Both G-10 and EM currencies have now pared back nearly all of their respective October gains versus USD as global growth uncertainties have been unrelenting. Headlines and data developments on the eve of the Thanksgiving holiday in the Americas culminated into an almost perfect backdrop for the US Dollar to begin its Thanksgiving feast a day early.

Dexia bailout concerns, sub-50 China HSBC PMI, disappointing preliminary German and French Manufacturing PMIs, and the poorly received 10yr German bund auction (sold €3.6bln with a 2% coupon at an average price of 100.150 & yield of 1.980%) sent risk assets plunging lower across the board on Wednesday– the S&P 500 shed -2.21%, silver lost about -2.5% of its luster, crude oil prices ended in the red by about -2% on average, and UST 10yr yields closed the day out -1.75% lower.

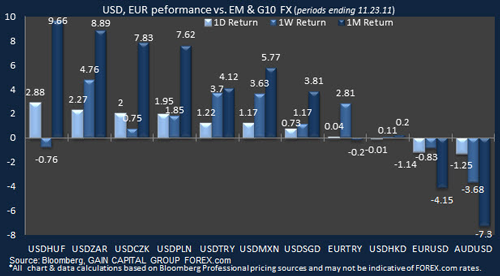

In currency markets, USD gobbled up most G-10 and EM counterparts as its relative liquidity advantage alongside recent US: Euro-area data divergence sent currency flows pouring into the safety of the greenback.

In the EM FX space, South Africa’s Rand has been the clear underperformer – USD posted gains just short of +5% versus ZAR over the past 1-week period. The Hungarian Forint, generally near the top of the underperformer leaderboard actually outperformed other emerging market currencies as reported talks of IMF aid sent USD about -0.76% lower versus HUF.

Despite a broad-based exodus out of EM currencies, GEM (Global Emerging Market) equity fund flows are still net positive with inflows just short of $3bln so far in the 4Q (week-ending Nov. 16th). Redemptions out of EMEA (Europe Middle East & Africa) remained in trend but were more than offset by a preference for Asia (ex-Japan) equity funds as inflows into China and Hong Kong firmed.

EM EMEA (Europe, the Middle East, and Africa) will be posted later this evening.

Dexia bailout concerns, sub-50 China HSBC PMI, disappointing preliminary German and French Manufacturing PMIs, and the poorly received 10yr German bund auction (sold €3.6bln with a 2% coupon at an average price of 100.150 & yield of 1.980%) sent risk assets plunging lower across the board on Wednesday– the S&P 500 shed -2.21%, silver lost about -2.5% of its luster, crude oil prices ended in the red by about -2% on average, and UST 10yr yields closed the day out -1.75% lower.

In currency markets, USD gobbled up most G-10 and EM counterparts as its relative liquidity advantage alongside recent US: Euro-area data divergence sent currency flows pouring into the safety of the greenback.

In the EM FX space, South Africa’s Rand has been the clear underperformer – USD posted gains just short of +5% versus ZAR over the past 1-week period. The Hungarian Forint, generally near the top of the underperformer leaderboard actually outperformed other emerging market currencies as reported talks of IMF aid sent USD about -0.76% lower versus HUF.

Despite a broad-based exodus out of EM currencies, GEM (Global Emerging Market) equity fund flows are still net positive with inflows just short of $3bln so far in the 4Q (week-ending Nov. 16th). Redemptions out of EMEA (Europe Middle East & Africa) remained in trend but were more than offset by a preference for Asia (ex-Japan) equity funds as inflows into China and Hong Kong firmed.

EM EMEA (Europe, the Middle East, and Africa) will be posted later this evening.