The U.S. Dollar concluded the month on firm ground against the majority of its counterparts as better than expected data on Consumer Confidence and Business Activity bolstered speculation that the Federal Reserve may scale back on the $85 billion of monthly asset purchases. Furthermore, anticipation that the central bank may cut back on the current monetary easing prompted U.S. premiums to increase over those of Germany and Japan. Releases from the University of Michigan confirmed that the Index of Sentiment reached 84.5 in May; and Manufacturing in the Chicago area increased at the quickest pace in more than one year as it posted a seasonally adjusted 58.7 last month, rising from 49.0 in April. These positive numbers were issued after the Commerce Department revealed that U.S. Consumer Spending dipped 0.2 percent. The greenback advanced as much as 0.7 percent versus the basket of major currencies upon the release of Eurozone metrics which denoted that Unemployment reached a record high.

This week, major central banks will hold their meetings while important announcements regarding PMI and unemployment out of the U.S. are expected. Meanwhile, Gold prices fell the most in two-weeks subsequent to official data indicating that Consumer Confidence rose in the world’s biggest economy to the highest level in close to six years last month. As previously mentioned, the Thomson Reuters/University of Michigan’s Index on Consumer Sentiment climbed from 76.4 to 84.5. Gold Futures for August delivery dipped 1.3 percent and settled at $1,393 a troy ounce on the Comex Division of the New York Mercantile Exchange; this was the biggest decline for an active contract since mid-May, when Futures slipped 5.4 percent, making it the seventh drop in close to eight months.

The Euro declined after having traded at three-week highs versus the U.S. Dollar as demand for the 17-nation currency ebbed on announcements which revealed that German Retail Sales went down, and E.U. Unemployment reached a new record. The Euro was also weighed down by higher demand for safety brought on by uncertainty over the Federal Reserve’s next actions. The strong data issued on Friday raised speculations the Fed may cut back the current monthly purchases; however, metrics from the prior day showed that the U.S. economy expanded less than expected in the initial quarter of 2013. In the days to come, market investors will pay close attention to the outcome of the European Central Bank’s policy meeting. The British Pound also edged lower against the greenback at the end of last week, as uncertainty over whether the Federal Reserve will slow its easing measures supported demand for the U.S. monetary unit.

And while the greenback strengthened against most majors, it weakened against the Yen after the International Monetary Fund indicated that it supports the Bank of Japan’s efforts to raise consumer prices to 2 percent inflation by employing “sweeping enhancements” in its monetary policy structure. The IMF went on to explain that as long as the bank’s purchases meet domestic goals, they don’t see problems with the devaluation of the Yen. Japan’s currency rallied against all of its peers.

Lastly in the South Pacific, the Australian and New Zealand Dollars were sharply lower versus their U.S. counterpart on Friday. The Aussie came close to a 19-month low, while the Kiwi traded at an 8-month low on the possibility he Federal Reserve may reduce the amount of assets it purchases per month. The Reserve Bank of Australia will hold its policy meeting this week.

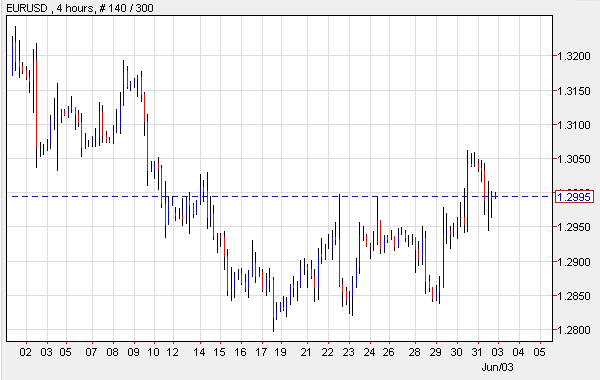

EUR/USD- ECB To Hold Policy Meeting

Analysts and experts in the Forex market believe this may be a wild week for the Euro, especially as the European Central Bank is scheduled to hold its policy meeting, and the U.S. will report on Non-Farm Payrolls. Furthermore, while the bank’s President, Mario Draghi is forecast to leave the interest rate unchanged, investors speculate policy makers may opt for expanding monetary easing. The Euro rose last week after the U.S. reported surprising surges in Consumer Confidence and Business Activity. It also benefitted from data issued by the European Commission which showed that Sentiment in the Euro-zone rose to 89.4 in May, the first hike since February. However, the shared currency fell off the highest price in three weeks versus the U.S. Dollar after Germany announced that Retail Sales dipped 0.4 percent in April, and Unemployment in the region hit 12.2 percent. EUR/USD" title="EUR/USD" width="600" height="380">

EUR/USD" title="EUR/USD" width="600" height="380">

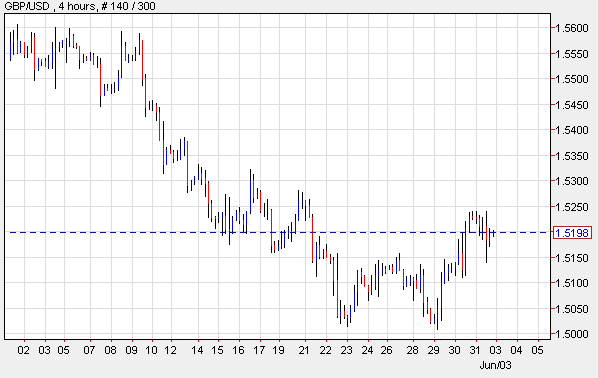

GBP/USD- Investors Look Forward To BOE Meeting

The British Pound edged lower against the greenback on Friday subsequent to the release of better than expected U.S. economic data which raised the possibility the Federal Reserve may consider reducing the amount of assets it buys per month. In the U.K., the Sterling climbed to a two-week high last week as the U.S. reported that its economy grew less than initially predicted in the first three months of the year. This week, investors will focus on the Bank of England’s policy meeting as well as on the release of U.S. Non-Farm Payrolls, since these may provide clues on how the Federal Reserve will proceed. The U.K. will also issue data on Manufacturing, the Services sector, Consumer Inflation and Construction. GBP/USD" title="GBP/USD" width="599" height="378">

GBP/USD" title="GBP/USD" width="599" height="378">

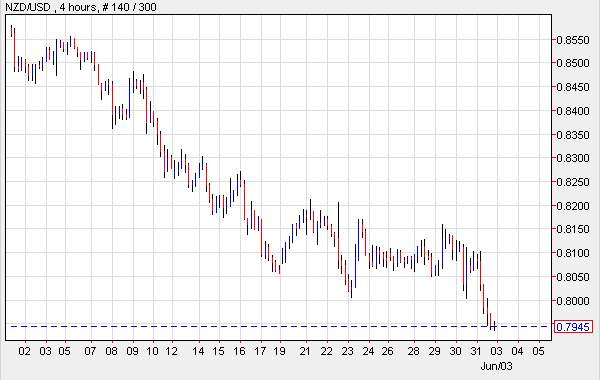

NZD/USD-Kiwi Reaches 8-Month Lows

The New Zealand Kiwi traded at an 8-month low versus its U.S. peer on concerns the Federal Reserve will end stimulus early. In the meantime, the South Pacific currency rose slightly as domestic data showed that the Business Confidence Index climbed from 32.3 in April to 41.8 in May. Analysts expect this may be an active week for the so-called Kiwi as China is scheduled to issue revised metrics on Manufacturing activity. NZD/USD" title="NZD/USD" width="600" height="380">

NZD/USD" title="NZD/USD" width="600" height="380">

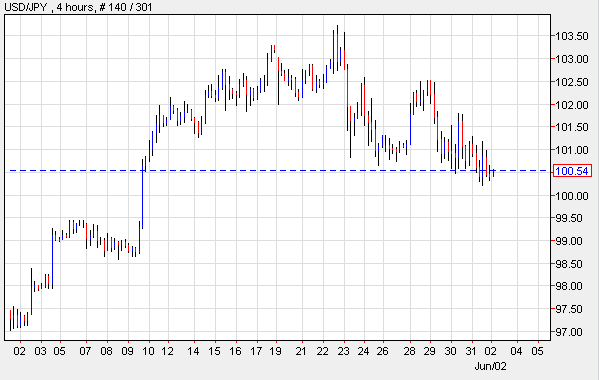

USD/JPY- Dollar Lower Than Yen

While the greenback advanced on Friday, it weakened versus the Yen amid speculations the U.S. central bank will cut back its asset purchases. The Yen was also supported by positive economic data out of Japan which revealed increases in Industrial Output. For many, this was indicative that Abenomics is a total success. The Ministry of Finance’s Money Flow Report revealed that Japan’s investors were still net sellers of foreign bonds; and it showed that U.S. Treasuries were “the major recipients of Japanese flows.” And with the support of the International Monetary Fund, who indicated that it backs the central bank’s measures to boost consumer prices to 2 percent, the Yen continued to rally. USD/JPY" title="USD/JPY" width="599" height="380">

USD/JPY" title="USD/JPY" width="599" height="380">

Today’s Outlook

Today’s economic calendar shows that the Euro region and the U.K. will release data on Manufacturing PMI. The U.S. will issue the ISM Manufacturing Index. Japan will announce the Monetary Base YoY. And Australia will publish the Current Account.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Daily Report: US Dollar Strengthened On Better Than Expected Data

Published 06/03/2013, 03:55 AM

Updated 09/16/2019, 09:25 AM

Daily Report: US Dollar Strengthened On Better Than Expected Data

iFOREX

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.