Is the inflation surge easing?

Inflation in America stood at a 13-year high in July according to the CPI measure, unchanged from the previous month, as supply constraints and pent-up demand continued to exert upward pressure on a broad range of prices. Those pressures might be easing, however, as the month-on-month rate is forecast to decelerate for the second straight month from 0.5% to 0.4% in August. That should bring the 12-month rate down a notch to 5.3%. Although this would still be well above the Fed’s 2% target, it would add credence to the view that the current surge is temporary.

There was already some evidence of this in July when inflation for some items that had been a major contributor to the jump in CPI, such as used cars, cooled off significantly. However, inflation in other areas like housing costs and rent have only recently started to take off and could accelerate rapidly due to soaring demand and housing shortages, not to mention the end of the eviction ban and rent freeze.

Even if some of the predicted spikes in consumer prices don’t materialize quite so strongly, it’s looking increasingly likely that a lot of the upward drivers will persist for some time, especially on the supply side, and inflation won’t fall as fast as policymakers would like. For this reason, the Fed will probably not delay a decision to trim its asset purchases beyond the end of this year even as some signs of slowing growth are emerging.

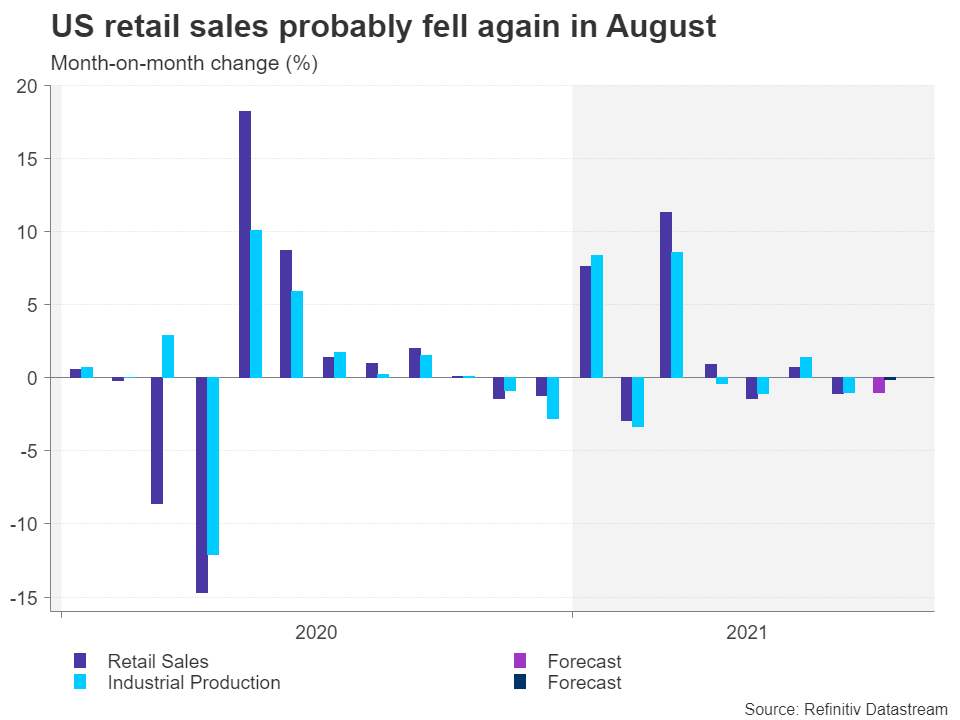

Falling consumption a worry

Thursday’s retail sales data could be another such sign. Retail sales are forecast to have declined by 1.0% m/m in August. Coming on the back of the 1.1% drop in July, this would paint a worrying trend for consumption, though the closely watched control group measure is expected to drop by just 0.1%.

The Delta variant is proving to be a much bigger bump in the road than anyone anticipated. Consumer confidence is falling, many firms have delayed a full return to the office and some airlines have already lowered their earnings guidance for the third quarter. Should more companies begin to downgrade their profit expectations, that could sound the alarm bells for Wall Street.

Has the Fed trapped itself into a taper corner?

But as far as the Fed’s taper timeline is concerned, policymakers are unlikely to get too concerned about weakening growth just yet and they appear to have set themselves on a course to flag a tapering decision for November at their upcoming meeting on September 21-22. Hence, any positive surprises in this week’s data would likely underscore tapering expectations, bolstering the dollar.

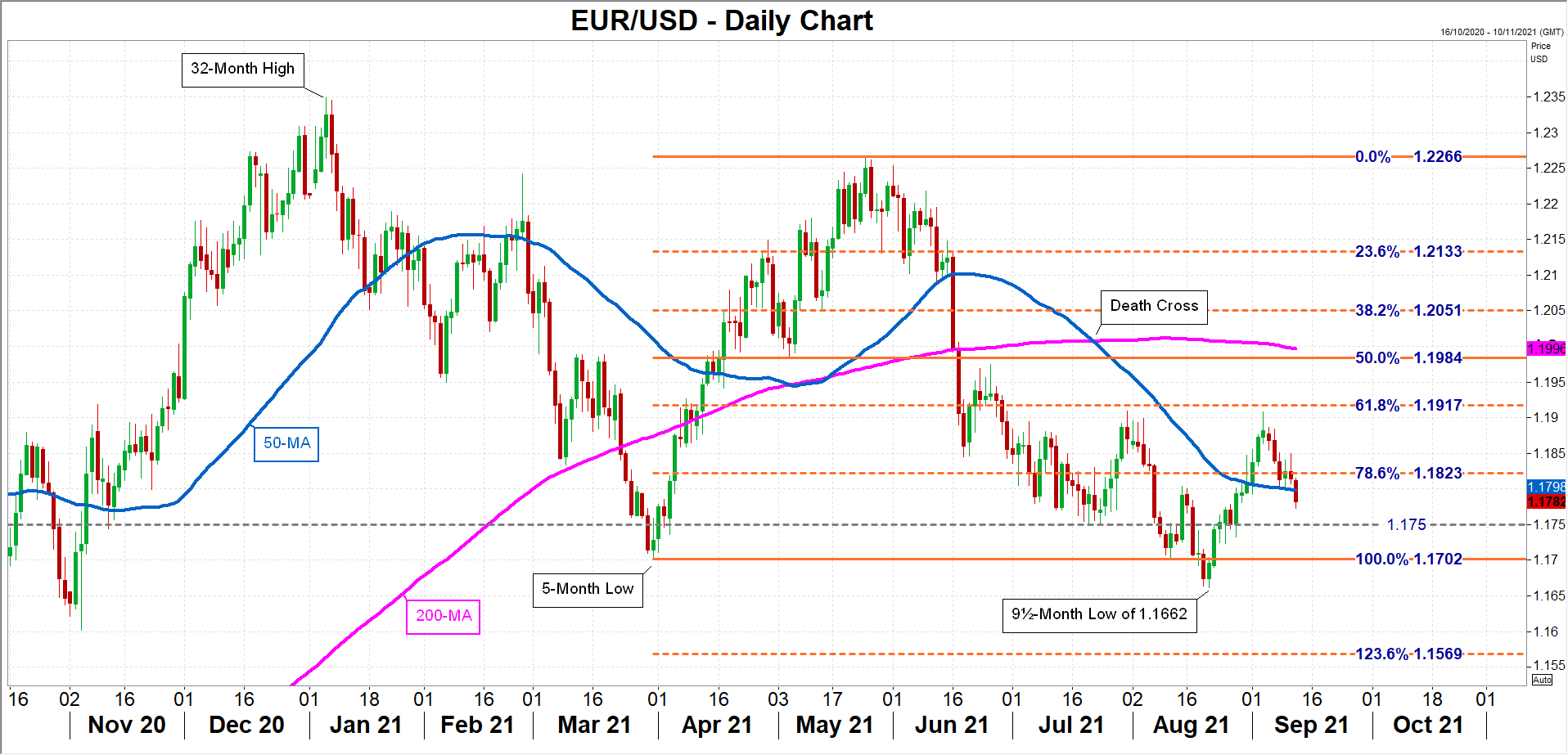

The greenback is extending its post-NFP gains, particularly against the euro, which just slid below its 50-day moving average (MA). If euro/dollar continues to decline, there could be some support for the pair around $1.1750. However, breaching this level would pave the way for a revisit of the 9½-month low of $1.1662 from August 20.

On the other hand, a big miss in either the CPI or retail sales reports could knock the dollar back, helping the euro to claw back above its 50-day MA and climb towards the 61.8% Fibonacci retracement of the March-May uptrend at $1.1823, which lies slightly above the September top.

A Delta storm might be brewing

Beyond the upcoming releases, there’s a growing risk that US data over the next few weeks will disappoint just as the Fed is preparing to scale back its massive asset purchases. At this point, it may be too early to get enough of a read on how much of an impact the Delta outbreak is having on the US economy. But if the Fed ploughs ahead regardless, the recent patch of unusually low market volatility might come to an end.