The U.S. Dollar traded mixed during subdued market activity and slipped against a number of majors including the Euro and the British Pound. The greenback received some support as market traders raised speculation that the upcoming Non-Farm Payroll reports will show that the U.S. economy is making progress, a major factor which could influence the Federal Reserve to start slowing down on its monthly asset purchases. According to some analysts, the central bank will place emphasis on keeping the interest rate low in an effort to ease investor concerns. Policy makers have indicated that they will reassure speculators in order to avert another sell-off of global assets should the central bank announce a cut back to stimuli. Meanwhile, some economists are anticipating that Gold Prices may be headed for the largest monthly fall since last June on the likelihood that the U.S. central bank may reduce the asset purchasing program in December. Bullion depreciated by $26.00 so far this year, as billionaire John Paulson indicated that he may not invest in the precious metal, as he and many other investors don’t consider gold a viable investment at this time. Gold appreciated 70 percent between December 2008 and June of 2011 while the Federal Reserve injected over $2 trillion into the system, boosting worries about accelerated inflation and a devalued Dollar. The good news is that Futures for February delivery climbed on the Comex on signs that demand for gold jewelry and bars has risen dramatically in China, the world’s second largest buyer. Futures traded at $1,250.40 a troy ounce last Friday on the New York Mercantile Exchange.

In the Euro region, economic announcements boosted the 17-nation currency, prompting it to rally close to a four-week high against the greenback, and came close to a five-year high against the Yen. The currency’s appeal improved after Eurostat reported a hike in Consumer Prices, increasing speculation that the European Central Bank may refrain from expanding its monetary easing program. The Euro was also supported by news out of Germany, denoting accelerated Inflation and an overall drop in the Unemployment rate for the entire Euro-zone. The British Pound also appreciated following additional positive macroeconomic fundamentals which confirmed a major increase for Mortgage Approvals. The currency traded high even as the central bank’s governor, Mark Carney, commented on the Loan Incentive Plan now in place, and suggested that the bank will now offer a greater number of businesses loans. Mr. Carney explained that the shift was due to concerns over a possible property bubble. The U.K. reported growth in the third quarter, another factor that propelled the Sterling to greater highs.

The Yen slipped to the downside against the greenback and the shared currency despite the fact that trading was thin due to the Thanksgiving Holiday weekend in the U.S. The depreciated Yen bolstered hopes that Japanese firms will show bigger earnings; however, a lower than predicted report on Industrial output weighed on the currency and caused the Nikkei to decline.

Lastly, in the South Pacific, the Australian Dollar remained under pressure days after the RBA governor Glenn Stevens indicated the likelihood of an intervention in the market in an effort to keep the value of the Aussie low. New Zealand’s Dollar rebounded, although its advance was capped by expectations that the Federal Reserve may scale back on bond purchases some time this month. The Kiwi was fueled by figures which denoted an increase in Business Confidence as well as a contraction in the Trade Deficit.

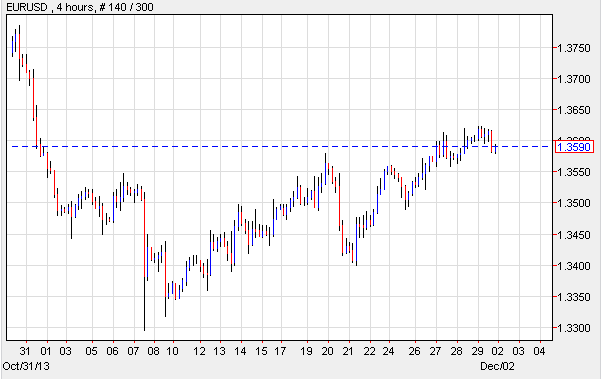

EUR/USD- Inflation Increases

The Euro finished the week stronger against the U.S. Dollar, subsequent to reports which confirmed that Germany’s Inflation rate rose more than anticipated, and Consumer Prices in the Euro-zone rose 0.9 percent from the prior year. The E.U. had issued a 0.7 percent inflation rate in October. And while the figures remain low, the upward movement eased concerns, which in the previous month caused the European Central Bank to cut the benchmark interest rate. The 17-nation currency was also supported by stellar news out of Spain showing that Gross Domestic Product came in as expected, and as the Unemployment rate went from 12.2 to 12.1 percent in October. This was the first decline for the unemployment rate since the beginning of 2011.

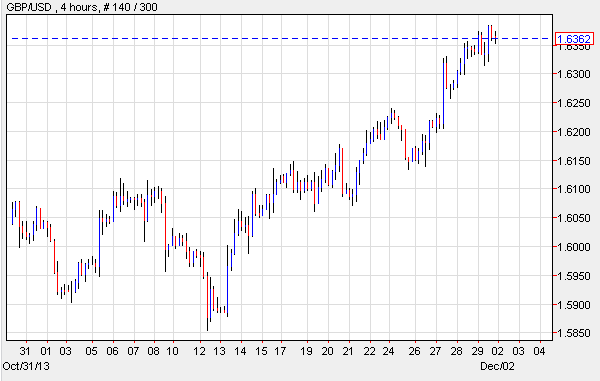

GBP/USD- Sterling Rallies To New Highs

The British currency gained versus the greenback, touching over two-year highs against the latter after data confirmed that Mortgage Loans rose to the highest level in close to six years, suggesting that the U.K.’s economic outlook remains positive. Friday’s fundamentals revealed that lenders issued 67,701 Mortgage loans in October. The British currency had started its rally days before, when it was announced that the British economy expanded 0.8 percent in the third quarter, and Consumer Spending climbed by 0.8 percent. The Sterling ignored comments by central bank governor, Mark Carney, who indicated that the “overheated” real estate sector could derail the economy, and added that the Bank of England would now focus on business lending.

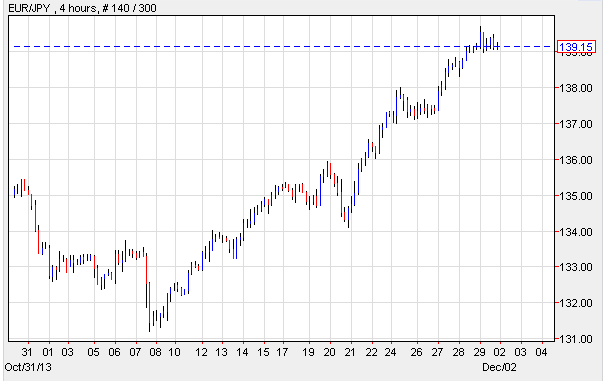

EUR/JPY- Euro Breaks Record Highs

The Euro inched higher against the Yen and traded close to a five-year high as the latter remained under pressure on speculation that the Bank of Japan may increase quantitative easing. Data issued over the weekend showed that Japan’s economy is improving, and that Abenomics is working as anticipated. The central bank is expected to expand stimulus in the coming months in order to lower the unemployment rate and reach an inflation target of 2 percent. On the data front, Japan announced that Household Spending climbed 0.9 percent in October, and Industrial Production surged 0.5 percent. Despite the fact that output fell short of forecasts, it still showed improvement. According to analysts, electric machinery production which drives output was sluggish, but it appears to be increasing. The Euro continued to trade high against the Yen following data which showed a decline in German Unemployment and better than estimated metrics for minor Euro-region reports.

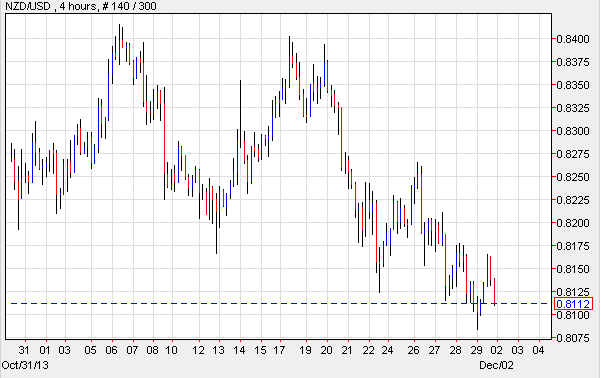

NZD/USD- Job Growth Supports Kiwi

The New Zealand Dollar advanced against the U.S. currency, but its gains were capped by the belief that the Federal Reserve may trim stimulus soon. The Kiwi rose as reports pointed to growth in the Employment sector along with higher rates of retirement, which bolstered speculation that the Unemployment rate could dip to 4 percent by 2021. Analysts have stated that payrolls are expected to increase by 180,300 between now and 2016, and perhaps by another 174,500 between 2016 and 2021. This means that the country’s economy could expand at a rate of 2.7 percent annually. The Kiwi was supported by news indicating that confidence among Business Entrepreneurs reached a 15-year high, despite the fact that Construction of New Homes slumped in October due to the restrictions on the low deposit lending program. The numbers revealed that approvals for loans to be used for building of homes and apartments dipped from 1,762 to 1,751 in October.

Today’s Outlook

Today’s economic calendar shows that the E.U. will report on Spanish and German Manufacturing PMI, as well as on the Euro-zone’s Manufacturing PMI. The U.S. will release data on Construction Spending, Manufacturing PMI and ISM Manufacturing PMI. Australia will publish Current Account, Retail Sales, the RBA Statement and the Decision on Interest Rates. Lastly, China will announce Non-Manufacturing PMI.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Daily Report: EUR/USD, GBP/USD, EUR/JPY And NZD/USD : December 02, 201

Published 12/02/2013, 04:15 AM

Updated 09/16/2019, 09:25 AM

Daily Report: EUR/USD, GBP/USD, EUR/JPY And NZD/USD : December 02, 201

iFOREX

Dollar Slips Against Euro And Yen

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.