- The physical oil market remains relatively bullish, with crack spreads and futures prompt spreads continuing to trend higher.

- This suggests the oil market is much tighter through the first few months of 2024 than many were expecting.

- However, as a result of refinery maintenance season and weather-induced refinery closures, crude oil demand has temporarily taken a hit, and how impactful this is to price will depend on whether refined product inventory draws can offset crude oil inventory builds.

- But, as refinery demand comes back online in the coming weeks, coupled with favorable seasonality, investor positioning, and a tight physical market, the oil price remains well supported for the time being.

Cautiously Bullish Oil

Crude oil’s fundamentals remain favorable and continue to suggest the oil market is much tighter than anticipated through the first few weeks of 2024.

Nowhere is this notion more prevalent than in the spectrum of global crude oil inventories. As we can see below, observable crude inventories on land, at sea, and in-transit have started 2024 at much lower levels than anything seen over the past five years.

Source: Morgan Stanely

However, as I noted within my recent oil market update, we continue to see a disparity between crude oil inventories and total crude and petroleum inventories, of which the latter includes refined products, notably gasoline, distillate, and jet fuel.

While crude oil inventories commenced 2024 below their seasonal averages and below 2023 levels, total crude and petroleum inventories did not.

Meanwhile, gasoline inventories saw significant builds to close out 2023 such that 2024 was commenced with inventories in-line with seasonal norms.

And finally, although distillate inventories still remain well below seasonal averages, they have started 2024 at higher levels than 2023.

The initial crude oil draws we saw to start the year were partly a function of the extreme cold weather during January, which took large parts of US oil production briefly offline.

In addition, this January cold blast also saw a drop in gasoline and diesel demand as road traffic temporarily took a hit, resulting in builds in gasoline and distillate inventories through January.

In the past few weeks, however, as US oil production has rebounded, we have seen the opposite occur.

Crude oil has seen builds such that in the US, inventory levels are now above seasonal averages, while total petroleum inventories have seen builds, as refined product draws have exceeded inventory builds.

Total crude and petroleum inventories now sit below seasonal averages.

What’s important to note here is the January draws in crude oil inventories (bottom chart below) were more than enough to offset the builds in refined products, for the most part, resulting in persistent below seasonal draws in total crude and petroleum inventories (top chart below). Given my preferred means to assess the inventory spectrum of the oil market is through the lens of total crude and petroleum inventories, this is most definitely a bullish dynamic. And, so long as product draws continue to offset any potential builds in crude, the inventory picture remains bullish in my book.

Alas, as we can see above, this was not case this past week and may not be the case for the next couple of weeks either. The recovery in crude oil production has occurred at a faster pace than the recovery in refinery demand, as refinery throughput remains down, headlined by the outage of BP’s ~400,000 barrel p/d refinery facility in Whiting, Indiana.

That this is also occurring amidst refinery maintenance season has led to refinery crude throughput and utilization rates drop to their lowest levels for this time of year in over half a decade. As refiners are the primary consumers of crude oil, a drop in refinery utilization coupled with a bounce back in crude production is a combination for builds in crude oil inventories, which is what we have seen this past week and will continue to see for the next week or two.

Unless gasoline and inventory demand are such that we see draws in these refined products offset builds in crude, this is a headwind the oil market will need to face for the next couple of weeks, and could limit short-term upside.

However, refinery utilization will recover as refineries come back online following the weather-induced outages and maintenance season. Most importantly, the incentives for refiners to increase crude throughput are present, with refining margins (i.e. crack spreads), continuing to trend higher, as we can see below. So long as gasoline and distillate crack spreads remain firm, the builds in crude oil are likely to be only temporary.

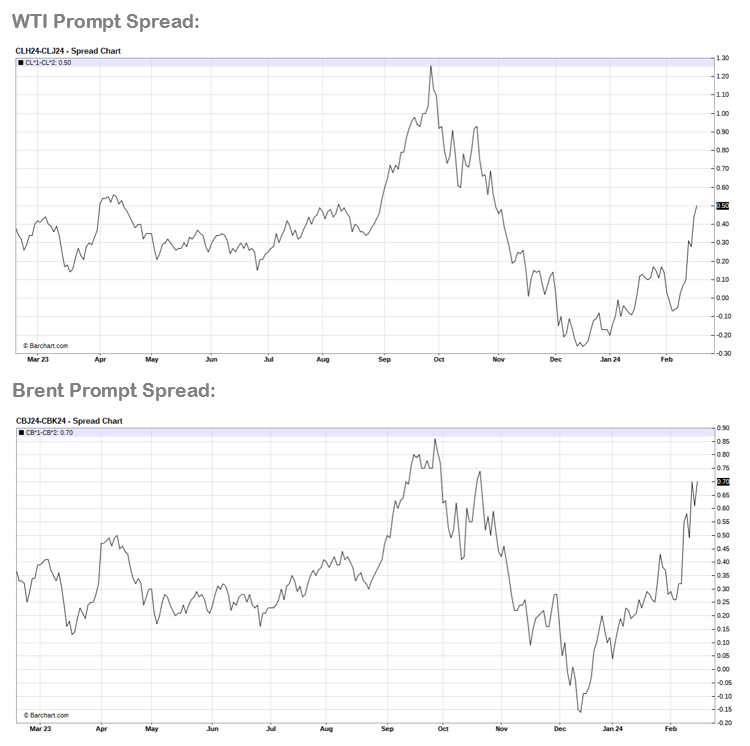

Meanwhile, the futures term structure for both WTI and Brent indicates the oil market remains tight, as evidenced by their current state of backwardation (which is being confirmed by backwardation in Brent CFDs and DFLs). Importantly, this backwardation is continuing to tighten at the front of the curve, as we can see below.

Meanwhile, both price and demand seasonality are turning bullish. This is true of both crude oil and refined products, with seasonal demand for refined products set to rise as we exit the northern hemisphere winter during a time where both gasoline and distillate inventories are now below their seasonal averages.

While we also continue to see OPEC+ implement their production cuts with relatively high levels of compliance. I would expect this continue for at least the next few months given the tightness in the market we are seeing.

In addition, OPEC+ remains well incentivized to keep a lid on production while speculators are still positioned bearishly as they currently are, as we can see below. If the tightness in the market continues and we see a prolonged combination of backwardated term structure, robust crack spreads and overall petroleum and crude inventory draws, speculative short covering could easily fuel oil prices into the mid-to-high $80s in short order.

Thus, as it stands, while there are short-term headwinds present stemming from a temporary drop in refinery utilization, the incentives from refiners to increase crude oil throughput as they come back online are present and should see this bearish dynamic itself be temporary so long as crack spreads don’t roll over from here.

In addition, should we see refined product draws offset crude builds during this period and the term structure remains in backwardation, the oil price should continue to be well supported through the first quarter of 2024, particularly as the market appears much tighter than consensus forecasts were expecting.