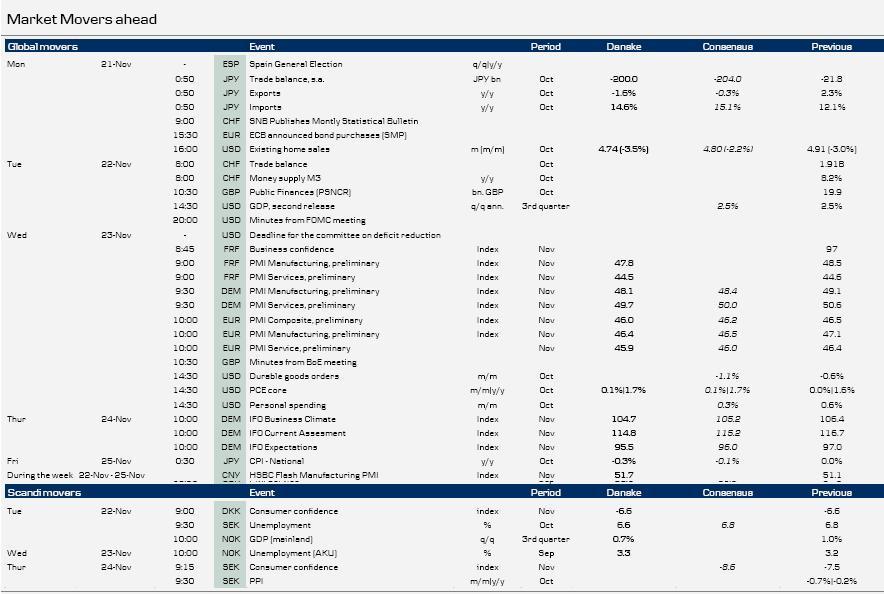

• US markets will be closed for Thanksgiving on Thursday next week. Data for core PCE is due on Wednesday. As the Fed’s preferred inflation measure, we will look to this to see whether inflation pressure is easing. We expect an increase of 0.1% m/m and 1.7% y/y, which is well within the Fed’s confidence band. On a similar note, minutes from the FOMC meeting earlier this month will be published. We hope to get some hints as to possibilities for further easing over the coming months, but we do not expect any major news from the release.

Data for durable goods orders for October is also due. In line with this week’s surprisingly positive industrial production, we expect a moderate increase in orders of about 1% since September, sticking to the overall trend of increasing domestic demand. On the same note, second estimates for third quarter GDP and private consumption are due. We do not expect any major revisions from the last release, as the strong trade figures are expected to be offset by weaker-than-estimated inventories.

• Another major focus next week will be on the deadline for the Joint Select Committee on Deficit Reduction – the so called ‘super committee’ in charge of presenting a plan for deficit reduction – on Wednesday. If the bipartisan committee does not succeed in reaching an agreement on a plan cutting the budget deficit by USD1.2trn over the next 10 years, it will be faced with automatic spending cuts across the board. This would be highly undesirable, as among other things, it would highlight the frozen state of the US legislature, and move a potential further downgrade of US debt closer.

• The general election in Spain on Sunday will attract attention, although it will probably make little difference for the sovereign bond market right now. In the short term, market sentiment depends heavily on the ECB purchases through the SPM programme. Mariano Rajoy and the centre-right Popular Party (with the slogan: Join the change) is expected to take over from Rodrigues Zapatero’s socialist government. Alfredo Perez Rubalcaba has taken over as the new leader of the socialist party. The two main challenges for the expected new centre-right government are to regain market confidence and to try to bring down unemployment from the current level of five million (21%).

• On the data front, there is a very interesting week ahead. We expect PMI data from Germany, France and the euro area to continue to send strong recession signals. In October, the PMIs decreased to just above 47 and the forward-looking new orders component dropped even further. We expect the PMI numbers to go even lower in November. Similarly, we expect the German Ifo data to contract further as the escalation crisis is now weighing on Germany. As we also wrote in Research Global: Euro area in recession, US and China recover, we expect a drop in the euro area GDP of 0.3% q/q in Q4.

• The Minutes from the Monetary Policy Committee’s latest decision will attract attention in markets as they could give a hint as to how close the Bank of England is to applying more monetary stimulus. If some members voted for more quantitative easing earlier this month, we might see an increase in the asset purchase target, currently at GBP275bn, already next month, while a unanimous vote for an unchanged target would probably signal no speed up in gilt purchases before January. The Inflation Report was very dovish, forecasting low growth next year and inflation to drop and remain below the 2% target in the medium term. We think the Bank of England will keep rates low for at least two years and perhaps even longer, to bring the economy back on track. Unemployment is currently high and rising so things are not improving as planned. The government will have to make serious revisions to its macroeconomic forecasts later this month and perhaps even come up with a Plan B to avoid recession.

• In Switzerland, the coming week brings money supply data, trade balance data and the publication of the SNB monthly Statistical Bulletin. However, key focus in the Swiss market currently is not so much on macro data, but rather on speculation about whether the SNB will hike the 1.20 floor. Local analysts have flagged the idea of a hike to 1.25 at the December monetary policy meeting and, as a result, and despite the escalation of the European debt crisis, the Swiss franc has weakened to trade around 1.24 against the euro.

• In China the most important release next week will be the flash estimate for HSBC manufacturing PMI for November. The HSBC manufacturing PMI in October improved from 49.9 to 51.1 and we expect this positive trend to continue in November when we expect HSBC PMI to improve further to 51.7. There is some uncertainty as to whether the current flooding in Thailand could have a negative impact because it has disrupted the supply chain, particularly within the global electronic industry.

• In Japan consumer prices for October will be released next week. We expect headline CPI inflation to decline from 0.0% y/y to -0.3% y/y and hence return to deflationary territory. The decline in inflation is solely due to fact that the impact from higher tobacco taxes in October 2010 will disappear in the year-on-year inflation rate. Nonetheless, Japan is one of the few countries where inflation remains substantially below the central bank’s inflation target (about 1% ) and for that reason at the moment is no major constraint on the Bank of Japan ability to expand its balance sheet more aggressively. Foreign trade data for November will also be released next week. Preliminary data suggests that exports have been relatively weak and imports resilient. For that reason, the seasonally adjusted trade balance not only remained in deficit in November, but the deficit also increased compared with October.

Data for durable goods orders for October is also due. In line with this week’s surprisingly positive industrial production, we expect a moderate increase in orders of about 1% since September, sticking to the overall trend of increasing domestic demand. On the same note, second estimates for third quarter GDP and private consumption are due. We do not expect any major revisions from the last release, as the strong trade figures are expected to be offset by weaker-than-estimated inventories.

• Another major focus next week will be on the deadline for the Joint Select Committee on Deficit Reduction – the so called ‘super committee’ in charge of presenting a plan for deficit reduction – on Wednesday. If the bipartisan committee does not succeed in reaching an agreement on a plan cutting the budget deficit by USD1.2trn over the next 10 years, it will be faced with automatic spending cuts across the board. This would be highly undesirable, as among other things, it would highlight the frozen state of the US legislature, and move a potential further downgrade of US debt closer.

• The general election in Spain on Sunday will attract attention, although it will probably make little difference for the sovereign bond market right now. In the short term, market sentiment depends heavily on the ECB purchases through the SPM programme. Mariano Rajoy and the centre-right Popular Party (with the slogan: Join the change) is expected to take over from Rodrigues Zapatero’s socialist government. Alfredo Perez Rubalcaba has taken over as the new leader of the socialist party. The two main challenges for the expected new centre-right government are to regain market confidence and to try to bring down unemployment from the current level of five million (21%).

• On the data front, there is a very interesting week ahead. We expect PMI data from Germany, France and the euro area to continue to send strong recession signals. In October, the PMIs decreased to just above 47 and the forward-looking new orders component dropped even further. We expect the PMI numbers to go even lower in November. Similarly, we expect the German Ifo data to contract further as the escalation crisis is now weighing on Germany. As we also wrote in Research Global: Euro area in recession, US and China recover, we expect a drop in the euro area GDP of 0.3% q/q in Q4.

• The Minutes from the Monetary Policy Committee’s latest decision will attract attention in markets as they could give a hint as to how close the Bank of England is to applying more monetary stimulus. If some members voted for more quantitative easing earlier this month, we might see an increase in the asset purchase target, currently at GBP275bn, already next month, while a unanimous vote for an unchanged target would probably signal no speed up in gilt purchases before January. The Inflation Report was very dovish, forecasting low growth next year and inflation to drop and remain below the 2% target in the medium term. We think the Bank of England will keep rates low for at least two years and perhaps even longer, to bring the economy back on track. Unemployment is currently high and rising so things are not improving as planned. The government will have to make serious revisions to its macroeconomic forecasts later this month and perhaps even come up with a Plan B to avoid recession.

• In Switzerland, the coming week brings money supply data, trade balance data and the publication of the SNB monthly Statistical Bulletin. However, key focus in the Swiss market currently is not so much on macro data, but rather on speculation about whether the SNB will hike the 1.20 floor. Local analysts have flagged the idea of a hike to 1.25 at the December monetary policy meeting and, as a result, and despite the escalation of the European debt crisis, the Swiss franc has weakened to trade around 1.24 against the euro.

• In China the most important release next week will be the flash estimate for HSBC manufacturing PMI for November. The HSBC manufacturing PMI in October improved from 49.9 to 51.1 and we expect this positive trend to continue in November when we expect HSBC PMI to improve further to 51.7. There is some uncertainty as to whether the current flooding in Thailand could have a negative impact because it has disrupted the supply chain, particularly within the global electronic industry.

• In Japan consumer prices for October will be released next week. We expect headline CPI inflation to decline from 0.0% y/y to -0.3% y/y and hence return to deflationary territory. The decline in inflation is solely due to fact that the impact from higher tobacco taxes in October 2010 will disappear in the year-on-year inflation rate. Nonetheless, Japan is one of the few countries where inflation remains substantially below the central bank’s inflation target (about 1% ) and for that reason at the moment is no major constraint on the Bank of Japan ability to expand its balance sheet more aggressively. Foreign trade data for November will also be released next week. Preliminary data suggests that exports have been relatively weak and imports resilient. For that reason, the seasonally adjusted trade balance not only remained in deficit in November, but the deficit also increased compared with October.