Euro complacency appears high while the chart shows the euro on the defensive – will the ECB clear things up? Also, the JPY rally has so far proved short-lived as the yen weakened again on new BoJ speculation.

The JPY weakened sharply again as speculation noise is increasing on the BoJ adopting a 2% inflation target in line with the new government’s hopes at its January 21-22 meeting. A strong rally in Asian equities also boosted JPY crosses. A Wall Street Journal article yesterday discussing some Japanese companies’ concerns that too much, too fast in JPY weakening might not be a good thing and this may have helped fuel some of the consolidation, but the quick return of USD/JPY back above 87.25 after an attempt below discourages the downside view for the moment.

Additionally, news stories of the government’s new stimulus plans and the possibility of increased military spending are additional worries for the yen from the sovereign debt load perspective. Still, it’s a long wait for that BoJ meeting and now that we have established two-way volatility in JPY crosses, the going is likely to get more treacherous from here for JPY bears.

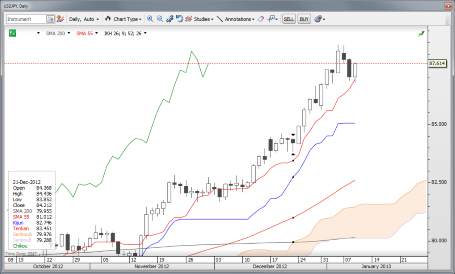

Chart: USD/JPY

Note for JPY traders that the USD/JPY support was found very close to today’s Tenkan line, which I mentioned yesterday as an important trend support. It’s worth the trader’s while to be aware of these Ichimoku levels when the JPY crosses are on the move. USD/JPY" title="USD/JPY" width="455" height="274">

USD/JPY" title="USD/JPY" width="455" height="274">

Fed’s Lacker

Last night, the Fed’s Lacker was out with his usual hawkish rhetoric on the risks from Fed policy feeding into inflation and said that the economy is strong and will grow about 2% this year. But Lacker is not in the majority and loses his voting status in 2013.

UK Trade Balance vs. upcoming US Trade Balance

The UK trade balance number was a bit weaker than expected – this serves as our monthly reminder of how little the GBP weakness of recent years has failed to begin to “fix” it’s terms of trade. US Trade numbers, by contrast, are beginning to trend toward balance again, helped by years of a weak US currency, growing US oil production and falling oil consumption.

Looking forward, a pinch in general consumption from upcoming austerity and the re-shoring phenomenon could lead to strong further improvements in the year ahead. Let’s see if Friday’s November US Trade Balance number provides further positive surprise on this account.

Looking ahead

German Industrial Production numbers up shortly could be a trigger for short-term volatility.

It’s all about tomorrow’s ECB meeting (with a sideshow of a Spanish debt auction as well). To judge from peripheral spreads and European bank shares, complacency continues to rise in Europe, though this is not reflected on the euro charts at the moment. Perhaps there is a desire to see the other side of the ECB meeting before giving into the positive euro vibes in FX?

Certainly, while my longer term view on the euro is cloudy at best, it’s a bit of a struggle to see why it is under pressure at this snapshot moment in time. A rate cut from the ECB (nontrivial, but still relatively low odds) tomorrow might require a one-off move lower in euro, but more widespread signs of concern about the EU project need to crop up from here for our bearish euro view to get more traction.

Regarding the considerable confusion triggered by the most recent FOMC minutes and the apparent risk that Fed balance sheet expansion could end sooner than expected despite the recent September and December QE3 and “QE4” (it seems the market is losing enthusiasm for numbering the QE’s), Mr. Bernanke’s town hall appearance on Monday is taking on added significance as it will be a tall task for him to explain what is going on.

Other FOMC members will be out speaking in similar appearances next week, which will be an interesting one for Fed watchers. See Steen’s post yesterday on the idea that Mr. Bernanke is strongly considering his legacy, and his term will run out at the end of January next year.

Also, considering that global markets are rotating on an axis of Fed money printing, it won't be long before we begin to see heightened expectation of who will replace Bernanke (especially assuming he soon announces that he won’t run for reappointment). Expect Obama to go with the least imaginative, most expected choice…but still…the process becomes very interesting if we get a bout of volatility or market disruption that can be pinned on Fed policy before or during the nomination process.

Economic Data Highlights

- US November Consumer Credit out at +$16.04B vs. +$12.75B expected and +$14.08B in Oct.

- New Zealand November Building Permits fell -5.4% MoM

- Australia November HIA New Home Sales rose +4.7% MoM (0005)

- UK December BRC Shop Price Index rose +1.5% YoY vs. +1.7% expected and vs. +1.5% in November

- Australia November Retail Sales fell -0.1% MoM vs. +0.3% expected

- Norway November Retail Sales out at +0.3% MoM and +2.4% YoY vs. +0.9% expected (MoM) and vs. +3.8% YoY in Oct.

- UK November Visible Trade Balance out at £-9164M vs. £-9000M expected and £-9487M in Oct.

- Germany November Industrial Production (1100)

- Canada December Housing Starts (1315)

- US Weekly DoE Crude Oil and Product Inventories (1530)

- New Zealand November Trade Balance (2145)

- New Zealand December QV House Prices (2300)