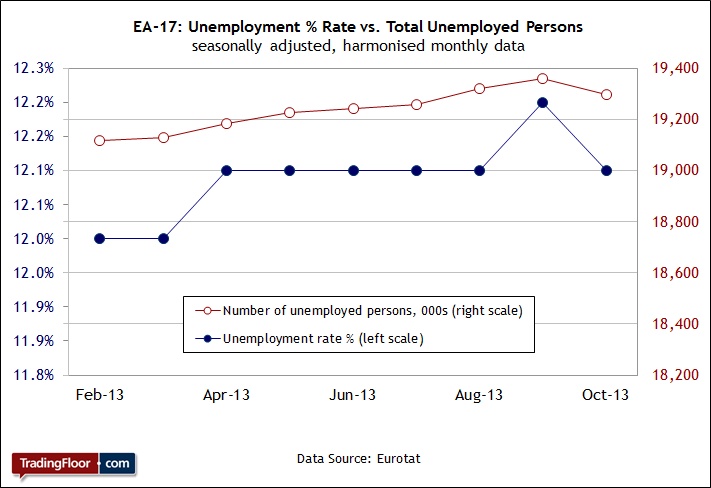

EU Unemployment (10:00 GMT): The jobless rate is a lagging indicator and so this data is of limited value for assessing the current state of the business cycle. But with the ongoing weakness in inflation raising concern that the Eurozone recovery is vulnerable, it’s going to be hard to ignore today’s unemployment report if the rate inches higher in the estimate for November.

Analysts, however, think that the jobless rate will remain steady at 12.1 percent, according to the consensus forecast. But that’s still close to a record high. In any case, the reaction to a steady jobless rate will be influenced by the retail sales numbers for Europe that are also scheduled for release today at 10:00 GMT.

Whatever the outcome in today’s unemployment report, it's sure to remind the world of the sharp contrast between the macro trend in Germany versus the rest of the Eurozone. Indeed, the Bundesbank yesterday reported that the number of unemployed workers in Europe’s leading economy dropped the most in two years in December. “A robust jobs report for the end of the year provides further support for a strong finish to 2013 from consumer spending [for Germany],” says an economist at Berenberg Bank in London. “Strong labor-market data raises the chances of stronger wage growth in 2014 and thus higher consumption.”

The only question is whether the divergence between Germany and its neighbors is on track to widen in 2014. Today’s unemployment report will bring new numbers for estimating the odds.

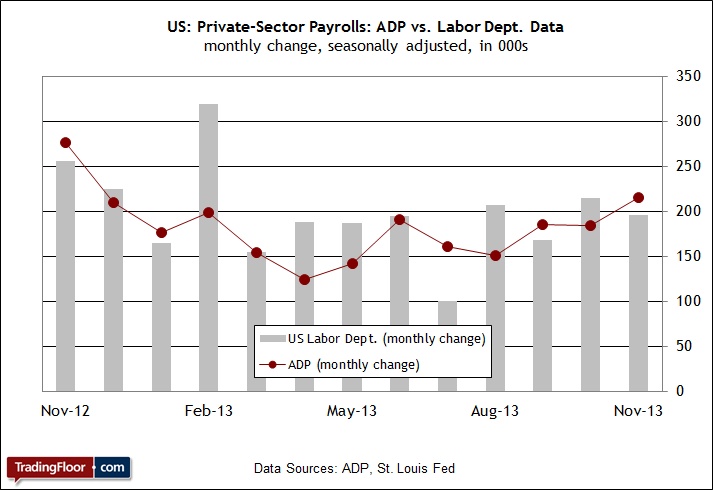

US ADP Employment Report (13:15 GMT): Today’s update from ADP provides a preliminary look at the labour market in the final month of 2013. The consensus forecast sees this measure of private payrolls rising at a pace above the 200,000 mark for the second month in a row in December—a gain that’s in line with my econometric outlook. If the upbeat predictions hold, the rate of jobs creation for the private sector will post its best two-month stretch in a year. In turn, an encouraging report from ADP today will boost confidence that Friday’s official payrolls report from the government will bring good news too.

Analysts have been inclined to forecast stronger growth for the US economy in recent weeks, thanks in part to stronger numbers from a variety of indicators. That includes a bullish reversal in what had been a worrisome rise in jobless claims in early December. If today’s ADP report tells us that the economy continued to mint new jobs at a comparatively elevated level versus recent history, the news will inspire more predictions that the US economy is on track for faster growth in 2014.

In that case, last week’s commentary on the outlook for monetary policy from Philly Fed President Charles Plosser will resonate a bit deeper with investors. In a speech on Friday, he said that the central bank may be forced to “aggressively” hike interest rates this year to keep a lid on inflation if—if—banks begin shifting the huge pile of excess reserves into the economy by extending more credit to borrowers. “How fast will we have to move interest rates up?,” Plosser asked. “We don’t know the answer to that,” said the banker, who is scheduled to become a voting member of the Fed’s FOMC in 2014. Much depends on the economy's strength in the months to come. Meantime, today’s ADP number will dispense fresh guidance on deciding how to answer Plosser’s question.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

EU Retail Sales And Unemployment, US ADP Jobs

Published 01/08/2014, 06:20 AM

Updated 03/19/2019, 04:00 AM

EU Retail Sales And Unemployment, US ADP Jobs

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.