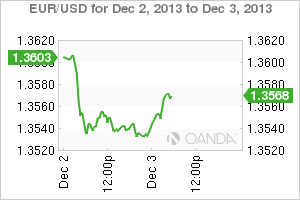

Many believe that the "mighty" dollar is on an edge and about to wake from its two-month slumber of trading in a tightly contained range. Improvement in US growth and the orderly move higher in treasury yields is sure to support the dollar. This is in stark contrast to what the market was exposed to during last summers Emerging Market flight. During that period, investors were wide-open to volatile spikes and relentless selling of EM assets on the belief that the Fed was about to ease their foot off the QE pedal. Stronger reported data, especially in the jobs sector Stateside this week could entice a December taper back into fray at the Fed's next meeting in a couple of weeks. EUR/USD" border="0" height="200" width="300">

EUR/USD" border="0" height="200" width="300">

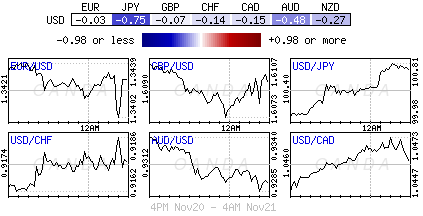

So far a range bound market continues to pan out for the FX majors. The dollar index (DXY) has failed just above its 100-DMA ahead of its November 25th high of 81.02. Its noted that the bulk of the current dollar longs are JPY based, which obviously has a limited influence on the DXY. However, market sentiment will still be influenced by any DXY's slide. Analysts fear that a close today back in the cloud (80.83-80) could encourage further dollar selling. Obviously on the other hand a broad dollar rise would appease all the dollar bulls that have been burnt outright on at least more than one occasion this year.

Yesterday's stronger than expected US ISM manufacturing reports (+57.3) have pushed treasury yields back towards this weeks high just shy of +2.80%. The employment component garnered much attention, printing its highest level in 18-months at 56.5. Will this bode well for Friday's employment numbers? Choppy trading in treasuries is to be order of the day for this week. Expect bond prices to be pushed about on Fed buybacks and a few deal pricings. It's important to follow US treasury yields, the dollars biggest supporter, thrown into that mix some stronger US data and a usually boring December may become very eventful, especially as we close in on the next FOMC meeting. AUD/USD" border="0" height="200" width="300">

AUD/USD" border="0" height="200" width="300">

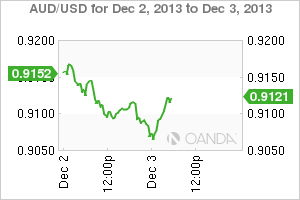

This week a plethora of Central Banks get to throw their weight around. Expect most policy makers to "whing and whine" about economic growth and inflation while throwing a few curves on the value of their domestic currency. Governor Stevens at the RBA seems to be on a one-man crusade to depreciate his previously precious Aussie dollar. Earlier this morning the RBA released nearly identical statement in its last policy decision of 2013, with no change in the wording for AUD, mining investment or the forward guidance paragraph. Again the committee was most notably concerned about their currency value, which it continues to view as "still uncomfortably high" despite a four-cent drop since the November decision. At its final board meeting of the year the Reserve Bank kept the cash rate at an all-time low of +2.5%, where it has stood since August. The board meets again in February. Governor Stevens said the board judged that rate settings were "appropriate." However, providing the AUD some support outright was the October retail sales topping estimates (+0.5%), along with the previous month's figure being revised higher (+0.9%). With an economy showing signs of some solid growth, selling AUD blindly could be a tad rich. USD/JPY" border="0" height="200" width="300">

USD/JPY" border="0" height="200" width="300">

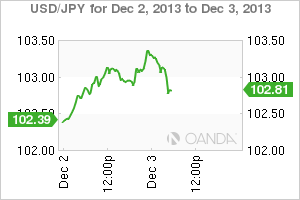

From Australia and across the Sea of Japan, the Yen remains under pressure amid further speculation that PM Abe's core CPI will not achieve its +2% target in 2-years. If that were the case, this would probably call for more BoJ easing further down the line. Currently, investors are investing in the Nikkei that continues to outperform as it's mostly tracking the softer yen. It's believed that the BoJ is planning scenarios for an expansion of its already massive economic stimulus program, looking to go beyond its $70b a-month bond-buying operation. It's speculated that policy makers require an additional package to bolster the Japanese economy ahead of the sales tax rise next April. Their options include major purchases of stock market linked funds or other assets riskier than Japanese government bonds (JGBs). Knowing the BoJ, expect more radical ideas to be floated. In the overnight session, USD/JPY rallied above 103.30, highest level since May, amid further speculation over the need for more BOJ easing. Being short Yen at such lofty dollar heights could be deemed at tad rich – touching a six-month dollar high has encouraged some investors to bank some profit ahead of BoJ meet. However, the better than expected US economic data has increased expectations of a near-term tapering of the FOMC's asset-purchase program – expect the market to favor buying USD on pull backs.  EUR/JPY" border="0" height="200" width="300">

EUR/JPY" border="0" height="200" width="300">

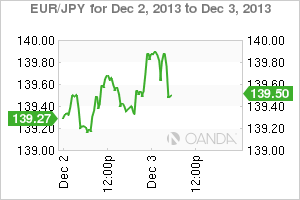

The 17-member single currency does not seem to want to make too much of a fuss just yet and this despite Draghi stating last week that trading north of 1.30 "harms the competitiveness of southern European exports." As the market heads Stateside, the EUR is managing to ease itself a tad higher, aided by the surprise drop in Spain's November Net Unemployment print this morning (-2.5k). The single currency's biggest supporter, similar to other major currencies, has been the yen weakness driving the EUR/JPY to five-year highs this morning. The techies continue to expect that cross to gain to 141.00, as new multi year highs are set today. However, currency direction rarely takes a direct route. The market talk of heavy USD/JPY offers above the 103.00 seems to have been correct, at least first time around. This has also allowed the EUR/JPY to suffer, pressurizing the cross to drop from an intraday high 140.03 to 139.47. The next big level for EUR support should be around 139.00.

The market can be expected to tighten up as the week progresses; especially ahead of Friday's US non-farm payrolls. Capital Markets expects a stronger print – anything disappointing and a December Fed taper will be priced out very quickly.

Original post

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Does The Dollar Have The Support To Head Higher?

Published 12/03/2013, 06:47 AM

Updated 07/09/2023, 06:31 AM

Does The Dollar Have The Support To Head Higher?

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.